Analysis

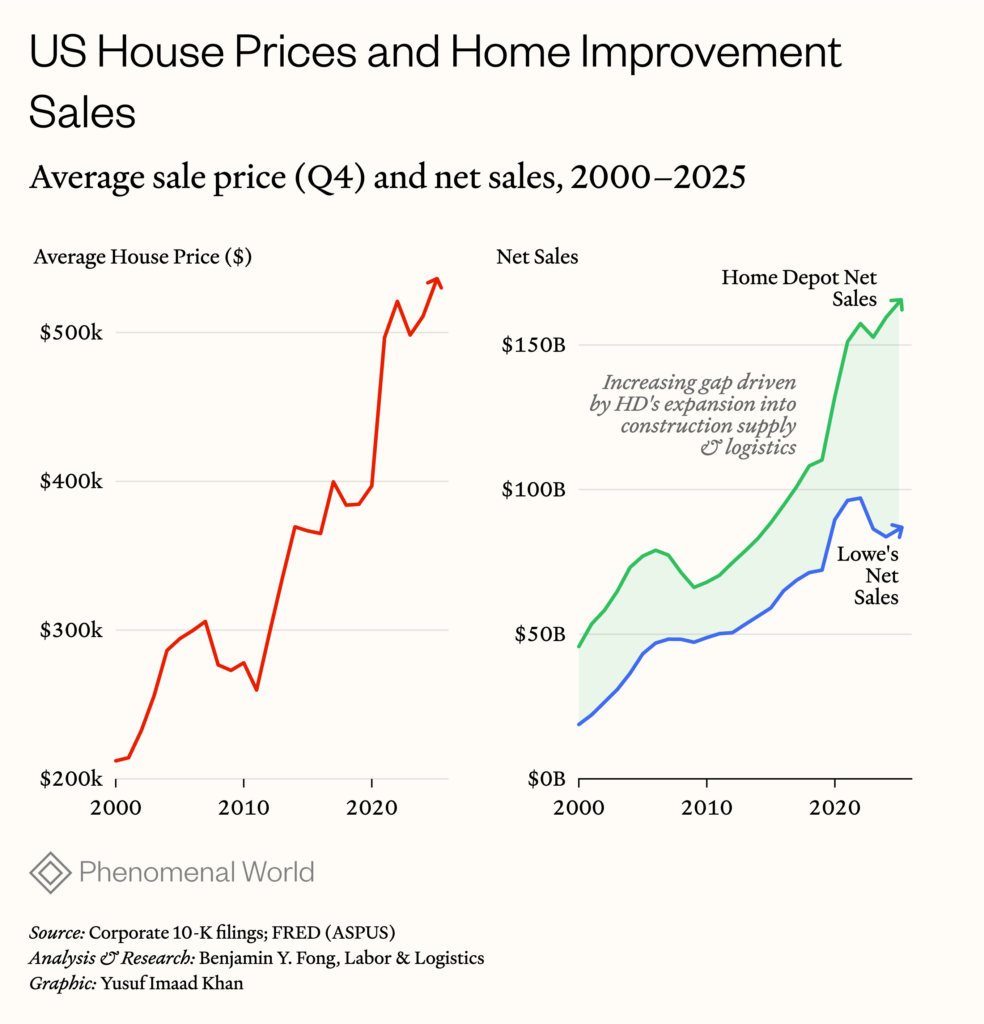

The rise of the big home improvement retailers—Home Depot and Lowes in particular—has coincided historically with the era of ever-appreciating residential real estate in the US. They tell the stock-buying public that their business forecasts depend on home values. “Our consumer [has] seen their home prices increase by over 50 percent since 2019,” Home Depot CFO Richard McPhail told the Reagan Economic Forum last year. “That means they’re sitting on $11 trillion in tappable equity. The means to spend is there.”

