Issue 1, June 2026

Analysis

Arms Markets

A look at the world’s largest military industries

In 1934, a US Senate Committee chaired by the Republican Gerald Nye began eighteen months of hearings on the domestic arms industry, investigating the enormous profits it had generated from World War I, amid speculation that the “merchants of death” might soon drag America into another major conflict. The inquiry channelled a popular contemporary discourse which claimed that wealthy industrialists—executives at firms like DuPont, J. P. Morgan, and Pratt & Whitney—were wilfully stoking inter-state antagonism to drive up their margins. “The arms maker has risen and grown powerful,” noted a prominent study at the time, “until today he is one of the most dangerous factors in world affairs—a hindrance to peace, a promoter of war.” Even the Wall Street Journal, in its defense of the Nye committee, felt able to denounce the “vicious system which both admits and tempts men to the commercial development of bad blood among neighboring peoples.”1H.C. Engelbrecht and F.C. Hanighen,(<)em(>) Merchants of Death: A Study of the International Armaments Industry, (<)/em(>)(1934), p. 9. “Private Traffic in Arms,” (<)em(>)Wall Street Journal(<)/em(>), Sep. 8, 1934, p. 6.

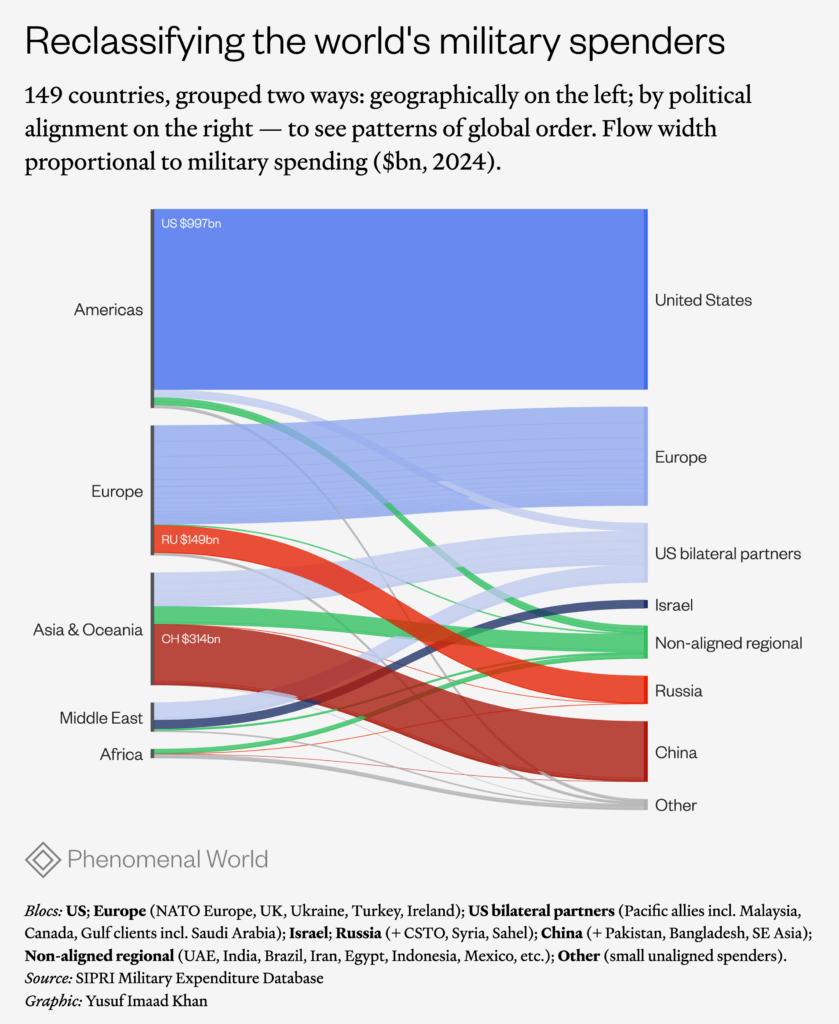

The notion that private interests are creating global volatility has never left circulation, but has newfound relevance as worldwide military spending reached a historic high of $2.9 trillion last year, to the benefit of weaponsmakers from Israel’s Elbit and the American “Big Five” (Boeing, Northrop, Lockheed, Northrop, and RTX), to Germany’s Rheinmetall and the UK’s BAE Systems.2The figure is for calendar year 2025 at 2025 prices and exchange rates. (<)a href='https://www.sipri.org/databases/milex'(>)SIPRI Military Expenditure Database 2026(<)/a(>) (as of April 27, 2026). Figures in the following paragraph are in current (nominal) prices, converted at the exchange rate for the given year, from this source. Figures in subsequent sections on exports and company rankings are from (<)a href='https://www.sipri.org/databases/armsindustry'(>)SIPRI Arms Industry Database(<)/a(>), retrieved December 2025, and (<)a href='https://armstransfers.sipri.org/ArmsTransfer/'(>)SIPRI Arms Transfer Database(<)/a(>).

Peace activists are correct to point out that the death merchants have been thriving in the 2020s, and that their interests lie in prolonging the destruction in Gaza, Iran, Ukraine, Sudan, and elsewhere—with teams of lobbyists striving to keep policymakers on a constant war-footing. But while the phrase “military industrial complex” was coined to warn that these profiteers could effectively capture the state, and that the primary problem is therefore the privatization of the defense sector, this framework risks neglecting the imbrication of public and private power in the global arms industry today. It is not private actors qua private actors who are responsible for the growth of the armaments industry. Ultimately, military markets are shaped by states: as clients and as owners. Mapping the world’s largest military-industrial complexes, their relationships to one another, and their overlapping structures of corporate ownership suggests that their expansion is, in the final estimation, subtended by the violent functions of statecraft itself.

