Issue 1, June 2026

Interviews

Empire Suicide Watch

Examining the anatomy of US power

Over the past eighteen months, the US has laid bombs down on Iran, Venezuela, Syria, Yemen, Somalia, Nigeria, Iraq, and across the Caribbean Sea, while threatening to deploy US troops to a host of other countries including Mexico, Ecuador, and Cuba. This escalation in global warfare—alongside trade conflicts and energy crises that have upended crucial supply chains—has had many questioning the rationality of American imperialism. What kind of empire is the American empire? Does Trump’s belligerent protectionism mark a break in American hegemony, or the reconstitution of a prior era of domination?

In the conversation that follows, Herman Mark Schwartz locates American empire in historical and comparative perspective. Drawing on debates within international political economy, Schwartz considers dollar centrality, the limits of US production and growth, and the endurance of American military power over the past century. Empires, Schwartz argues, have historically required forms of cooperation between the center and the periphery—it is this necessary collaboration that Trump’s global aggression threatens to disrupt.

Herman Mark Schwartz is Professor Emeritus of Politics at the University of Virginia. An economic historian, Schwartz’s work interrogates the relationship between state and market power. Among his many published works is the textbook States Versus Markets, now in its fifth edition, which examines the state-market relation through currents of globalization and economic crisis. Phenomenal World editors Maria Fernanda Sikorski and Jack Gross interviewed Schwartz in May 2026, over two months into the protracted US-Israeli war on Iran.

An interview with Herman Mark Schwartz

Maria Fernanda Sikorski: Let’s begin with the basics: What is an empire?

Herman Mark Schwartz: We tend to think of empires as a set of power relations that can be physically described on a map, coloring in the territorial reach of the Roman or the British Empire. This assumes that the empire depicted has some sort of clear beginning and end—everything not colored in is therefore not part of the empire. I think that is a fundamentally wrong understanding of how empires work. There is a gradient of declining cooperation and rising coercion moving out from the center.

The history of human civilization is in large part a history of empires: large-scale societies mobilizing enormous volumes of resources and exerting control over other human beings, whether by directing labor or regulating behavior in accordance with imperial objectives. At the root of this is the connection between violence and trade—between states and markets. All empires arise through control of long-distance trade.

States seeking to tax their populations often found that the most efficient and profitable strategy was to control long-distance trade and the circulation of luxury goods. Their scarcity made such goods valuable sources of revenue and, critically, these resources were extracted from the elites. Universally consumed commodities—most notably salt—became extraordinarily profitable once brought under centralized control. (This is why we saw salt monopolies in large-scale durable empires like those in China.) But the principal threat to central authority in large empires came from internal elites, and one of the most effective ways to extract resources from them—as they often resisted taxation—was through luxury goods. That’s what the tribute system was about: by controlling external trade, the state secured access to scarce goods and used their distribution to extract wealth via taxation, thereby maintaining leverage over potential internal rivals.

There’s a close connection between long-distance trade and political power. Empires are not necessarily, or uniformly, ruled by despots. Despotism, as Michael Mann demonstrated, is incredibly inefficient. Durable empires are based on cooperation and trade between elites at the center and elites in subordinated societies. But different elites strike different deals—some better than others, but the center always determines the rules of exchange, distribution, and political engagement.

If you look at the British Empire in the nineteenth century, some areas were ruled despotically yet technically formed part of the core of the empire, like Ireland, and others were self-governing dominions like the white settler colonies which had a far better deal. These latter colonies received disproportionate amounts of capital investment and a degree of limited autonomy. Then there were the Crown colonies under direct administrative control. South Asia was governed far more violently, but there was still buy-in from domestic elites.

Further down the chain of sovereignty were protectorates, where local laws, currencies, and languages persisted, but interactions with the empire came via the center’s language, law, and currency. The five largest non-white zones of the British Empire—the West Indies, the Straits Settlements, India, East Africa, West Africa—had their own silver-based currency that did not circulate beyond their respective zones, thereby suppressing investment and credit creation there. These currencies needed to be converted into British pounds through private British banks and local currency boards—colonial monetary authorities that issued local currency exclusively backed by reserves held in London. It was the center that decided the shift from private banks to colonial currency boards, and that the currency would be silver, not gold.

Of course, there have been differences within this general logic of empires across history, as social technologies and the capacity to mobilize labor and resources have significantly expanded, enabling a general shift from despotic regimes towards infrastructural power.

