Analysis

The Beijing Pivot

Strategic stability and industrial autonomy after the US–China summit

Programming Note: In addition to this monthly newsletter, Kate and Tim are regularly publishing dispatches and putting out podcasts, which you can find at thepolycrisis.org.

The US–China presidential meeting in Beijing last month signified the end of a decade of trade and economic hostility. The countries agreed to establish joint boards of trade and investment, pledging their intention to achieve “strategic stability.” Sales of Boeing aircraft to China were announced (albeit fewer than expected). The possible resumption of rare earths exports to the US was floated, and China gave assurance that it wouldn’t provide arms to Iran. After years of chip wars, sanctions, and economic isolationism, both countries declared they would move towards a more constructive stance based on “fairness and reciprocity.”

After a decade of bipartisan enmity towards China, the US is seeking rapprochement. Threats of skyhigh tariffs were substituted for an entourage of American CEOs in Beijing seeking access to Chinese markets.

The sources of this capitulation are multiple. One is the failure to get other countries on board with an anti-China stance. Europe had already rejected the US language of “decoupling” from China in 2022–23. Trump’s “Liberation Day” tariff announcement last April was roundly viewed by US allies as an attack, ultimately causing many of them to reaffirm their ties with China; numerous heads of state from Europe and G7 countries have visited Xi in Beijing since Liberation Day.

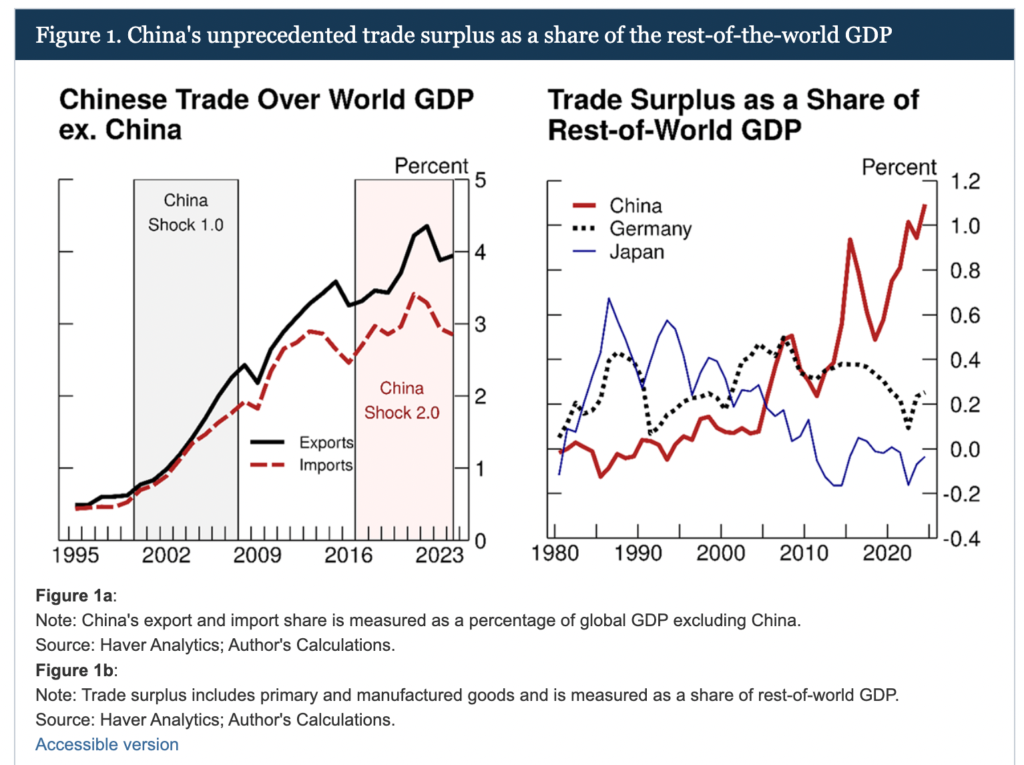

Another factor is the realization that the US cannot defend itself against China’s dominance in rare-earths production—a weapon that China is now demonstrably willing to wield. US defense, aerospace, tech, and energy manufacturers quickly began to struggle with shortages of rare earths such as yttrium when China imposed export controls on half a dozen minerals last year, before winding them back when the US administration backed away from punitive tariffs of up to 250 percent on Chinese goods.

Securing supplies of critical minerals and rare earths has become a key plank of US trade agreements, but establishing new supply chains is slow and complex work. China has been building its mineral production capabilities for decades, investing in training engineers and building out industrial and foreign-policy tools. Sourcing replacements for Chinese materials cannot be done swiftly, even with all of the legislative and financial power that the US administration can muster. You can print money but you can’t print molecules.