This exercise also sheds light on how hard power is distributed on a global scale. The US is far and away the world’s largest military spender, military producer, and arms exporter, accounting for more than a third of global military expenditure and 42 percent of all exports, surpassing $1 trillion in 2024. Yet the global military economy is also populated by other actors who can influence the number and variety of weapons that are produced, bought, sold, and used on the battlefield. China is the world’s second largest military spender. Though it trails far behind the US ($335 billion), China’s military spending has increased every year for three decades, such that it now makes up approximately 12 percent of the world’s total. Third is Russia, which, since its invasion of Ukraine, has transformed into a war economy, more than doubling its military expenditure from $69 billion in 2016 to $190 billion in 2025, or 6.3 percent of GDP in 2025—a new high since the end of the Cold War.

Regional powers are also militarizing, with Iran proving itself a formidable armed opponent to Israel and the US, while India and Saudi Arabia are staking out their positions as the world’s largest arms importers. These states form part of a wider cohort, including the United Arab Emirates (UAE) and Turkey, which is now seeking military self-sufficiency through industrial and technological development geared towards domestic arms production. Each of them uses their military apparatuses against subordinated populations—the Kashmiris, the Yemenis, the Kurds—while others have developed arms-import networks beyond the reach of American empire.

Tracing the production and transfer of arms across the globe illuminates structural linkages between the wars ravaging disparate places. Israel and the US are collaborating on the campaign against the people of Gaza, Iran, and Lebanon, who are themselves using arms supplied by other Western states; Iran is trying to defend itself by drawing support from the Houthis, Hezbollah, and Hamas; Russia is attacking Ukraine and sending weapons to Iran in exchange for drone technology; Ukraine has developed fast and cheap counter measures against Russia and is dispatching them to Gulf states; the UAE, a key participant in the war in Yemen, is also supporting the Rapid Support Forces in Sudan, and so on. These connections make it difficult to isolate a single actor to hold accountable. For a more complete picture of these interlocking conflicts, we can assess each of the biggest arms titans in turn.