This shift explains the huge differences between the US empire and previous ones. First, it rests on an unprecedented scale of offshore endogenous credit creation, larger than what we saw under British hegemony. Second, the destructive capacity of modern warfare has expanded dramatically. Third, transnational corporations have become conduits for the diffusion of productive knowledge, accelerating economic catch-up. (One big challenge for the center is ensuring that the periphery is always kept behind.)

From the perspective of uneven and combined development, the central challenge for any imperial core is preserving the asymmetry between center and periphery—maintaining a decisive advantage in the capacity to mobilize resources and generate power. Yet under contemporary conditions, that gap tends to narrow far more rapidly than in previous eras.

Jack Gross: What is the difference between states and empires?

HMS: The belief that the Peace of Westphalia (1648) somehow set the world on a path away from ancient agrarian empires and toward a modern system of sovereign states is untrue for several reasons. As a historical matter, the end of formal empires—even within the Westphalian framework—is extremely recent. I was alive as some of the last countries were decolonized. And when you look at empires, heterogeneity is important—there are always zones of partial sovereignty and layered governance.

Many of the places we call states today are effectively in that same semi-sovereign position. Europe possesses greater local sovereignty and legal autonomy than many regions, but militarily it is very clearly semi-sovereign, and monetarily it sits a step below the Federal Reserve and the offshore dollar system. Europe also remains populated with American military bases, as do Japan and South Korea. And this is asymmetrical too: you won’t find German military bases in the US. What we conventionally describe as sovereign states are in fact components of a broader imperial system, differentiated by varying degrees of autonomy.

JG: How does the production and reproduction of elites and managerial layers fit into this view, both historically and in the present?

HMS: I’ll start by saying that no system of power is perfectly run. When a central power brings a peripheral one into the system of empire, it offers some sort of exchange, either by cutting semi-sovereign political entities into trade profits or by granting them more political power.

This would often happen through intermarriage. The Chinese dynasties managed rivals through dynastic marriages, integrating elites at the frontier into cooperative relationships with the imperial center. The Roman Empire operated as a gradient of economic integration centered on the Mediterranean, so as one moved toward the frontier, economic integration weakened and luxury goods became increasingly important relative to basic goods: the distribution of these luxury goods helped bind frontier elites to the center. In the British Empire, it was the ability to borrow money from London capital markets that enabled local landowners in Argentina or the US to accumulate wealth. In each case, local elites benefited from integration into imperial financial networks.

There are many similar mechanisms of political exchange at work today. The US has built a coalition around intellectual property rights (IPR) by mobilizing European firms in the pharmaceutical and tech sectors to lobby their governments to enforce those rights, which in turn enforces those firms’ profitability. US military protection of Europe, Japan, and Korea has a similar function.

What destabilizes imperial systems is often not revolt, but tensions within these bargains. In the Middle Ages, the typical problem was aristocratic tax exemption. This is what made the Spanish state so weak at the height of its empire. The British Crown, too, was weakened when the aristocracy, acting through Parliament, asserted control over taxation. These elite efforts ultimately worked to undermine the broader imperial structure on which elite security itself depended, leaving the system vulnerable to rival powers.

Today, elites are avoiding paying taxes in the US and around the world. The drop in corporate tax rates is hollowing out state capacity, as is privatization. The primary threat to imperial survival today is not from peasants or workers but from the strata of elites whose cooperation is necessary for making the system run.

When states’ own cadres lose sight of what it is they are meant to be doing, more issues arise. They might begin to prioritize their own private interests at the expense of their collective class interests. They might also simply get things wrong, or get locked into bureaucratic routines that don’t suit the reality of the moment. US military losses in the Gulf today are just one example. The US military, organized around expensive high-tech weapons systems, hasn’t realized that drones and AI have made protection of infrastructure and logistics more critical. Despite three years of drone war in Ukraine, they just keep running the same routines.

MFS: When would you say that the US became an empire? And is it in decline?

HMS: In the eighteenth and nineteenth centuries, the US was part of the imperial frontier. They were the local elites cooperating with the British imperial center, until, of course, they launched the American Revolution. The historian Mark Egnal argues that at the time of the Revolution, these local elites were already imagining the construction of an empire in North America, making plans to kick out the French, the Spanish, the Mexicans, and the native population, while striking deals with the British Empire.

The transformation of the US into the global hegemon is the result of two world wars, which knocked out several rivals, and the Cold War, which reduced its only potential challenger to a lower status. In historical terms, imperial dominance rested on the capacity to successfully wield violence. But if we want to understand how empire works, we need to disaggregate the sources of power and focus on concrete mechanisms.