While both Home Depot and Lowes benefited from the Covid inflation of home prices, Lowes’s annual revenue has decreased dramatically in the past few years after a pandemic high, while Home Depot’s growth has maintained its stronger upward trend. In 2020, Home Depot’s annual revenue was 1.47 times that of Lowes; in 2025, it made 1.91 times that of its second fiddle. Part of this has been Home Depot’s expansion into commercial business-to-business sales to the construction industry: despite McPhail’s description of Home Depot’s market as DIYers working on their own homes, 55 percent of Home Depot revenues come from the just 5 percent of customers in their “Pro” membership business—general contractors and other kinds of businesses in the construction industry. For Lowes, the comparable figure is only 25 percent.

Another key reason for Home Depot’s success has been its ability to meet this demand. Over the past eight years, Home Depot has been on a building and acquisitions spree, restructuring its trucking networks and rapidly taking over a half-dozen logistics companies. In the process, it has created a unique opportunity for organized labor. Aiming to achieve same- or next-day delivery for ninety percent of its customer base on things like lumber, pre-fabricated materials, and home appliances, Home Depot’s expansion and centralization of its logistics business has required onboarding thousands of directly employed drivers at the trucking and warehousing companies it has acquired. In this process of solidifying dominance over Lowes and the big construction materials distributors, it has brewed a great deal of frustration for these new employees, and inadvertently propped open the door for unions.

Last mile, with bulk

Last mile delivery is the most expensive part of any parcel’s journey, often accounting for up to 50 percent of total shipping costs. It’s to internalize—and therefore control—these costly operations that Amazon built its own outbound network of Sortation Centers and Delivery Stations, as well as creating the aggressive subcontracting system of captive third-party Delivery Service Providers and casualized Flex gig drivers. Walmart has similarly invested in its Spark driver program, and Target in its Metro Sortation hub strategy—all in the name of finding ways to get packages to your doorstep with reliable speed.

Home Depot wants in on this game too. But given its product catalog (think windows, doors, lumber, appliances, vanities), it can’t simply assign gig workers as Amazon does to pick up a load of packages. Its strategy for speedy distribution of these bulky items has therefore involved two new kinds of distribution nodes that they have built out since 2017: what it calls its Market Delivery Operations (MDOs) and Flatbed Distribution Centers (FDCs).

Home Depot’s MDOs are cross-docking facilities, i.e., smaller warehouses that do not hold inventory and merely serve a routing function, near or in urban centers that handle appliances, and more recently larger items like patio furniture. The FDCs are larger warehouses where flatbed trucks are loaded up with construction materials for Home Depot’s professional clients. According to a recent company presentation, Home Depot currently operates 160 MDOs in the US, evenly distributed across the nation’s geography, and 17 FDCs in all the largest urban centers—which are also the largest construction markets.

MDOs provide three key benefits to the business of delivering to consumers: First, by routing all appliances through these cross-docks, which are connected upstream to vendors and other Home Depot distribution facilities, they can achieve speedier delivery on the company’s full assortment (one million SKUs online, as opposed to ~35,000 SKUs in store), beyond what’s available in-store. Equally important, the MDOs allow Home Depot to do quality assurance checks that reduce the number of returns on bulky products—for which the reverse logistics is an albatross. Lastly, the MDOs protect stores from dealing with the growth of home delivery. Attempting to expand deliverable inventory and increase quality assurance to the levels of a warehouse at a retail store degrades the in-store experience.

Despite the retail industry’s experiments with store-as-last-mile-facility strategies, many multinational retail corporations are increasingly coming to recognize that the logics of traditional retail and of e-commerce differ pretty significantly. You can’t do both in the same place very well without degrading the in-store experience or limiting the e-commerce assortment. This is especially true for bulky items like appliances. At around 9 percent of net sales, home appliances—refrigerators, dishwashers, washing machines and dryers—is pretty consistently Home Depot’s largest merchandising department.

The MDO expansion has relied not only on new warehouses, but on new trucking fleets and services. Home Depot decided to internalize a portion of this with its own private fleet, announcing in 2020 that it was handling 20 percent of MDO “deliveries in-house, while the rest are farmed out to third parties.” In 2023, it also acquired Temco Logistics, a trucking company that describes itself as providing “white glove” service to retailers as an appliance delivery and installation company. Home Depot rolled its existing private fleet into its new subsidiary, and today Temco handles a variety of different services for Home Depot in addition to MDO routes, including both deliveries from stores and, as we will see, deliveries from the new FDCs.

