Analysis

Drowning in Debt

Financial inclusion and financial expropriation in Brazil

The upcoming presidential election in Brazil, set to take place in October of this year, will for a third time pit Luís Inácio Lula da Silva’s Workers’ Party against the far-right movement led by Jair Bolsonaro. Lula is running for reelection at the end of his third term as president, campaigning on the back of a relatively successful macroeconomic performance. After a long period of crisis and stagnation–average annual GDP growth between 2015 and 2022 was 0.3 percent–the Brazilian economy grew about 3 percent per annum in the first three years of the current government, and the unemployment rate declined from 9.5 to around 6 percent (comparing the averages for 2022, the last year of the preceding government, and for 2025).

Yet the polls are suggesting that this won’t be enough to guarantee an easy reelection. Most of them are predicting a close race between Lula and Flávio Bolsonaro, the eldest son of the former president, who is currently serving time for an attempted coup. The resilience of bolsonarismo has prompted critical engagement with lulismo’s strategy, pushing the debate beyond the macroeconomic headlines to examine the longer-term impacts of the policies adopted by the Workers’ Party. In this regard, popular indebtedness has been foregrounded as a key issue, with rising incomes at the bottom being immediately transferred to creditors at the top, leaving little room for improving living standards–vindicating those like Lena Lavinas, who has been for years sounding the alarm on mass-based financialization. The undeniable benefits of financial inclusion, which widened access to basic appliances like fridges and washing machines, have recently been overwhelmed, in the public’s perception, by the costs of financial expropriation.