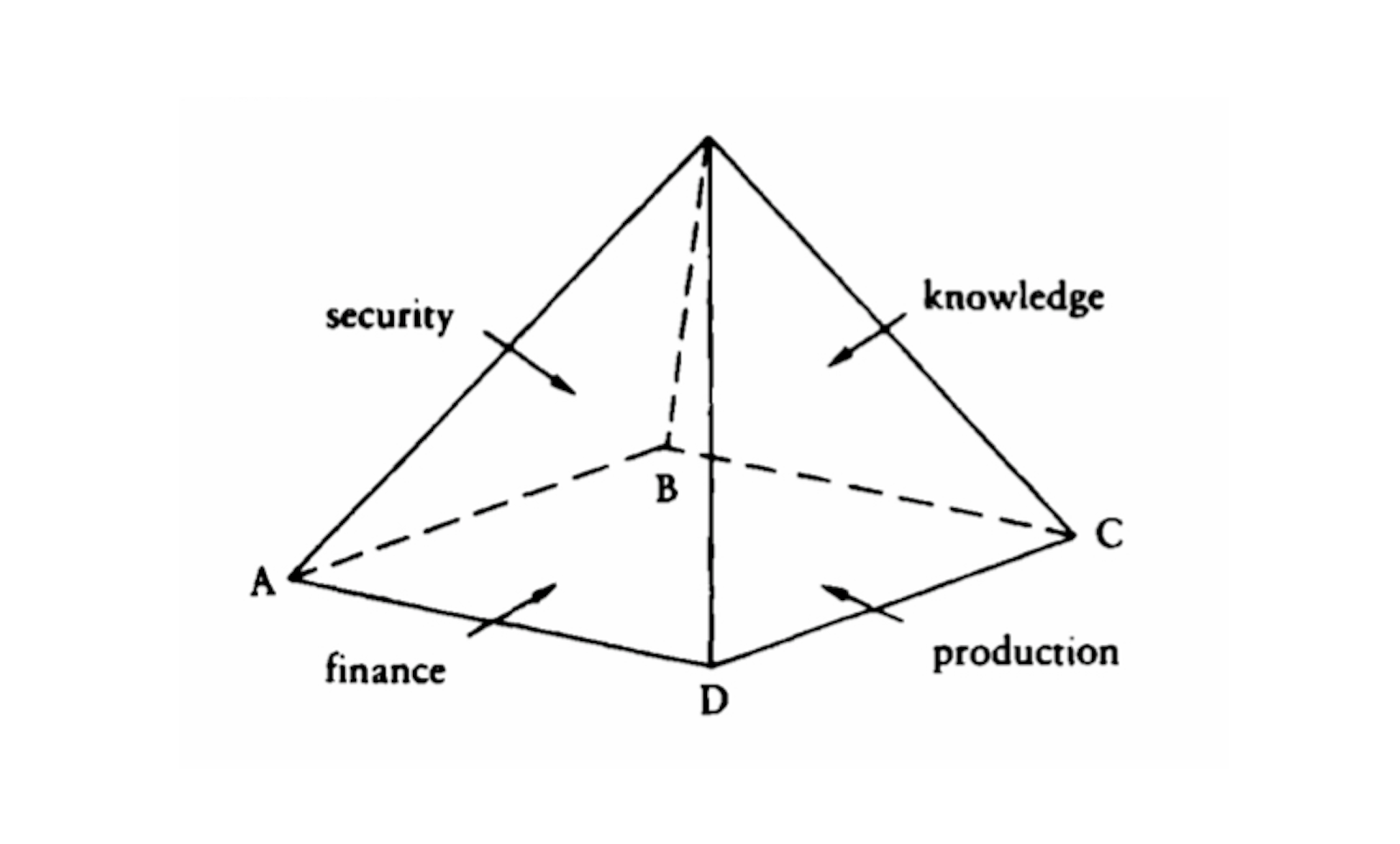

Susan Strange is useful here. Her great contribution was in arguing that international relations, rather than being primarily about military force and geostrategic politics, were a subset of what we now call the international political economy. Resources precede and shape the exercise of violence. Strange also argued that the American empire operated through four sources of structural power: productive power, financial power, knowledge power, and military power. Her refusal to reduce power to a single dimension is helpful in considering imperial systems, because different forms of power are emphasized in different subordinated zones.