The United States and the North Atlantic

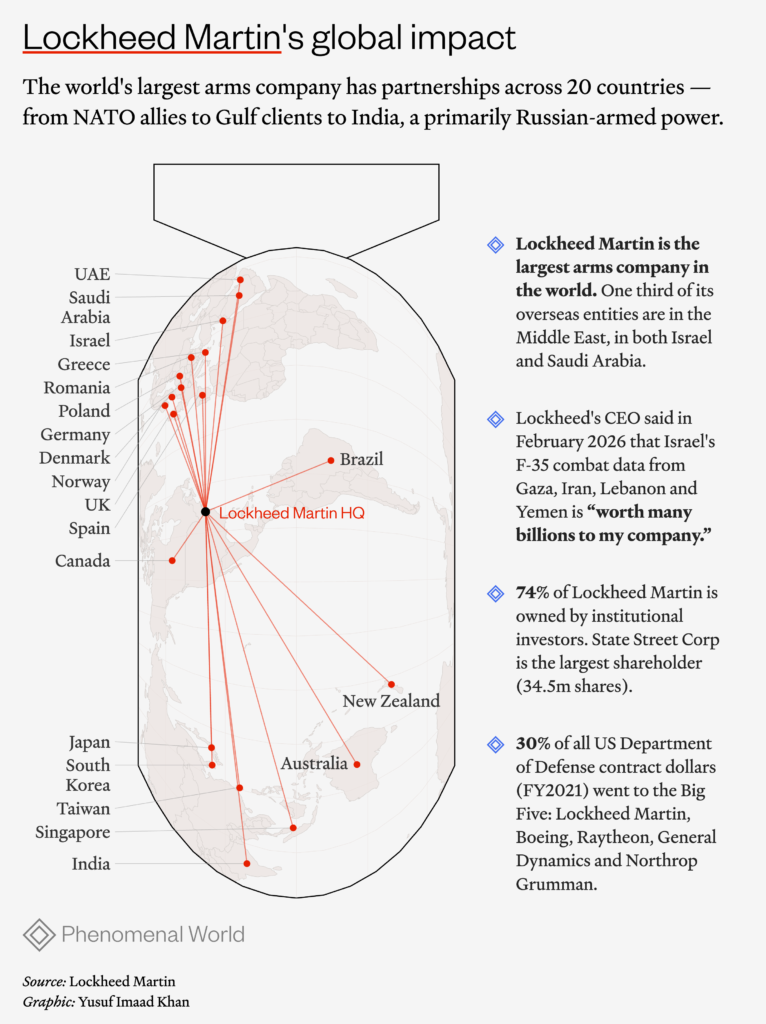

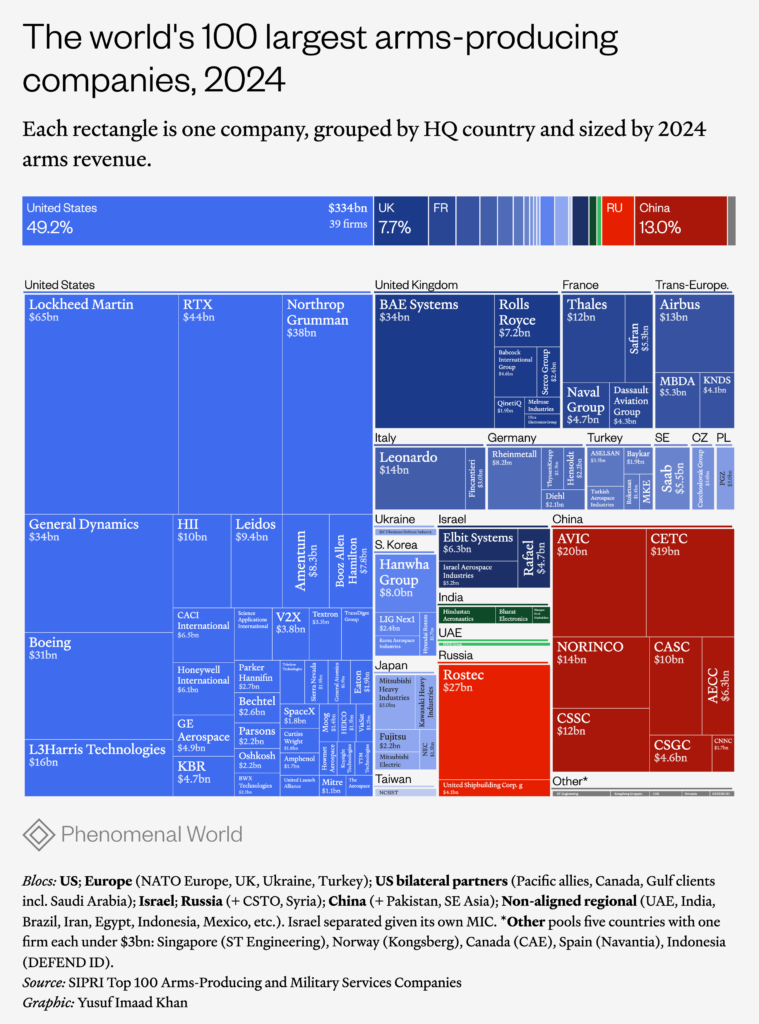

Just as the American state spends by far the most globally on its military, so do its companies dominate the industrial landscape. Thirty-nine of the top one hundred arms companies are headquartered in the US, and they account for 49 percent of the revenue of that group. The world’s largest arms companies are publicly traded corporations. They market securities to public and institutional investors through an initial public offering (IPO), usually traded on a stock exchange, and have public disclosure obligations. Most of their stocks or shares are owned by institutional investors. Asset-management firms own 74 percent of Lockheed Martin, and its biggest investor—owning 34.5 million shares—is the US-based multinational financial services company State Street Corp. The biggest individual shareholders were company insiders such as the CEO James Taiclet, former Chief Financial Officer Jesus Malave, and business segment president Stephanie C. Hill. As of May 2025, Taiclet on his own held 68,070 shares.3Lockheed Martin Corporation, 2025 Proxy Statement. Institutional ownership is from MarketBeat.

The ostensible separation between the private arms industry and the public sector benefits both parties. When arms companies are questioned about why and how their weapons are used in human rights violations, they cite government laws around arms exports. When governments are asked for details about company products and operations, they cast it off as commercially confidential information they are not at liberty to disclose. Privatization enables private and public actors to deflect scrutiny and accountability.

The non-state ownership of the arms industry, however, belies its dependence on the state. Most sales from American companies are to the US government—nearly three quarters of Lockheed Martin’s $75 billion 2025 sales were domestic—with the remaining quarter primarily sold to Saudi Arabia and Ukraine. The company ended 2025 with a record backlog of orders of nearly $194 billion. Arms firms have a tap on state resources through government defense budgets. In the US, almost half of the federal discretionary budget is allocated to the Department of Defense—now War—and over half of that department’s spending is channelled to military contractors. For the 2021 financial year, 30 percent of Department of Defense contract dollars was distributed across the top five contractors: Lockheed Martin, Boeing, Raytheon, General Dynamics, and Northrop Grumman.