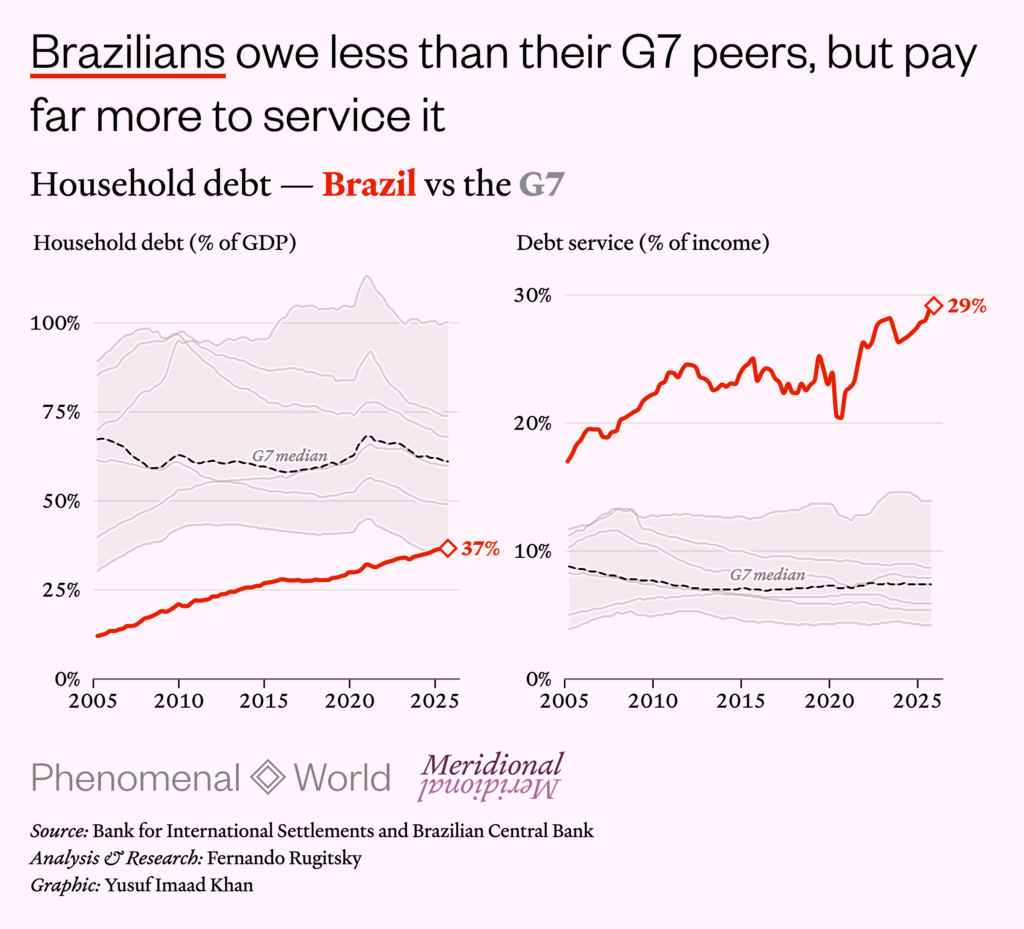

It would certainly be an exaggeration to attribute the current electoral uncertainty to consumer credit policies. But analyzing them in detail can illuminate a problematic feature of the Workers’ Party attempt to promote inequality-reducing economic growth. Doing so can also illustrate how the global boom in lending to households has particular effects in the global South, as consumer credit policies interact with international financial subordination and the resulting high and volatile interest rates. Substantially lower levels of indebtedness (as a share of GDP) relative to other countries tend to correspond with extraordinarily high shares of income being used to service debt obligations, due to the expensive credit.

As the figures below show, Brazil’s household debt-to-GDP ratio only recently surpassed 30, whereas the ratios for the G7 countries (except Italy) usually stand between 50 and 100. Nevertheless, the opposite ranking can be seen regarding debt-service-to-income ratio: while in the G7 countries, it stands between 5 and 15, in Brazil it has been close to 25 since the 2010s and recently approached 30. It is important to mention that institutional diversity limits the international comparability of these ratios, but there is little doubt about the overall picture. To grasp its significance, it is useful to chart the rise of workers’ indebtedness in a bit more detail.

Uneven and combined

The worldwide boom in household borrowing has its origins mainly in the United States and the United Kingdom in the 1980s, when squeezed workers started to rely on larger quantities of debt from simultaneously squeezed commercial banks. The latter had been losing one of their main sources of funding, as higher-earning individuals started shifting their balances from bank accounts to “mutual, pension and money-market funds” to take advantage of tax benefits and higher returns. At the same time, non-financial firms also diversified their sources of credit, raising money without the intermediation of commercial banks. In the case of the US, banks were also struggling due to the pressures on the mortgage business stemming from the Volcker shock, which had already brought down the so-called savings-and-loan banks.

Short on funding and losing many of their borrowers, these banks badly needed alternative sources of revenue. As Paulo dos Santos explained, they turned to “investment-banking services to corporations,” “retail brokerage services,” and “household credit.” On the other side of these deals were the workers, facing the triple whammy of jobs being relocated to East Asia, governments committed to weakening unions, and increasingly commodified access to basic goods and services, like education, health and housing. With stagnated wages, they depended more and more on borrowing to make ends meet.

According to data from the Bank for International Settlements (BIS), the household debt-to-GDP ratio, which in the 1970s oscillated around 30 in the UK and 45 in the US, rose continuously in both countries to peak at just under 100 during the great financial crisis of 2008 (see figure above). Canada charted a similar path, while France saw its ratio triple in the same period, though it only surpassed 50 in the run-up to the 2008 crisis, having started at a much lower level. Germany and Japan also experienced the workers’ indebtedness boom, but their ratios peaked earlier, at the turn of the millennium, around 70.

With the adoption of the euro, economies in the European periphery (Greece, Portugal and Spain) joined the trend, with the household debt-to-GDP ratio surging in the 2000s. In Asia, the boom in Korea and Thailand also took the ratio close to 100 during the pandemic, and the ratio’s rise in China was likely one of the fastest globally, tripling in a decade to peak at just over 60 in 2020. BIS data for Latin America is more limited, but a rise in the mentioned ratio can be clearly seen in Brazil, Chile and Colombia–they remain, however, at a lower level (Chile’s peaked at just under 50 in 2020, Colombia’s around 30 in the same year, and Brazil’s is still rising, approaching 40).