When it comes to productive power, we can see clearly that even as US firms remain far more profitable than Chinese ones, physical production is largely dominated by Chinese firms. But financial power pulls in the other direction: the dollar is the central unit of account for credit in global markets, and non-US banks create more dollar-denominated credit in offshore markets than banks in the US create in the domestic market. This is a huge source of infrastructural power that the US retains. In terms of knowledge, American universities used to be the best in the world, but they are now being systematically undermined by federal policy. As the only power with global reach, but with waning deterrence capabilities, the US is “semi-dominant” in military terms—there are now enormous limits to the sorts of wars it can wage.

The dollar and empire

JG: You have argued against the conventional sovereign-currency view of the international monetary system and instead proposed what you call the credit-creation view. Can you talk more about that distinction between these two perspectives and how it changes our understanding of dollar centrality?

HMS: Non-US banks create more dollar-denominated credit offshore as banks in the US create domestically. This is a fact. It is also a fact that the US runs a current account deficit. One’s interpretation of these facts is a function of one’s model of money and one’s theory of money and credit. The sovereign-currency view is the traditional one presented in mainstream economics textbooks. It presents money as a pure asset rather than as an instrument on a balance sheet with a corresponding liability. This is a view that emerges out of a narrative of the past in which gold, the chosen medium of exchange, was deposited in banks before it could then be lent out as credit. The same logic produced the loanable funds model. Savings come first, and then banks simply loan those savings out to borrowers. Scaling this up to the global financial system, the model means domestic savings are shifted from surplus to deficit countries. But the model points you to the wrong indicators of power—towards currency and foreign-exchange reserves rather than credit creation.

This traditional view thinks of savings as the basis of credit, but it ignores where those savings actually came from. The original income that became savings is created by credit! It is generated by businesses that have borrowed money, either long or short term, to buy inputs, including wages. The financial system is not composed of storage units full of cash, but rather a web of interconnected balance sheets in which credit has been created partly by central banks, partly by private banks, and, critically, created out of nothing.

This is called endogenous credit creation. So when banks make loans, they are not taking your savings and handing them out. They are making two balance sheet entries: recording the loan as an asset and the deposit in your account as a liability. Money is created through the act of lending itself. These balance sheets are interlocked, so an American bank might make a loan to a subsidiary in the Cayman Islands, which then makes a loan to Petrobras, which then loans to a local supplier.

What does this all mean for dollar centrality and American power? In the offshore dollar system, non-US banks create huge quantities of dollar-denominated credit, despite not being based in the US. This matters because when things go wrong—and as Hyman Minsky shows, they always do—the asset, or the loan, will be worth less than the deposits, or the liabilities, on the bank’s balance sheet. The bank can either go bankrupt or receive a bailout, but the only place it can receive dollars is the Federal Reserve, via swap lines. (It can’t create dollars itself as it did before because that means adding symmetrical assets and liabilities on the balance sheet, and the crisis means that the existing assets are now worth less than the liabilities.)

You can see why disaggregating the sources of power matters if we want to understand its mechanisms. Where a particular central bank sits in the global credit hierarchy determines its access to dollar liquidity in a crisis. As Steffen Murau has shown, certain countries get greater access to US dollars. At the inner core of the empire are the Bank of England, the ECB, the Swiss National Bank, the Bank of Japan, and the Bank of Canada, all of which have unconditional and unlimited swap lines with the Fed. If they get in trouble, they can borrow dollars easily against their own currencies. Below them in the pecking order are nine countries: Singapore, South Korea, Mexico, Brazil, Denmark, Norway, Sweden, Australia, and New Zealand. These are countries that are important to the US economy in one sense or another, granting them unconditional access to liquidity, though of limited quantity—either $30 billion or $60 billion.

For the rest, more extensive conditions apply. Dollars can be sought by way of the Foreign and International Monetary Authorities (FIMA) repo facility. Here, central banks can temporarily exchange US Treasury securities or American mortgage-backed securities for dollar liquidity. The limitation here is whether the country has treasuries. Without treasuries, they can’t get anything, and to the extent that they have treasuries, they determine how much you can borrow.

The last layer is for those countries that have no treasuries at all. They have to go to the International Monetary Fund and other multilateral lending institutions and beg for charity. The asymmetry is present across all of these relations because it is always the Fed that gets to call the shots. The US Treasury can use access to bailouts to extract concessions from these semi-sovereign systems lower in the global hierarchy. For example, during the Asian Financial Crisis, the US government used access to bailout funds to pry open the Korean financial system, allowing American financial institutions to buy up equity positions in Korean firms and begin lending activities in Korean financial markets. The same thing happened to Mexico during the 1994 crisis.

