Analysis

The Economic Consequences of the War

The Hormuz shock, inflation targeting, and the prospects of a new cycle of global monetary tightening

As negotiations and a so-called tenuous ceasefire place the war on Iran in a holding pattern of destruction and misery, it can seem misguided to focus on the economic effects for societies far from the conflict. But the prospects of halting further escalation may hinge on the interests affected by the widening radius of economic devastation—including the ruling classes in the capitalist core.

The current wave of imperial aggression has elicited little opposition from these corners, in part one of its effects has been to further redistribute wealth upward. When the oil trade is disrupted, many oil giants increase their leverage, able to raise their profit margins as buyers scramble to buy any available barrel. This is what Isabella Weber and Evan Wasner, borrowing a concept from Abba Lerner, have described as “sellers’ inflation.” As they have shown, the distributive impacts of the 2022 energy crisis triggered by the war in Ukraine worked to the benefit of the United States, as US headquartered companies responded for about a third of the total net income made by publicly listed oil and gas companies in that year.

The winners were those at the very top: more than half of the 2022 oil profits were appropriated by the richest 1 percent of individuals, while the bottom half of society managed to capture just 1 percent of the total. An obscene imbalance: 50 percent to the top 1 percent, 1 percent to the bottom 50 percent. In a series of recent pieces written with Gregor Semieniuk, Weber has been making the case that, in the absence of a radically different policy response, the current war in Iran is bound to yield similar results.

Since oil is a systemically significant sector, its price affects that of many other goods and services. Any change quickly influences the overall rate of inflation and pushes central banks to act. The conventional tool of monetary authorities—an increase in interest rates—will do little to address the energy crisis. It merely shifts the burden of adjustment towards the working classes, increasing unemployment to soften demand and try to mitigate the rise in the price level.

In regions of the global periphery like Latin America, interest rates tend to rise even further, as countries scramble to defend their currencies from the drying up of global liquidity. In these economies, the impact of monetary policy on unemployment is often less pronounced, but higher interest rates still bear a class character: they boost the rentier share of income, transferring more and more revenues collected by regressive tax systems towards the rich, while deepening the debt bondage of the vast majority. Throughout the North and the South, then, oil shocks lead to upward redistribution of income and wealth, both directly via oil profits, and indirectly via the effects of monetary policy.

Could alternative policies, beyond the inflation targeting regime, remake this calculus, shielding those at the bottom and shifting burden to the top? Were such measures put in place, wars may no longer promise such easy profits and financial returns, and the forces that have been driving them could perhaps be weakened.

This column will briefly discuss the theoretical reasoning behind conventional monetary policy which tends to offer the same solution to any price shock. It will then examine the reaction of central banks to the 2022 energy crisis, both in rich countries and in Latin American countries with consolidated inflation targeting regimes (Brazil, Chile, Colombia, Mexico, and Peru, according to CEPAL’s classification). This will help to shed light on our present situation, illuminating what could happen over the coming months if states double down on the same strategy.

Wage inflation

Mainstream economic theory has provided ammunition for an anti-worker monetary policy for more than half a century by focusing on a particular interpretation of inflation encapsulated in the “Phillips curve.” In the 1958 article that began this discussion, the economist A. W. Phillips was not concerned with price inflation, but rather with the relationship between unemployment and changes in wages. His analysis centered on the very plausible argument that low unemployment strengthens workers’ bargaining power, creating conditions for wage increases. “When the demand for labour is high and there are very few unemployed,” he wrote, “we should expect employers to bid wage rates up quite rapidly, each firm and each industry being continually tempted to offer a little above the prevailing rates to attract the most suitable labour from other firms and industries.”

In 1960, when Paul Samuelson and Robert Solow named a curve after Phillips, they made a crucial alteration to his analysis. The relationship they interrogated was not the one between unemployment and wage inflation, but rather between unemployment and inflation as a general rise in the price level. The underlying assumption was that, whenever tight labor markets pushed nominal wages up, firms would simply translate these higher costs into higher prices. In this model, workers’ power to appropriate a larger share of income was effectively contained by the market power of firms. And, critically, inflation was seen as fundamentally driven by wage inflation.