Such a quantitative increase was premised on qualitative transformations in the banking sector. Credit relations based on long-standing local relationships between banks and borrowers were replaced by concentrated operations based on quantitative credit ratings and done at scale, contributing to the ongoing consolidation of the banking sector. Besides, large-scale securitization meant that lenders did not need to keep risky assets in their balance sheets but could pass them forward as securities to institutional investors and shadow banking firms. In the process, large US and European banks not only increased their market share in their economies but also expanded to the global South, seizing additional profit opportunities. For this effort, they counted on the helping hand of the World Bank, which had been pushing for the liberalization of the financial sector in peripheral countries, particularly for the opening of their markets to foreign banks. In the cases of Brazil and Mexico, for instance, those foreign banks led the way in the increase in household credit–even if domestic banks remained dominant, as they did in Brazil.

The changes in the supply of, and demand for, credit soon acquired macroeconomic relevance. In Robert Brenner’s influential interpretation of the period, governments tried to counteract the long downturn resulting from global manufacturing overcapacity and falling profit rates by stimulating asset-price bubbles that could boost consumption. The mechanics of this bubblenomics was the following: Rising asset prices, especially house prices, increased the collateral that households could offer to borrow more money. When they borrowed in order to buy houses, they pushed their prices further up, creating a cumulative process. As Chen and his co-authors showed, more than 60 percent of the mortgage refinancing operations done in the US between 1985 and 2013 increased the total borrowing by at least 5 percent, indicating that borrowers were cashing out or, as they put it, using their houses ‘‘as ATMs.’’

Brenner’s analysis remains controversial, but the fact that governments deliberately pushed workers into debt traps is much less so. Sometimes, as in Colin Crouch’s concept of privatized Keynesianism or in the post-Keynesian argument about debt-led growth, workers’ indebtedness compensated for rising inequality and stagnant wages, attenuating the downward pressure on the demand for the goods and services produced. It dealt, in other words, with Marx’s realization problem. Others, such as Wolfgang Streeck, highlight political legitimacy rather than economic performance: private debt was thus interpreted as a third attempt by capitalist democracies to buy time, transitorily avoiding explosive distributive conflicts. Through borrowing, workers could maintain to a certain degree their expected living standards at the same time as their stagnant wages guaranteed rising profits for the capitalists. Win-win–before it all came crashing down, causing a worldwide crisis.

Lulismo and workers’ indebtedness

In the South, government policy was also crucial to stimulate indebtedness, but both the mechanics of the cycle of debt and the rhetoric supporting it were different. The case of Brazil helps illustrate these particularities. Credit operations to individuals as a share of GDP had been increasing since the 1990s but from 2004 onwards the rise picked up speed, due to both falling interest rates and a direct policy push.

Lula’s first electoral victory, in 2002, took place amidst a speculative attack, as capital aimed to discipline the Workers’ Party into preserving the neoliberal strategy of the outgoing government. The capital flight meant massive currency devaluation and an increase in inflation, pushing the central bank to hike interest rates–the nominal policy rate reached 26.5 in February 2003. From then on, however, the boom in commodities’ prices and capital flows gradually appreciated the real, bringing inflation down and opening the way for the central bank to reduce the interest rate. The real policy rate (that is, discounting inflation) fell from an average of 12.8 in 2003 to 3.7 in 2010, as Lula concluded his second term.

Hoping to bring down the actual borrowing rates faced by workers, the government authorized in 2003 the crédito consignado, that is, credit lines with automatic deduction from the paycheck. This entailed significantly lower credit risk to lenders, especially in the case of public servants and pensioners, who, up to 2025, responded for more than 90 percent of total outstanding credit in this modality. In many ways, crédito consignado fits perfectly with the weak reformism that characterizes lulismo. It widened the access to basic consumption goods, reducing inequalities in living standards, but it avoided confronting the interests of the ruling classes, circumventing deeper redistributive efforts. It boosted financial institutions’ profits at the same time as it stimulated consumption and economic growth, increasing tax revenues and opening the way to increasing social transfers (mainly conditional cash transfers and pensions). It was an expansionary policy that could complement more conventional fiscal policy measures, which were constrained by fiscal targets.