This entire structure only makes sense once money is understood not as a fixed stock of preexisting savings, but as a system of endogenous credit creation.

MFS: How do you assess the dollar’s position in the global economy today? Has anything about the second Trump administration changed your view of a potential shift in the dollar’s role internationally? What would an inflection point look like?

HMS: There is a lot of talk about the decline of the US dollar at the moment. That originates from the fragmentation of the other three pillars of structural power that Strange highlights. But the dollar remains a relatively stable pillar of power, and in the medium term I don’t see that changing very much.

Predictions of dollar decline often cite the view that the dollar is falling as a percentage of formal foreign-exchange reserves, or else the slightly falling foreign-exchange value of the dollar against other currencies. But these are all less important than the credit question. Over the last quarter century, about 60 percent of global trade has been invoiced in dollars, and 80 percent of trade settlements. So even if you are invoicing in yen, you often will still settle in dollars. This has been extremely consistent for at least twenty-five years.

Between 60 to 70 percent of offshore bank and bond lending is done in dollars, and almost half of foreign exchange trades involve the dollar—which is really almost all of them, because every foreign exchange trade has two sides. That has been constant throughout the Trump administration, although it is possible that the war with Iran could initiate some change to this. US GDP is about 25 percent of global GDP, but the dollar is nearly three times a higher share of transaction volumes. (The euro, by contrast, has a share roughly proportional to the European economy as a whole.) If we want to consider the possibility of dedollarization, we might want to think about how the dollar came to be so dominant as the global currency.

When the Second World War devastated Europe and Japan, those economic zones became dependent on the US for reconstruction, much of which had to be imported—food, oil, machinery. To manage that, Europe set up the European Payments Union (EPU) in 1950. The Americans had mandated the creation of the Union as a condition for receiving Marshall Plan aid. The EPU meant that European countries could avoid trade surpluses against each other, which would have been deflationary. Instead, they could build up credits in the EPU and settle them periodically through a common unit of account that, in practice, everyone understood to be the dollar. The dollar was established as the dominant currency in postwar reconstruction.

Foreign exchange and capital controls soon came to an end, as did the EPU, and European national banks went overseas in search of expansion—the single market was yet to exist—and denominating their loans in dollars. This was one major factor in the rise of the eurodollar market in the mid-1950s. Later, oil shocks reinforced this process, as oil was priced in dollars.

The result was a global system in which balance sheets across the world became heavily denominated in dollars. The flip side of this is that everyone outside the US wants to run trade surpluses because they are demand deficient at home and depend on export-led growth. But if surplus countries were to translate their dollars back into local currency, their exchange rates would appreciate against the dollar, thereby undermining their trade surpluses. To get around this, they instead recycle dollars into financial assets, producing ever larger dollar-denominated balance sheets again. If elites continue to profit from exporting to the American market and holding dollar assets, why would they disrupt this system?

JG: A year ago, the financial press was abuzz trying to discern a logic to the Trump administration’s economic policies, taking particular interest in former Trump advisor, now member of the Fed Board of Governors, Stephen Miran’s policy document published in the run-up to the 2024 election. Miran claims dollar centrality leads to US economic weakness, and that persistent US deficits and an overvalued dollar undermine domestic industry. You have argued, however, that these features are not weaknesses, but structural conditions of dollar dominance. How should we understand the administration’s view?

HMS: There’s an operational coherence to what Trump is doing, but there is no true strategy. Miran and Trump think that deindustrialization is a problem, and they want to combine tariffs with a weaker dollar to solve this. They would like to bring the trade deficit down, but the rest of the administration’s policies are not in line with those aims.

The Johnson and Nixon administrations had a similar concern, and they developed a grand strategy to combat it. In the late 1960s and early 1970s, the US had an emerging trade and current account deficit, and this was perceived as being detrimental to US manufacturing employment. It was clear that the trade deficit was a function of Europe and Japan catching up in mechanical production. Those countries could make the same kinds of cars, but with a lower price point because they had lower wages. In the case of Japan, steel and automobile production actually exceeded American productivity in the 1970s. (This is that typical imperial pattern of peripheries catching up.)

In response, the Nixon shock combined a 10 percent tariff with a 10 percent dollar devaluation, temporarily restoring America’s external balance. But the broader strategy went further—the government accepted that the US could no longer dominate lower-value industrial manufacturing, particularly in sectors like steel and automobiles where unions were most powerful. It opted to move away from competing with Japan and Europe in those sectors, eviscerating the domestic trade unions in the process. It was in the 1970s that the US reoriented the domestic and global economies to new technologies.