To make matters clearer, it is useful to compare this view with a contrasting one put forward by Richard Goodwin in 1967. In his model, Goodwin assumed the original Phillips empirical relationship (between unemployment and wages), abstracted from price changes. As a result, the model shows that during booms, when the industrial reserve army of labor is depleted, workers squeeze profits. The ensuing crisis restores the surplus population and, with it, profits. Business cycles, in this reading, are cycles of profitability and unemployment.

In contemporary capitalist economies, abstracting entirely from inflation—as Goodwin did—is misleading, as distributive struggles are partially reflected in changes in prices. But Samuelson and Solow’s Phillips Curve went too far in the other direction, assuming away the possibility of workers increasing their real wages—thus abstracting from cyclical profit squeezes. In so doing, they laid the groundwork for the argument that it is not harmful to workers for anti-inflation policy to operate through the labor market, as their attempt to push for higher wages must be futile, with nominal wage increases fully compensated by inflation.

Samuelson and Solow were writing at a time when macroeconomists believed their main challenge was to guarantee full employment. The shadow of the 1930s mass unemployment and its political consequences—fascism first and foremost—still loomed large. With their Phillips Curve, they suggested that full employment was achievable but may come at a cost in terms of inflation. Policymakers, they said, had a ‘‘menu of choice:’’ low unemployment with higher inflation, or low inflation with higher unemployment.

In the late 1960s, Milton Friedman and Edmund Phelps challenged this view, claiming that once governments started taking advantage of the menu, inflation expectations would be adjusted, and inflation itself would climb higher. Their work marked the abandonment of full employment as a goal of macroeconomic management. From then on, the aim of keeping unemployment close to its “natural rate,” as Friedman called it, became increasingly widespread. Some unemployment was seen as unavoidable—or, at least, not subject to macroeconomic policy. To lower its “natural rate,” governments would need to resort to other measures, mainly slashing labor rights. The policy shift was dramatic. Price stability, rather than full employment, was the focus of economic policy, and employment policy meant structural reforms to labor market institutions.

The Friedmanian turn in monetary policy consolidated a narrow view of inflation, inherited from Samuelson and Solow, according to which it is simply driven by wage inflation. The inflation targeting that became hegemonic in the 2000s—that is, the policy regime in which central banks change interest rates to try to meet a pre-defined target for the inflation rate—adopted precisely this theory. From this perspective, every time inflation increases, even if it’s driven by, say, an oil shock from abroad, the only possible solution is to increase unemployment to reduce wage inflation, and thus bring inflation back to the target.

In a recent influential analysis, Olivier Blanchard and Ben Bernanke asserted that “pandemic-era inflation was due primarily to supply disruptions and sharp increases in the prices of food and energy.” Yet the policy implications they draw seem curiously unaffected by this: “returning price inflation to target may require a period of modestly higher unemployment.” Though they do not interpret the recent inflation as the proverbial nail of excess demand, they cannot help but argue that the solution is the hammer of unemployment-inducing rate hikes.

If inflation was usually caused by tight labor markets, inflation targeting would work well enough on its own terms. But with inflation much more clearly resulting from supply shocks—geopolitical or climate-related—the limits of traditional inflation theory are more apparent, and the need for alternative theory and policy more pressing. One could start by examining the four different drivers of inflation, as Lance Taylor and Nelson Barbosa-Filho have suggested: wage costs, profits, import prices, and indirect taxes.

Once inflation is seen in this light, we can imagine a variety of policies to address oil crises or other price shocks: from taxing windfall profits to nationalising the energy sector, from targeted price controls to planned decarbonisation. The question then becomes political: how will the higher cost of oil be shared between workers, oil-consuming industries, oil companies, and the government? There is no easy answer. Yet a carefully designed policy mix could plausibly attenuate the impact of shocks on the most vulnerable at the same time as it increases the long-term resilience of the economy and addresses the climate crisis.