Arms companies are, to varying extents, internationalized, with companies headquartered in one country while holding foreign entities abroad that manufacture weapons (or parts of weapons) and provide services. US firms have a presence in Israel, Japan, South Korea, and Taiwan, and beyond. UK-headquartered BAE Systems’s subsidiary, BAE Systems, Inc., is American, and the conglomerate as a whole sells as much, if not more, to the US Department of Defense than to the UK Ministry of Defense. This internationalization is a product of the post-Cold War period, when mergers and acquisitions, joint ventures, sub-contracting and technology-transfer agreements facilitated the consolidation of a transatlantic industry amid the (temporary) decrease in government military budgets after the fall of the USSR.

European countries have close relationships to US arms companies, though this takes a variety of forms. The UK has encouraged the privatization and internationalization of its military industry while state ownership is more common in continental Europe: Thales (the fifteenth largest arms firm globally in 2024, with $11.8 billion in revenues) is one-quarter owned by the French state. Leonardo (thirteenth, with $13.8 billion) is 30 percent owned by the Italian state, and Navantia (in lowly eighty-eighth place, with $1.3 billion in revenues) is fully owned by the Spanish state.

While defense procurement, military spending, and arms-export policy remain national issues, the supra-national European Union (EU), too, plays a role. It has helped drive militarization by way of the European Defense Fund, which was established in 2021, as well as the European Defense Industrial Strategy and European Defense Industry Programme, adopted in 2024. The EU has also used the European Peace Facility to finance weapons to Ukraine by reimbursing EU member states for deliveries of arms.

In part driven by Ukraine, in part by floundering US-NATO commitments, the EU has sought to dramatically ramp up its military industries. Arms exports across member states increased by 36 percent between the period 2016–20 and 2021–25, forming 28 percent of global arms exports in the latter period. As of 2025, Europe’s largest arms suppliers—France, Germany, Italy, and Spain—were responsible for exporting nearly two-thirds the volume of US arms exports, with 84 percent of EU exports going to non-member states. The EU’s export volume remains four times that of Russia and five times that of China, making it a highly influential global supplier.