The strategy was tied to an effort to reorient the US around sectors in which it had technological leadership. This was the War on Cancer, which turned out to generate a huge investment in biotechnology, and the shift to a smart weapon strategy. They encouraged R&D investment in electronics, pharmaceuticals, and they changed international property rights at both the domestic and international levels. The Supreme Court validated the idea that novel biological entities created with the new biotechnologies could be patented. Congress passed a law making software copyrightable. They created new types of property rights, and generalized these intellectual property laws to the rest of the world in sectors that the US was or could be competitive in.

Stronger copyright protections were great for Hollywood and the software industry. Stronger biotech patents were great for pharmaceutical exports. Agricultural liberalization reinforced US agro-industrial dominance, increasingly tied to biotechnology. All this corresponded to a shift in the American military away from World War II style mechanical weapons to high-tech military strategy built around smart munitions, semiconductors, digital signal processing, and so on. Here, the goal was to maintain technological superiority while reducing dependence on large-scale troop deployments, relying instead on allies and proxies to supply manpower on the ground. This is a coherent strategy, and it is one we don’t see from Trump.

An integrated strategy similarly emerged in the Obama years in response to mounting structural pressures: a huge and growing trade deficit with China, and dependence on oil imports, which by 2008 accounted for almost half of the US trade deficit. The “pivot to Asia” was key to this, as was his move to reduce the ability of the World Trade Organization to adjudicate trade disputes, because the Chinese were now using WTO procedures both to gain access to foreign markets and to shield its own. Obama had a coherent strategy around the military, tech, and trade deficit sides. He ramped up fracking, expanding domestic oil and gas production and transforming the US into a major oil and gas exporter, thereby gaining the upper hand. Europe needs oil. Japan needs oil, China needs oil. Under Obama, the US gained its energy independence, freeing itself from Middle Eastern imports.

For this reason it is completely chaotic that Trump has taken the US back into the Middle East. The administration’s policy is incoherent at the level of building new technologies and new economic capabilities. It undermines the institutional foundation of US technological leadership by attacking universities, public research and scientific funding. Agencies like the National Science Foundation, National Institute for Health, and research arms connected to the CIA and departments of defense and agriculture played a central role in building this technological system.

Trump’s policy is incoherent—one step forward on trade, ten steps back on everything else. If your strategy is simply looking at the exchange-rate value of the US dollar, or foreign exchange reserves as measures of US power, it is focusing on the wrong things. Ever since Nixon took the US out of Bretton Woods, exchange rates have fluctuated constantly. Yet throughout the ups and downs, the dollar has remained dominant. The exchange rate is largely irrelevant. The question is: what’s the unit of account for credit creation?

Global growth waves

MFS: The last decade of political debate and policy shifts in the US can be characterized as reactions to the recognition of decline in productive power. But you’ve argued that the apex of US productive power has actually coincided with deindustrialization, as firms have organized their profit strategies around global productive chains ruled by strong international property rights—capturing a disproportionate share of profits in the US. Can you explain the relationship between globalization, IPR as a profit strategy, and Strange’s “productive power”?

HMS: Recall that Strange argued that the US empire rested on four structural pillars: dominance of production, credit, knowledge, and military power. What happened on the production side was that Veblenian dynamics caused the hollowing out of US manufacturing. Thorstein Veblen argued that what he called industry, meaning actual productive capacity and advances, was in tension with what he called business—the drive for profitability.

Put broadly, the reason we end up with a situation in which US firms have profitability without production, and Chinese firms have production but with minimal profits, is that US firms have reacted to the great labor upheavals and macroeconomic shocks of the 1960s and 1970s by trying to expel as much physical capital and labor from their firms as possible. Meanwhile, those firms became owners of IP—patent, copyright, trademark, brand—and lobbied for greater protection of that IP. For example, Disney secured the extension of copyright to 105 years to protect profits generated by Mickey Mouse.

One result was much higher profits for some US firms: US firms capture a disproportionate share of global profit; within that, IPR firms capture a disproportionate share of that profit. The US is about 25 percent of global GDP, but its firms capture about 35 percent of global corporate profits. Apple and Nike control their whole production chain but in a de facto, not de jure sense. Nike mainly designs shoes and emotions, and lets other firms actually make the product; Apple does software and chip design, but again, other firms do the manufacturing: TSMC makes the main chip, Samsung and STM make memory and gyroscope, Hon Hai assembles everything. Firms at the bottom of the chain face enormous competitive pressure to lower prices and don’t make large profit volumes.