Blaming the victim

In 2022, how did rich countries deal with the energy shock triggered by the Russian invasion of Ukraine and the subsequent sanctions on Russia? Faced with higher inflation as a result of Covid-induced supply disruptions, central banks initially tried to wait it out in the hope of a quick reversal; they knew that their usual tool—interest rates—was poorly suited to the task at hand. And they feared that raising interest rates amid the fragile post-pandemic recovery could trigger a sudden decline in asset prices that threatened financial instability. Indeed, after more than a decade of purchasing assets in large quantities to prevent deflation when interest rates had hit the so-called zero-lower bound, central banks were now overseeing yet another asset bubble and compelled to act as market makers of last resort.

At this point, however, a powerful deflationary bloc mobilized inflation hawks to push monetary authorities into action. They argued that a slow reaction from central banks could unmoor inflation expectations, which had been firmly anchored by decades of carefully following the inflation-targeting script. Once that anchor was lost, prices and wages would spiral upwards in a rerun of the stagflation of the 1970s, and control of inflation would be lost. Beyond managing expectations, they claimed, tight monetary policy was needed to contain the second-round effects of the oil price shock, preventing its diffusion throughout the economy.

These technical arguments generally ignored the ineffectiveness of the interest rate as a tool. Surely higher rates in New York, London, and Frankfurt would not bring the war in Ukraine to an end, and would thus fail to address the ultimate source of inflation. Nor would they have a significant effect on energy demand that could moderate the increase in prices. So insisting on restrictive money policy as a response to a supply shock essentially meant managing the average: as the oil and gas prices were not expected to fall, bringing inflation back to the target required that the prices of other goods and services were cut in real terms.

This cut was supposed to be accomplished through the medium of the labor market, as discussed above. Increasing unemployment and reducing the bargaining power of workers, who would shoulder the burden while profit margins remained shielded. It was rare for this disinflation strategy to be openly acknowledged, since its effects are so naturally unpopular, but there were exceptions. In 2022, Andrew Bailey, governor of the Bank of England, declared that workers needed to contribute to the disinflation effort by moderating their wage demands. Without “restraint in pay bargaining,” he said, inflation “will get out of control.” Blaming the victim?

To be sure, governments did not leave the job exclusively to central banks. In many countries, a set of measures was introduced to soften the blow. The United Kingdom and the European Union imposed energy price caps, with Westminster funding them partly through windfall profits on oil firms. But the inflation hawks prevailed, and these policies were largely offset by the usual interest rate hike.