China

Internationalization of the arms trade is much less pronounced in China, whose military industry is national in orientation and organized through state-owned enterprises. Defense is one of the seven strategic industries in China over which the government aims to have total control.4Lucie Béraud-Sudreau and Meia Nouwens, “(<)a href='https://www.tandfonline.com/doi/abs/10.1080/10242694.2019.1632536'(>)Weighing Giants: Taking Stock of the Expansion of China’s Defence Industry(<)/a(>),” (<)em(>)Defense and Peace Economics(<)/em(>), Vol. 32, Is. 2, (2021). The Made in China 2025 initiative ramped up funding for high-tech manufacturing, listing shipbuilding and aerospace as two of its top ten industry priorities. Since 2025, military-industrial officials have gained increasing relevance within the CCP. Beijing’s most recent Five Year Plan, announced in March of 2026, includes new sections on modernizing military strategy and governance. Since the period 2016–20, China has increased its arms exports by 11 percent: 77 percent are sent to Asia and Oceania; 13 percent to Africa. In Sub-Saharan Africa, China supplies 17 percent of imports—rivaling the US which supplies 19 percent.5Mathew George et al, “Trends in International Arms Transfers, 2025,” SIPRI Fact Sheet, March 2026.

Companies like North Industries Corporation (NORINCO) and Aviation Industry Corporation of China (AVIC) have significant international reach, having by now developed longstanding military pacts with Cambodia and Pakistan, whilst cultivating new relationships elsewhere in Asia and in Europe.. China’s key export customer is Pakistan, to whom it has transferred a wide inventory of weaponry, from fighter aircraft, frigates and tanks, to missiles and armed drones. As with India’s imports from Russia, some of Pakistan’s weapons are assembled from kits or produced domestically under license from China. Chinese-owned foreign entities in Western states are mainly oriented to civilian technology with some military application, most likely an attempt to gain access to dual-use technologies from abroad.

Some have criticized the risk-averse and bureaucratic nature of China’s state-owned enterprises, which, they argue, hinder competition.6Richard A. Bitzinger, “(<)a href='https://www.tandfonline.com/doi/abs/10.1080/01402390.2016.1221819'(>)Reforming China’s defense industry(<)/a(>),” Journal of Strategic Studies, Vol. 39, Is. 5-6 (2016). Under Xi Jinping, SOEs have been partly privatized in a search for new sources of capital. Shares of subsidiary firms are increasingly sold on the Shanghai, Shenzhen, and Hong Kong stock markets. This partial privatization has also had the effect of producing a more hybrid supply base, made up of non-state military-industrial firms as well as high-tech firms like Huawei and Lenovo.

Russia

Like China, Russia’s arms-industrial bases are national in orientation and located within the country’s borders. Russia has almost no military-technical cooperation with North Atlantic companies. Its arms industry is almost entirely state-owned and the government puts a strong focus on the domestic development of weaponry. This is partly a product of Western states’ restrictions on direct foreign investment, as well as sanctions against Russian companies since the annexation of Crimea in 2014.

Russia reportedly also owns military manufacturing entities in India, Kazakhstan, and Vietnam, which are the largest importers of Russian weapons. India’s Hindustan Aeronautics Ltd (HAL) and Russian firms have also engaged in joint ventures. But out of the world’s largest arms suppliers, it is the only one whose share of total exports are in decline—falling from 21 percent in the period 2016–20 to just 6.8 percent in 2021–25. India remains a significant importer of Russian weapons because it acquired most of its major military platforms from the USSR, useful for confrontation with China and Pakistan. But beginning in the early 2000s, India turned increasingly to American and European suppliers. Some of its weapons are systems assembled from imported kits, or produced under licence in India, like MiG and Sukhoi fighter jets. Russia’s declining exports have equally been driven by shifting import patterns from Algeria, China, and Egypt.