Like a pro

The FDC side of Home Depot’s new last-mile operation is being built to meet demand from the professional construction industry, not DIYers. First opened in 2020 in Dallas, Texas—a stronghold of open shop employers since before the McCarthy era—the FDCs are giant warehouses in which flatbed trailers are loaded up with bulk construction supplies. The idea is to be able to deliver lumber and other building materials to job sites via flatbed truck either same- or next-day. The Dallas FDC opened with the ability to accommodate 65-75 flatbeds per day. Since more than half of Home Depot revenues come from this market, the company has invested a great deal in the build out.

But FDCs are only one component of Home Depot’s strategy of bringing in the Pros. In 2004, it created a division called HD Supply for maintenance, repair, and operations (MRO) products and services. In other words, HD Supply provides big apartment complexes, nursing homes, hotels, etc. with replacement appliances and things to fix electrical and plumbing systems, all at wholesale prices. Home Depot sold this division in 2007, spinning it off into an independent corporation that grew its own distribution network of 129 facilities, by my current count. But in a renewed effort to grow its professional market, Home Depot reacquired HD Supply in 2024. Some of Home Depot’s largest warehouses by employee count today are HD Supply facilities.

The same year it acquired HD Supply, Home Depot also bought SRS Distribution, which supplies professionals in roofing, pool, and landscaping businesses. The deal came with 11,000 employees and 4,000 trucks across 700 branch locations. (Roofing is a key play for Home Depot at a time of slow housing construction, as 80 percent of roofing purchases are for repairs on existing homes.) It was also an indication to building materials distributors that the big retailers are coming for them. The major business-to-business materials distributors that are competitors in the Pro space with Home Depot include ABC Supply (~$21 billion net sales in 2025), W.W. Grainger ($17.9 billion), Builders FirstSource ($15.2 billion), Ferguson Enterprises ($12.8 billion), Graybar (~$12 billion), Boise Cascade ($6.4 billion), TopBuild ($5.4 billion), and BlueLinx ($3 billion), and F.W. Webb (~$2.4 billion). With 55% of its revenue coming from Pros, Home Depot’s comparative annual revenue for its Pro segment is $87.7 billion—more than four times its largest rival in the space.

A new workforce

The corporate reorganizations accompanying Home Depot’s logistics expansion represent a new centralization of business power. This centralization has not been altogether happy, but the pain is not without remedy. In February of this year, Temco Logistics drivers in Lithonia, GA became the first workers at a fully-owned Home Depot subsidiary to win an NLRB union election.

The newly unionized drivers, however, do not work out of an MDO or a store, but rather out of an FDC in Stonecrest, GA, just east of Atlanta. The warehouse is part of a large industrial cluster, including warehouses for Pepsi and a few other logistics and manufacturing operations. The Temco workers deliver building materials to job sites in flatbed trucks with Moffett forklifts on the back, which they also operate to unload the materials. The Lithonia workers are one of five Temco flatbed locations in the country; all other Temcos run two-man crews delivering appliances.

Among other factors contributing to the union effort was the fact that workers’ vacation time had gone down and their insurance costs had gone up since the acquisition. But it was work rules that seemed to most upset Temco’s drivers. Before the Home Depot acquisition, the majority of drivers with Temco had a steady four-day week of ten-hour shifts, and if the work was done early, they could go home and still get paid for the full ten hours. According to Matthew Rupley, a lead organizer with the Teamsters who worked on the campaign, after Home Depot bought the company it “stopped doing that. They make people sit in the yard and wait, or they send some people home and not others. The favoritism is crazy.”

“Terrible” is how Rupley described the conditions at Temco in Lithonia. “Their jobs were threatened every day. They have a pre-shift meeting at 5am where managers bully drivers. People do not feel like their job respects them at all.” Temco driver Jaree Beatles confirmed the hostile and stressful nature of these meetings:

Drivers would try to speak in a meeting, and they’d tell a grown man or woman to just hush. Like, we can’t talk. It was treating us like we were in middle school. And those meetings would go until like 5:30 am, and we would [still] have to be off the yard by 6 and… do a pre-trip [inspection] and… check our loads. It’s a lot of stuff to do and still be off in 30 minutes. It was just too much.