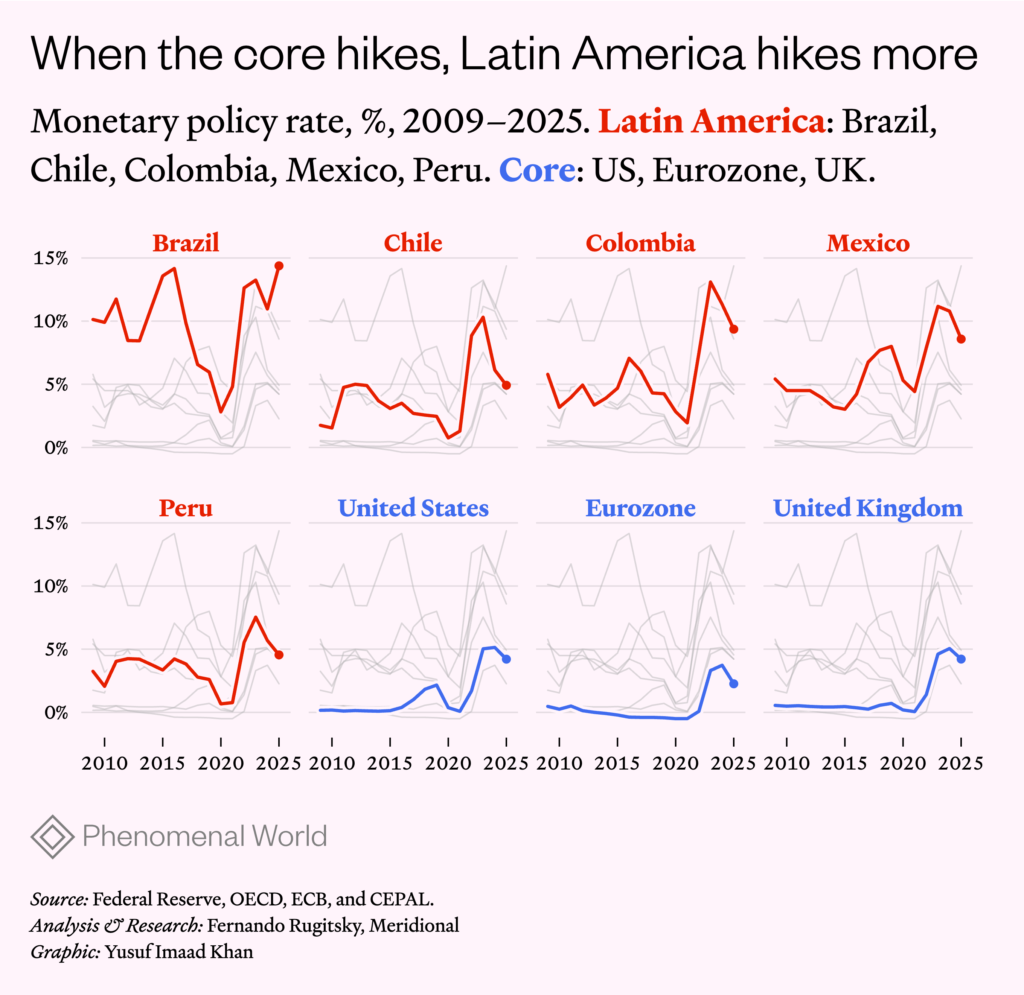

By mid-2023, a little more than a year into the war in Ukraine, the policy rate in the US and the UK climbed from just over zero to 5 percent. In the eurozone, the policy rate peaked at 4 percent—a figure without precedent since the introduction of the common currency. The effects on the labor market were predictable: in the US, the unemployment rate trended up from 2023 onwards, while in the UK it continued the upwards trajectory that had started in the preceding year. Central bankers once again made Friedman and Phelps proud.

Rentiers’ paradise

This abrupt monetary contraction inaugurated a downward phase in the global financial cycle. At moments like this, as Adam Tooze argued at the time, monetary policy reflects a bandwagon effect: “Once the Fed moves and the dollar strengthens, other countries either raise their interest rates or face a sharp devaluation, which further stokes inflation.” This time, however, we witnessed nothing short of “the most comprehensive tightening of monetary policy the world has seen.”

The Latin American inflation targeters moved decisively. In Peru and Chile, policy rates that were below 1 percent in the aftermath of Covid jumped up to, respectively, 7.75 percent and 11.25 percent by 2023. In Brazil and Colombia, the post-Covid trough had been a bit higher at, respectively, 2 percent and 1.75 percent, while the tightening took rates above 13 percent by 2023. In Mexico, the increase was from 4 percent to 11.25 percent. At one level the strategy seemed to work, albeit at a huge fiscal and distributive cost. While the dollar appreciated globally in 2022, reaching a “20-year high,” the Brazilian real, the Mexican peso, and Peruvian sol bucked the trend, becoming stronger relative to the dollar. In Chile and Colombia, the currency depreciated but less so than in many other peripheral economies. Having avoided massive depreciations, these Latin American economies reaped the benefits in terms of their inflation rates. Between 2021 and 2022, the average inflation rate fell in Brazil, rose only moderately in Mexico and Peru, and reached double digits only in Chile and Colombia.