Russia has three forms of state-owned military companies: joint-stock companies, which allow private investment; unitary enterprises whose assets are owned by the state; and state corporations. Since 2010, Putin’s tightening grip on the state has meant increased power over the military. He centralized and increased government ownership of the defense industry (by way of the Military Industrial Commission), defused the infighting between companies and state bureaucracy, and made himself the chief mediator and arbiter in major defense-industrial decisions.

Russia’s war against Ukraine has only increased state control over its military industry, with some enterprises—thought to have been “illegally privatized”—forcefully brought back under public ownership. Like private companies, Russia’s state companies are organized around profit incentives, with the state as the largest shareholder receiving dividends. Despite this structure, most Russian companies are not profitable: even major state corporations report significant losses and complain about lack of revenue.7Mathieu Boulègue, (<)a href='https://www.chathamhouse.org/sites/default/files/2025-07/2025-07-21-russia-struggle-modernize-military-industry-boulegue.pdf'(>)(<)em(>)Russia’s struggle to modernize its military industry(<)/em(>)(<)/a(>) (Chatham House), July 2025.

Rostec—a state corporation made up of hundreds of military, engineering, and pharmaceutical companies, including the legendary Kalashnikov—receives an estimated US$21–25 billion annually from a variety of sources: government procurement contracts, arms exports, the sale of raw materials, and state subsidies. Rostec controls about 75 percent of all Russian military-industrial production, giving it a de facto monopoly. On that basis, it was listed by SIPRI (the Stockholm-based institute that tracks global military expenditure and trade) as the world’s seventh largest arms company in 2024.8Nicole Krome, “(<)a href='https://www.tandfonline.com/doi/full/10.1080/09668136.2021.1988905'(>)State Corporate Governance in Russia(<)/a(>),” (<)em(>)Europe-Asia Studies(<)/em(>), Vol. 74, Is. 8 (2022).

The Director General of Rostec, Sergei Chemezov, is known as one of the three most powerful men in Russia and is part of Putin’s inner circle. The two met in East Germany in the 1980s while working for the KGB. Chemezov moved to Rostec from the state arms-export agency Rosoboroneksport in 2007. In the words of Nicole Krome, Rosoboroneksport “functions as Rostec’s ‘cash-cow’,” providing a source of steady revenue to the state-owned producer.9Krome, ibid. Chemezov himself holds no stake in Rostec, which is 100 percent government-owned, but the Pandora Papers revealed the extent of his wealth: he and his family accrued over $400 million worth of listed assets through a network of offshore companies in real estate, banking, and oil, mostly listed in the name of his stepdaughter. Though hit with sanctions in 2014, he and his family retain control over critical elements of the Russian military economy, often through flexible forms of ownership and disguised as civilian projects.

Though radically different on the surface, a closer inspection of the military industries of the US, EU, China, and Russia exposes in all cases a web of deeply intertwined and mutually beneficial state and private interests.

Regional powers

Today, a number of smaller, regional powers are also looking to grow their influence through the arms trade. SIPRI reports that in 2024, nine of the Top 100 companies were headquartered in the Middle East—the highest ever number from the region. But SIPRI’s regional categories can obsecure underlying geopolitical alliances: of the Middle Eastern companies, for example, three were based in Israel, five in Turkey, and one in the UAE.

Turkish drone systems have helped propel the country’s arms exports, but Turkish companies produce a range of military equipment, from armored vehicles and corvettes to precision munitions and military-grade batteries. Ramping up defense production in Turkey has greatly benefitted domestic political elites by drumming up nationalist sentiment.

Gulf states have similarly been seeking strategic autonomy by way of domestic military strategies. The Abu Dhabi headquartered EDGE Group, as well as Saudi Arabian Military Industries (SAMI) are both state-backed national champions reliant on joint ventures with foreign firms. EDGE has recently been ranked thirty-seventh in the SIPRI Top 100 arms companies. For both countries, commitments to economic diversification has meant significant build-up of military-tech production.

Despite these efforts, the Gulf remains dependent on the West. BAE Systems, L3Harris Technologies, Lockheed Martin, and Raytheon have manufacturing entities in Saudi Arabia, while others use the region for maintenance and repair. Indeed, a third of Lockheed Martin’s overseas entities are in the Middle East. So close are the links with Israel, for example, that Lockheed’s CEO reportedly told Tel Aviv’s ambassador to the US that information from Israel’s use of the F-35 in Gaza, Iran, Lebanon, and Yemen is “worth many billions to my company.” In Saudi Arabia, Lockheed Martin now has a joint venture with SAMI to build helicopters locally, which hitherto Riyadh had been buying from the US since the 1980s.