As firms globalized production, what that meant was concentrated profits in the US and concentrated productive activity in China. These patterns are self-reinforcing. The more manufacturing happens in China, the more firms are attracted to its extraordinarily deep pool of supplier firms. And the more US IPR firms are profitable, the more money flows in from other countries to own a piece of the pie, pushing up share prices for those firms, which makes contracting-out the “obvious” model to follow. This has had geopolitical consequences. We might naively think that if you make things, you have power; this is true in a military sense. But in a capitalist economy, what matters most is profitability. The US state has tacitly cooperated with the offshoring of production by making global legal protections for IP stronger, largely to protect those firms that contract out overseas. The WTO agreement on Trade Related Aspects of Intellectual Property Rights (TRIPS) made it possible for American firms in those sectors to become extraordinarily profitable.

All social processes contain contradictions. The US state cleared the path for firms to globalize, and it did give US firms control over much of global production and a disproportionate share of global profits. But it also caused deindustrialization, which had very negative domestic political and increasingly geopolitical consequences.

JG: The neo-Schumpeterian Carlota Perez scholar argues that there have been five technological revolutions since the Industrial Revolution, including the present “Information Age” (beginning circa 1971), now perhaps reaching a point of exhaustion, but definitive of the IP growth strategy. Is a new Schumpetarian growth wave on the horizon, particularly in the rapid expansion of green energy technology? Artificial intelligence? What are the implications of this regime for the balance of global power and the globalized economy?

HMS: For Schumpeter, capitalism is characterized by successive, but not automatic, waves of growth and stagnation. Each growth wave has emerged in response to the exhaustion of the relatively cheap resources driving the prior wave, and has involved five new things: a new energy source, a new transportation mode, a new general purpose production technology, new mass consumer or industrial goods generated by that general purpose technology, and a new form of production organization, or as I would prefer to understand it, a new mode of labor control and exploitation. The neo-Schumpeterians like Perez added a sixth “new”: a new mode of macroeconomic regulation to get supply and demand in balance.

The current or fifth information and communications technology growth wave was built on chips and software, digitalization, fossil fuels, consumer electronics, the internet, and massive vertical disintegration and globalization of production, plus what is often referred to as neoliberal macroeconomic policy. That wave is clearly exhausted. Critically, the cost of producing one transistor gate on a chip is now rising after having been falling for almost fifty years. We’ve depleted the carbon budget. Everyone has a smartphone, so new sales are largely replacement units. There are no more hours available for social-media consumption, and neoliberal governance has produced repeated financial crises and massive income inequality.

Any new wave would have to overcome all those barriers. Non-fossil fuel energy would clearly be a critical part of a new growth package. This might—and I stress might—look something like: renewables as a source of cheap electricity; the electrification of transport; AI and bio-engineering as new general purpose technologies, with AI applied to robotics and protein design; and a return to vertically integrated production. Here is where things become more uncertain: what will a macroeconomically and politically sustainable form of labor exploitation look like in the future? What will global trade and financial networks look like? What legal innovations will anchor profitability the way that protection for IPRs did for the information, communications, and technology wave? What might replace the current US empire of finance and globalized supply chains?

Those are the questions that are organizing today’s global conflicts: between incumbent fossil-fuel producers and renewables producers; between the US and China narrowly and the global North and South more broadly; between owners and workers; and between refugees from what will become climate disaster zones and populations living in less exposed locations. Clearly, technological shifts open the possibility for a shift in the global power structure—battery and drone production are creating new forms of military power; bioengineered substitutes for fibers and plastics will eat into the petro-agricultural system; and so on—but if I had solid answers to these questions I would be talking to my broker, not you guys.

As far as I’m willing to speculate, I wouldn’t be surprised to see a world of relatively disconnected regional economies using regional currencies rather than the dollar, facing some degree of deflationary pressure as the cost of manufactured goods falls dramatically, perhaps with occasional military frictions. Something combining elements of the so-called Great Depressions of 1873–96 and the 1930s, albeit less severe and—I hope—with less revanchist military activity.

Military power

JG: The Stockholm International Peace Research Institute estimates the highest ever levels of military spending around the world today. There is more growth than there has ever been historically in these competing military industrial complexes, though the US still comfortably sits at the top. What has and hasn’t changed about military power and its role in global imperial competition?