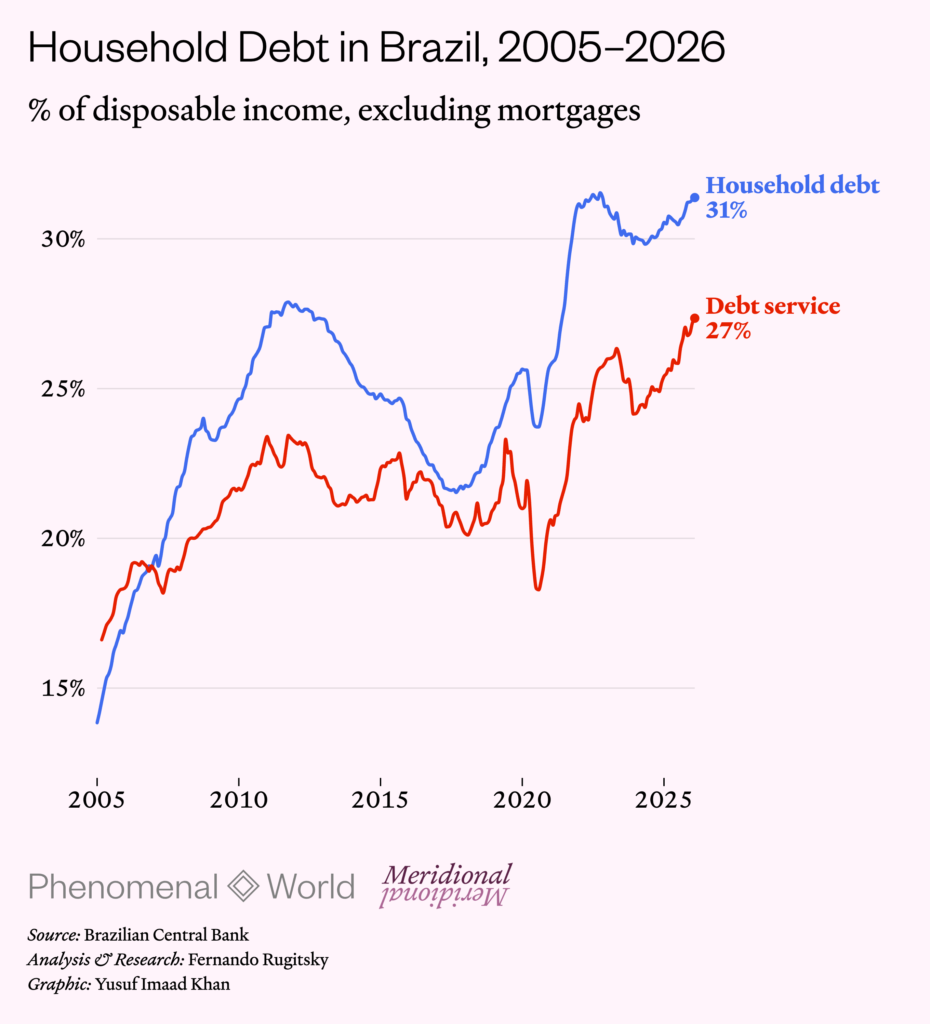

The effect was clear. Between 2005 and 2011, household debt as a share of disposable income, excluding mortgages, doubled from 15 to just under 30. As a consequence, the flow of interest income in the Brazilian economy was transformed. As Pedro Marques and I have shown, before the indebtedness boom, more than two-thirds of the intersectoral interest payments–that is, net interest payments from the main institutional agents (financial firms, non-financial firms, government, indebted households, lending households, and non-residents)–were made by the government, who was the main borrower in the economy. By the end of the 2000s, indebted workers displaced the government as the primary borrowers, becoming responsible, on average, for almost half of the interest payments between 2008 and 2011, pushing the government’s share down to 47.6.

One of the celebrated achievements of the Workers’ Party in the 2000s was an increase in the wage share of income, that is, the share of GDP appropriated by workers. Between 2005 and 2011, it rose from 46.2 to 48.1 percent, on the back of labor market formalization and minimum wage increases. However, once this share is adjusted for interest payments, the trend is inverted: the wage share net of interest actually fell from 44.1 to 42.2. Financial expropriation more than compensated for the labor market improvements.