This recognition has helped rebalance what Jon Bateman at the Carnegie Endowment for International Peace has referred to as the battle between American “restrictionists” and “cooperationists.” The more hawkish restrictionists often invoke arguments about cheap Chinese imports hollowing out US manufacturing—the China Shock thesis—and warn that “Chinese tech-driven dominance” must be stopped. Cooperationists, by contrast, point out that broadly cutting ties with China is impossible; they fear US overreach will cause extensive damage.

By now, it is clear that the restrictionists have lost because the US lacks the power to actually win the economic war it started. As sanctions expert Nicholas Mulder points out, the US may have maintained a monopoly on economic sanctions for decades in the post-war period, but China’s retaliatory export controls on rare earths last year, and Iran’s effective blocking of the Strait of Hormuz more recently, underscores the fact that powerful economic weapons are not solely the prerogative of Washington. US adversaries can harm the American economy and erode political will to continue restrictionist policies advocated by economic warriors.

However, a successful rapprochement with China will require some coalition of domestic corporate, financial, and political power. The US–China relationship has its own unique qualities, but there are few countries where economic models and politics are not facing challenges from Chinese manufacturing exports.

China boom

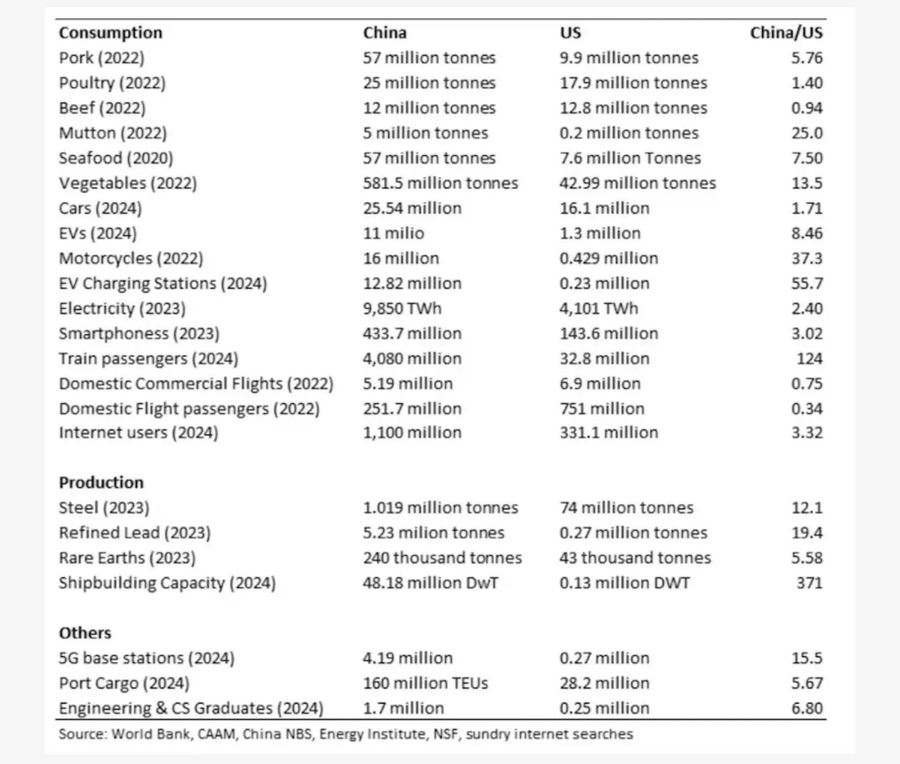

China’s manufacturing capability has developed rapidly since the 2000s. Local governments are encouraged to develop not only in established strategic products like the “new three”—solar, EVs, and batteries—but also “new quality productive forces” like robotics, AI, shipbuilding, and biomedical manufacturing.

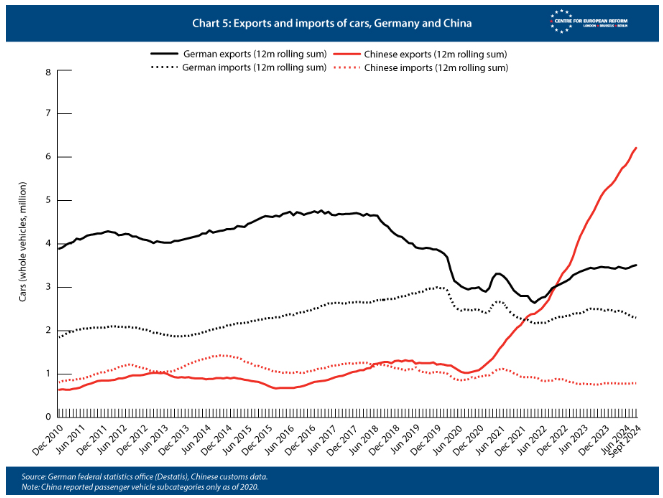

The speed with which some of China’s high-tech manufacturing has improved has taken some countries by surprise. Electric vehicles have been the most striking example, and it’s thanks to that boom in production that China overtook Germany as the world’s biggest passenger car exporter in 2022. German car sales in China, which were once a significant source of trade income, collapsed in just a few years.