HMS: Military spending and capacity never went away as a key pillar of imperial power. But there are some differences today, relative to the height of US hegemony. For one thing, we have overt military conflict at the edge of the inner core—the Russian invasion of Ukraine and the US-Israeli war on Iran.

Throughout the period of American hegemony, we have of course seen coups, election interference, bribes, police action, drones, and some wars, with greater or lesser degrees of visibility. But this is not the same as dropping parachutists on an airfield outside of Kyiv or rolling out tanks along disputed borders. Nor is it the same as blowing up every single bit of military equipment that the Iranians possess—ostensibly in an effort to get a deal the Obama administration already got in 2015. So while I would not say that military spending mattered less in the recent past, its importance has become more overt.

At the same time, the Trump administration has radically devalued American military power in three ways. First, it is burning through a decade of munitions; it’ll probably take ten years to replace them. Second, it has degraded the reputation of its military by demonstrating that those on the receiving end of a US offensive can fight back with relatively simple and cheap systems. One of the phrases currently going around is that the Americans are using Ferraris to shoot down frisbees, meaning million-dollar missiles are deployed to shoot down thousand-dollar drones. Insurgency can now extract a price from empire in terms of weapons systems; the entire radar infrastructure in the Gulf has been destroyed.

Third, deterrence is practically gone. Military spending is going up because the Koreans are seeing that the Iranians were able to destroy the interceptors that they will rely on to shoot down a nuclear-tipped North Korean missile. Remaining American interceptors are vulnerable to cheap weapons systems, which the Chinese can produce en masse. So a massive production increase is being planned across the board. The Japanese are legalizing sales of offensive equipment to other countries in order to build their own armaments industry and integrate regional actors into their military system. Canada is gesturing towards a similar direction with its new EU-focused rearmament plan.

Countries are thinking harder about nuclear weapons. The Americans under Biden could have been much more forward in supplying Ukraine with long distance weapons, but didn’t for fear, among other things, of Russian nuclear capabilities. Instead, the US is messing around with non-nuclear powers—Libya, Iran, Iraq. All incentives point towards those who can developing nuclear deterrence capabilities for self-insurance. To be a bit flip about it, most countries are perfectly capable of building nuclear weapons. The Israelis have them. The South Africans more or less built them and were then shut down. Brazil and Argentina were halfway. The technology is from the 1940s; the only barrier is whether they can get enough enriched uranium—frankly, one would be foolish not to. And that is a terrifying situation.

MFS: We’ve discussed moments in which the US has reshaped the global order. Today, many see the Trump administration as accelerating a change in the world order in ways that appear self-undermining—you’ve even joked that it is suicidal. Yet these same expressions of force seem to underline the US’s unparalleled power. To what extent can one administration damage such rooted structures of empire?

HMS: Empires typically do not collapse because of external aggression. They collapse because of some form of suicide. Going back to the discussion of elites, Trump is an extreme example of a cadre beginning to think about its own personal wealth at the expense of the big picture. But to what extent is the effort to create an inflection point purely a product of Trump? These efforts clearly predate him, as do the contradictions that led to his electoral victory. Trump did not cause the inflection point, but his actions will direct its outcomes.

But in terms of empire, this could take a very long time to play out. The downstream effects of the US university system collapsing, for example, are measured in decades, not weeks. While military credibility has been destroyed, the US remains the only force with logistical as well as command and control capacity to run a global war. It is possible that the Mad Emperor dies, a saner president is elected, and there’s some restoration.

As Edward Luttwak’s book on the Byzantine Empire argues, the essence of Byzantine strategy was simple: don’t get into a war you’ll lose because it will destroy the empire. He wrote it largely as a warning to the American defense and foreign policy rulers in the context of the Iraq War. The war with Iran today is even more stupid. Part of the problem lies in Trump himself being an erratic and idiotic decision maker, but the present configuration reflects the pressures of the vast social forces around him: the oil industry, the defense industry, Iran hawks, and so on. So I do think there is justification for saying this is an empire on suicide watch: the leadership at the center is actively undermining the very foundations of American power.

Further Reading

The Nokia Risk

Small countries, big firms, and the end of the fifth Schumpetarian wave

In the early 2000s, Finland was the darling of industrial and employment policy analysts everywhere. This small country with a population of 5.5 million and...

Brave New World

A third industrial divide?

Endogenous dynamics have crippled the current growth wave that began in the 1980s—yielding the period of decay in which we are now living. Rather than...

The Dollar and Empire

How the US dollar shapes geopolitical power

What does the US dollar’s continued dominance in the global monetary and financial systems mean for geo-economic and geo-political power?