Temco is not the only carrier that works out of Home Depot’s Stonecrest FDC. Home Depot also contracts with TMC Transportation, and it was common for Temco management to threaten their drivers that Home Depot would give their hours to their TMC counterparts. As Rupley described the threat, “If you don’t do like you’re told, your work’s gonna go to a contractor.” At the same time, TMC drivers weren’t forced to stick around after they finished their routes. Beatles says TMC drivers were also allowed to better heed safety precautions: “When they get to a location, and it’s not safe to do, they bring the stuff back. If we bring it back, [they tell us] to go back out and try to deliver that material” to the same location.

Beatles had previously driven for UNFI, a wholesale grocery distributor, and knew the benefits of being a union member. His leadership and respect among the drivers was instrumental to the success. But also aiding their effort was the fact that, in January, 59 drivers for the Pepsi plant in the same logistics cluster as the Stonecrest FDC won an NLRB election to be represented by Local 528. According to lead organizer Rupley,

We were organizing [Pepsi] drivers, and when we went out to do gate action, and hand out flyers to get out the vote,… Temco drivers came over to talk to us as they were getting off, because they’re literally across the street. Then the Pepsi guys were supporting the Temco guys, and now that whole corner of the industrial park is celebrating each other’s victories and pulling for each other.

After their successful election in February, Beatles said that management has turned up the pressure. “They implemented and started enforcing more policies that have been there but they weren’t enforcing before, like uniforms, point systems [their disciplinary system]. They’re being more tedious with that, and just overall.” Meanwhile, the informal flexible hours policy, where workers can go home after completing their daily routes, was re-instated for box truck drivers at the nearby Temco location in East Point, GA, which services a Home Depot MDO—an improvement in working conditions no doubt intended to halt the spread of unionization.

Temco workers are not the only drivers working directly for a recently acquired Home Depot subsidiary. SRS Distribution, the roofing, pool, and landscape supply company Home Depot bought in 2024, has 3,378 drivers for its 4,000 truck fleet, all of whom, like Temco employees, are adjusting to working for a new corporate entity. HD Supply, which has 12,000 employees and 700 delivery trucks, also has its own in-house delivery workforce. You don’t have to dig very much on Reddit or Glassdoor to find some simmering resentment among these employees. An SRS Logistics Specialist complained after the Home Depot acquisition that “There is now very little incentive for frontline employees to do anything other than the absolute bare minimum. On top of that, Home Depot continues to restrict branch resources putting an even harder workload on fewer employees.” On Reddit, a Home Depot employee expressed “My sympathies to SRS, their employees will be treated the same way we are.” Another noted: “I worked for hd supply/ Crown Bolt and was told nothing would change with acquisition. Everything changed with a year. Be prepared.”

In the flurry of activity to rework their last-mile options for both home and job site delivery, however, Home Depot may also have created a toehold for workers that want collective bargaining. The integration of their subsidiaries has created deep frustration among a variety of directly employed drivers who are essential to the success of their speedy delivery model. Of course, Home Depot can and likely will use third-party delivery options where they face the threat of unionization, as they have an established core carrier program and already appear to rely on a variety of them for flatbed deliveries. They will also try to divide the workforce by offering concessions to workers who reject unions. But for the moment, there’s a unique point of entry at an historically open-shop stronghold of big-box retail. As Beatles concluded, “If drivers come together, and they really stick together, the companies will have to start treating everybody fairly instead of treating us like a number.”

Further Reading

Overexpectations in e-commerce?

A story told through the clash of the world's two largest corporations by revenue

Is brick-and-mortar retail bound to lose ground to the new portals of infinite choice and doorstep delivery? The picture is more complex than it might...

The Apotheosis of Point of Sale Data

The complex logistics and labor costs that make same-day delivery possible

The increasingly complex logistics of Amazon’s same-day delivery expansion—and the labor costs that make it possible.

Scorched Earth

Climate adaptation on a boiling planet

Programming Note: In addition to this monthly newsletter, Kate and Tim are regularly publishing dispatches and putting out podcasts, which you can find at thepolycrisis.org....