That surprise is, in itself, surprising—at least in retrospect. The assumption, inherent in the convergence ideology of the 1990s, that a country the size of China would simply fall into line with the West, constraining its own development, was always naive. The first China shock, which came in the 2000s, may have been viewed in terms of “catching up.” But by now, China’s industrial and technological development is “redefining the boundaries of the possible in many sectors,” in the words of Adam Tooze.

China’s actions have been informed by its own economic, developmental and security strategies. Beijing’s drive for self-reliance during the economic war of the past decade came in part because of its fears of reliance on imported commodities. China became a net food importer in 2004, and in 2021 overtook the US to become the world’s largest food importer. It has been a net oil importer since the early 1990s, growing to become the world’s largest oil importer, and perhaps most surprisingly, became a net coal importer in the 2010s.

Xi began making statements about the need to plan for various challenges posed by foreign reliance soon after coming to power in 2013, but it was not until 2017, with the sanctioning of the giant Chinese telecommunications firm ZTE by the first Trump administration that Beijing was alerted to the extent of the threat. Kyle Chan has referred to that moment as a “wake-up call for Beijing,” noting that soon after, the Ministry of Commerce began establishing a “legally grounded, unified system of export controls.” With the US sanctions on Huawei in 2019, the need for such controls was made abundantly clear, and after the outbreak of Covid-19, Xi was open about China’s massive supply chain vulnerabilities. In a hostile geo-economic world, these would require sustained attention.

A European strategy

In Europe, the last few years have been similar debates and divisions about how best to relate to Beijing’s growing strength. The rapid eclipse of German global car exports by Chinese automakers in 2022 was a major turning point, persuading European leaders that Beijing could excel in advanced manufacturing and design. The timing of this roughly coincided with Europe’s squeeze by a protectionist American industrial policy in Biden’s Inflation Reduction Act. Covid supply chain shortages and the energy shock stemming from Russia’s invasion of Ukraine meant that Europe had to acknowledge the end of liberal globalization.

Europe has struggled to respond to this new world in which the lines between allies and rivals are blurred, and in which few are following the rules. The 2024 Mario Draghi report on EU competitiveness advised focusing on a strategic selection of manufacturing industries and buying the rest (mostly from China); the bloc would need €800 billion of investment a year to effect this. But implementation of the Draghi report has been slow. Tensions between member states means that Europe used precious little of the economic and security firepower it has at its disposal. Some strategic industrial development has taken place in the last few years thanks to loosening EU restrictions on state support of domestic industries, as well as some debt-financed investment from EU programs in the wake of Covid and the Ukraine energy shock. But the most significant response to this new landscape of industrial and sectoral rivalry is the proposed Industrial Accelerator Act (IAA), which seeks to use its annual €2 trillion of public procurement to support EU innovation and jobs with local content requirements and mandatory screening of inbound foreign direct investment.

EU politics are, of course, never simple and the IAA will pit French restrictionism (prioritizing EU-based production) against the cooperationist stance of trade-liberal states like Germany and the Nordics. Germany’s auto industry fears losing not just its remaining market in China but also its own Chinese-based manufacturing, its technical collaboration with Chinese firms, and its exposure to the “fitness centre” of the hyper-competitive Chinese auto market.