Mass consumption in Brazil, mass production in China

One could give lulismo the benefit of the doubt and consider workers’ indebtedness in a different light. It could be argued that the government was not the leading force behind the rise in borrowing, which was mainly a result of the global financial cycle, but simply aimed to adopt policies–like the consignado–that helped workers access cheaper credit. Besides, instead of focusing on the aggregate wage share and the macroeconomic consequences of financial expropriation, one could highlight the transformation in the daily lives of the workers who used credit to buy their first fridge, washing machine, or smartphone, which might allow them to increase their income. For example, in an interview carried out by researchers in Jardim Helena, a neighborhood in the periphery of São Paulo, one person reported, ‘‘I spend my days on WhatsApp talking to my clients. I’m self-employed [as an electrician and bricklayer], and I depend on my phone for my work.’’ Another added: ‘‘I get all my cake orders on a Friday. They come to me via WhatsApp. It’s great because the mobile phone has boosted my income.’’

Crucially, the process of financial inclusion could be seen as part of a larger development strategy that connected diversified mass consumption to the transformation of the productive structure. As those at the bottom were given access to a larger range of goods, they could push the economy to adjust accordingly, creating better employment opportunities and unleashing a virtuous cycle linking the structures of demand and supply. This view was articulated by Ricardo Bielschowsky, who argued that mass consumption should be one of the drivers of a development strategy for Brazil. He hinged his hopes on the fact that ‘‘mass consumption goods are produced by modern productive and corporate structures that are conducive to technical progress and productivity gains.’’ In this scenario, the debt extended to the workers would not grow unsustainably, but create conditions for its own obsolescence. As workers’ employment conditions improved, they would be able to pay back what they had borrowed and reduce their indebtedness level.

Such expectations were based on a specific understanding of what had happened during the so-called Brazilian economic miracle of the late 1960s and early 1970s. At that time brutal repression of unions and an abrupt reduction of wages were the means used by the military dictatorship to restore profitability. A substantial part of the investment boom that ensued was driven by the production of cars and electrical appliances, the demand for which was premised both on upward redistribution and on abundant consumer credit–extending access to those goods to the upper middle classes. Thirty years later, developmentalist economists came to believe that the unequalizing spiral of the economic miracle could be inverted, as modern consumption goods were no longer restricted to the rich but could also be accessed by the poor. There was, though, one important risk, which Bielschowsky himself was concerned about: ‘‘will mass production stimulated by mass consumption be undertaken in the country or will we have mass production in Brazil and mass production in China?’’

A second wave of indebtedness

In hindsight, it is clear that the virtuous transformation of the productive structure did not take place and that mass consumption did not alter the ongoing process of regressive specialization of the Brazilian economy. The more sophisticated goods that were being bought in droves during the mass consumption boom were, in the best cases, simply assembled in Brazil. More often, they were imported ready-to-use, usually from China.

The result was that the indebted workers did not have many opportunities to transfer to jobs with higher pay, which could sustain their higher consumption standards. In fact, they had to make do with low-paying employment in construction and basic services, the industries with the vast majority of job openings in the period of growth acceleration in the 2000s. Their debts, therefore, could not be paid back, but grew faster than income, increasing the share of their disposable income that went straight to creditors. Debt-service-to-income ratio (excluding mortgages) climbed from 16.6 to 23.4 between 2005 and 2011 (figure below–in contrast to the two earlier figures, the data in the one below exclude mortgages).

Between 2011 and 2013, Lula’s successor to the presidency, Dilma Rousseff, engaged in the so-called ‘‘interest rate spread battle,’’ using large state-owned banks to put competitive pressure on private institutions, forcing down borrowing rates. This was done simultaneously with a reduction of the policy rate by the central bank. The intention was perhaps to reduce the burden of indebtedness on the workers, allowing them to renegotiate their debts on better conditions. But it was also intended to unleash a new wave of borrowing in order to sustain economic growth. These initiatives were short-lived. The Brazilian economy collapsed between 2014 and 2016, and a gradual process of deleveraging took place, bringing the household debt-to-disposable-income ratio down from 27 to around 21 by 2017, and the debt service ratio down from 23 to 20 in the same period.