In the rich countries, higher policy rates are expected to disincentivize borrowing by firms and consumers, reducing demand and weakening the labor market. In the periphery, meanwhile, structurally higher interest rates, segmented credit markets, and the relatively more restricted role played by borrowing mean that this transmission channel is weaker. Monetary policy hopes to impact inflation mainly through the exchange rate, managing inflows and outflows of capital. In fact, disinflation, as estimated by CEPAL, took place in both Brazil and Mexico without output deceleration between 2022 and 2024. In Colombia and Chile, by contrast, depreciation pushed demand downward, reducing inflation in the usual way. (Peru was the exception in this case, avoiding depreciation but facing an output deceleration.)

Is it therefore possible to say that, in the case of Brazil and Mexico, monetary policy did not displace the negative effects of the shock onto workers? Not really. The upward redistribution in this case was not driven by capitalists taking advantage of the weak labor market but by rentiers boosting their income through their holdings of government bonds and the expropriation of indebted workers. (In peripheral economies, the labor market tends to be structurally weaker than in core economies, given the more significant share of precarious work contracts and widespread informality. The point is simply that monetary tightening in 2022–2023 did not make the labor market significantly weaker than it was in 2021.)

An increase in interest rates is usually assumed to have a negative impact on the assets of those holding public debt, as it reduces the market value of existing bonds with pre-fixed rates. However, in the Brazilian case, not only does a significant share of public bonds have floating rates, which means they are positively impacted by monetary tightening; the structural maintenance of extraordinarily high interest rates also creates abundant opportunities for the rich to capture higher and higher shares of the tax revenues. Thus, in financially subordinated economies, when monetary policy managed to defend the value of the currency in the aftermath of the 2022 shock, workers were both directly and indirectly expropriated by the rentier class, even as the labor market was preserved. These Latin American economies can only develop less deleterious methods to deal with price shocks if they manage their capital accounts in a way that reduces their vulnerability to the global financial cycle.

Hormuz and the rich

Will 2026 resemble 2022 when it comes to inflation and redistribution? The magnitude of the shock from the blockades of the Strait of Hormuz appears to be larger than the one caused by the war in Ukraine. The extent of its impact depends on how long the blockades last and how policymakers respond to the unfolding disruption. In terms of headline prices of systemically significant goods, the comparison is unavoidable: as soon as the attacks started in March, the price of oil leapt above 100 dollars, just as it did in 2022. And it is not just oil: major disruption has also affected the supply of natural gas, fertilizers, helium, sulphur and many other commodities.

Rising prices will once more pose the question of whether conventional inflation targeting is up to the task. If central banks decide that it is, they will likely put a stop to the ongoing monetary easing that began in 2024, once again shift the burden onto workers while failing to deal with the immediate emergency or its ultimate origins.

In Latin America, much depends on foreign exchange markets. Even economies like Brazil and Mexico that could benefit from higher prices earned from their oil exports would still be disrupted if the shock results in a reversal of the global financial cycle. So far, the Brazilian and Colombian currencies have appreciated, but the Peruvian one has depreciated slightly. Exchange rate turbulence and more significant depreciations have been confined to Chile and Mexico. If Northern central banks opt for contraction, depreciation pressures will likely spread throughout the region, and central banks will hike interest rates, channeling hard won tax revenues towards the rentiers—while the poor foot the bill of another distant war.

Further Reading

The Political Economy of Brazilian Inflation

The implicit income policy of central bank inflation targeting

A jabuticaba financeira

Selic altíssima e câmbio desvalorizado: uma análise sob a ótica da dominação rentista no Brasil

Controlling Capital

Inflation targeting and external vulnerabilities in the Brazilian economy

Further Reading

The Political Economy of Brazilian Inflation

The implicit income policy of central bank inflation targeting

Over the past two decades, Brazil has seen two great swings in its distribution of real national income. In the years between 2004 and 2014,...

A jabuticaba financeira

Selic altíssima e câmbio desvalorizado: uma análise sob a ótica da dominação rentista no Brasil

A hegemonia financeira que rege o país resulta de uma trajetória institucional singular em relação às práticas usuais de outros países, a ponto de se...

Controlling Capital

Inflation targeting and external vulnerabilities in the Brazilian economy

Central banks are back in the spotlight. After more than three decades of low inflation in rich countries, the rise in prices observed between 2021...