India is another example of a growing military industry, mostly composed of state-owned corporations. In 2026, forty-one government-run ordnance factories were centralized into just seven state-owned Defense Public Sector Undertakings, managed by the Ministry of Defense.10Ash Rossiter, “(<)a href='https://www.tandfonline.com/doi/full/10.1080/14702436.2019.1685880'(>)Making arms in India? Examining New Delhi’s renewed drive for defence-industrial indigenization(<)/a(>),” (<)em(>)Defense Studies(<)/em(>), Vol. 19, Is. 4 (2019). Military self-reliance has been a stated goal of Indian development, at least since the 2014 “Make in India” initiative. The Adani Group, led by personal friend of Narendra Modi, Gautam Adani, is central to this defense industrialization drive. Adani collaborates with Israel’s Elbit Systems, Israel Weapons Industries (IWI), and the French-headquartered (and partially state-owned) Thales, among others.

India’s growing military ties with Israel have recently come in for scrutiny. India normalized and established diplomatic relations with Israel in the 1990s but it was in 2017 that the two countries established their “strategic partnership,” which involves the joint development of weaponry and technology transfer to India. If Israel was once the supplier and India the recipient, by now the relationship is best understood as one of co-development and co-production. The export of Hyderabad produced drones to Israel (made by Adani-Elbit Advanced Systems India) no doubt had much to do with the Modi government’s abstention on a 2024 UNHRC resolution calling for an immediate ceasefire in Gaza and an arms embargo on Israel.

Awash in weapons

What conclusions can be drawn from this brief snapshot of the global arms industry? For all the ways in which the American empire may appear to be in decline, be it in terms of its political, strategic, or ideological metrics, its military remains dominant—the most extensive, well-funded, and sophisticated in the world. The US is by far the world’s largest military spender, military producer, and arms exporter. The effects of its industry can be felt globally, not only because weapons manufactured by American companies are being used to rain down on cities, towns, and villages from Gaza to Minab to Kismayo, but because US-headquartered companies themselves have various subsidiaries and entities around the world, and source their parts from manufacturers everywhere.

But the US is not the only catalyst of the world’s current militarization drive, nor the only belligerent power. Though Chinese military spending is still dwarfed by that of the US, Beijing is rapidly expanding its own air, land, and naval armory, while increasing its exports, most significantly to Pakistan. Its investment in the UAE’s Khalifa port includes military access, even as the UAE serves as a foreign partner for American firms. The invasion of Ukraine has further driven Russian militarization, and India—one of the world’s top two arms importers—remains Moscow’s largest market for weapons. Saudi Arabia, the UAE, India, and Turkey are ramping up domestic arms production, in a bid to secure more autonomy in a world of shifting alliances. Though it is American imperial adventures that undoubtedly wreak the most damage globally, Israel, Russia, China, India, Saudi Arabia and Turkey are aiming their own growing arms against subordinate populations in their own spheres of interest.

In a deeply interconnected global arms industry, where divisions between the private and public sector are structurally obscured, alliances and responsibilities become blurred. Who makes the profits and owns the intellectual property in joint ventures between Saudi or Emirati and US-based companies? Which state’s export controls apply to the transfer of weapons for such joint ventures? Any serious attempt at arms regulation must closely grapple with these seemingly technical questions.

Further Reading

Anatomy of a Defense Budget

Tracing the growth of US military spending

Defense spending is projected to increase in 2026, reaching almost $1 trillion. This vast US defense apparatus operates through labyrinthine budgetary procedures, policies, and logics that...

Rearming Europe

Political legitimacy through war

The main justification for the EU’s recent dramatic reorientation toward defense is the proliferation of threats to European security emerging from Russia’s invasion of Ukraine....

Selling American Bombs

An interview with Sarah Harrison on the mechanics of US foreign military sales

Martin Luther King once called the United States government “the greatest purveyor of violence in the world.” That formulation may be controversial, but no one...