From 2016 onwards, a new cycle of increasing global liquidity eased the constraints on the central bank and created conditions for a renewed wave of borrowing. At the same time, the depth of the recession that the economy went through kept inflation down and allowed the monetary authority to take the policy rate to levels never seen before in the country–6.5 in 2018 and then, after further easing, 2 percent in 2020. The household debt-to-disposable-income ratio surged 10 percentage points between 2018 and 2022. The debt service ratio took a little longer to follow, transitorily held down by the low interest rates.

In March 2021, however, the central bank reacted to contracting global liquidity and the inflationary pressures stemming from the post-pandemic recovery, taking the policy rate from 2 to 13.75 percent within eighteen months. The harsh realities of indebtedness in the capitalist periphery would soon become clear. Indebted workers were pushed to renew their debts under much worse conditions, and the debt service ratio shot up–from 18.3 percent in 2020 to 26.1 in 2023 and then, after the latest round of interest rate increases, to 27 percent in the first three months of this year (the latest data available). There is also evidence that the composition of debt deteriorated, with credit lines with higher interest rates (overdraft, credit cards and personal credit without automatic deduction from the paycheck) gaining ground in the last few years–rising from 18.2 to 24.7 percent of all household debt between 2020 and 2026.

From financial inclusion to financial expropriation

Lula completed his second term at the height of the first indebtedness boom in 2010, with very high popularity. There were naturally multiple reasons for that. Yet, it is plausible to assume that the credit policies contributed to it, as part of the strategy that stimulated the mass consumption boom. They were then seen predominantly as an achievement, as financial inclusion rather than financial expropriation, and their impact was very apparent. As the share of the population with bank accounts increased from 43 to 86 percent (between 2005 and 2017), the share owning a washing machine almost doubled (from 33.7 to 66.1 between 2001 and 2019) and the share owning computers more than tripled (from 12.6 to 40.6, in the same period). Meanwhile, ownership of fridges and TVs was effectively universalized (increasing from 85 and 89 to 98 and 99 percent, respectively).

A decade and a half later, the costs of worker indebtedness seem to have gained salience, overwhelming the earlier benefits. As interest payments surpassed a quarter of income, on average, the reality of financial expropriation as the other side of financial inclusion came to the fore. The government took heed and announced a series of initiatives to address over-indebtedness–first, in 2023, alongside the launch of the debt renegotiation program Desenrola, then this year with a second version of the program. Some of them aim to discipline the credit markets, imposing ceilings on some interest rates and on some debt service ratios. Most, however, focus on sponsoring the renegotiation of debts. They offer immediate relief to struggling debtors and may attenuate debt-driven resentment before the election. Yet, they are not up to the task of dismantling the mass-based financialization trap established over the last two decades.

The goal should obviously not be to drive the poor out of the credit markets, forcing them to make do with low and volatile incomes. Instead, the task is to complement financial inclusion with both a transformation of the productive structure that leads to better and higher-paying employment, and a strategy to reduce international financial subordination and thus address the problem of high interest rates. In this way, access to credit could actually benefit workers. In the absence of these transformations, however, as the Brazilian case illustrates, it simply pushes workers towards deepening financial expropriation.

Further Reading

Desenrola Brazil

Debt management as social policy under Lula 3

Credit in Brazil—and particularly consumer credit—is expensive, but ubiquitous. Exclusion from the credit market, where basic needs not covered by wages are increasingly financed, is...

Policy-Constrained Growth

Government spending and economic recovery in Brazil during Lula's third term

Despite headwinds from higher interest rates in the US and at home, the Brazilian economy is nevertheless emerging from a period of prolonged stagnation. After...

Controlling Capital

Inflation targeting and external vulnerabilities in the Brazilian economy

Central banks are back in the spotlight. After more than three decades of low inflation in rich countries, the rise in prices observed between 2021...