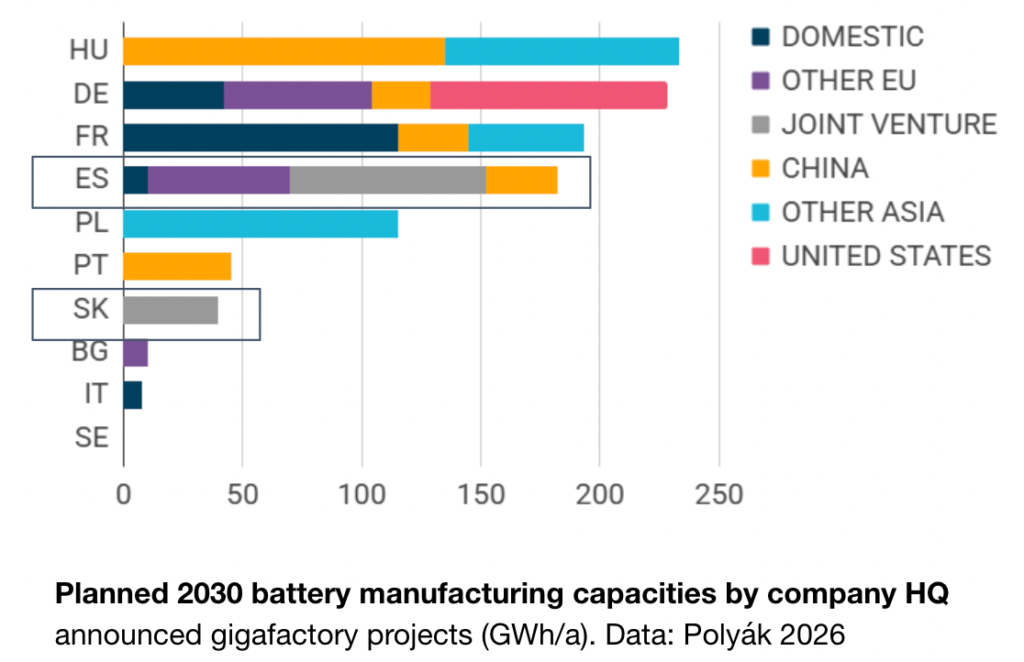

Chinese foreign direct investment in Europe is also growing. Hungary has attracted much Chinese FDI in its car and battery factories, and Spain, too, is fast becoming a destination for Chinese capital. It already hosts a Chery auto facility, and a €4bn CATL-Stellantis battery factory is being built in Aragon; SAIC will build its first mainland European factory in Galicia.

The “China squeeze”

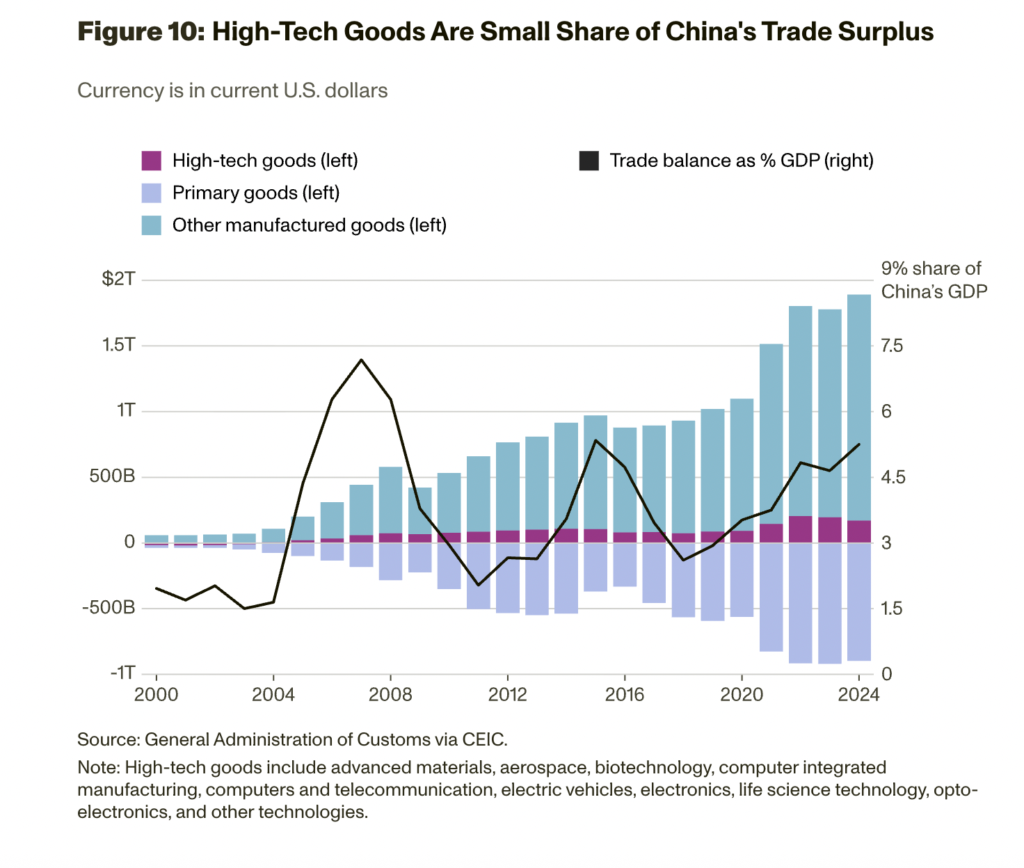

For all the alarm about Chinese high-tech goods, advanced manufactures are only a small part of China’s exports. The vast majority of exports remain simpler goods like apparel, and so far China is not abandoning these industries as it moves up the value chain.

That poses a threat, or at least a dilemma, for many developing nations. China’s extensive production of cheap goods, both simple and complex, reduces the space available for lower-income countries to industrialize and produce their own low-tech, labor-intensive exports. This is what Shoumitro Chatterjee and Arvind Subramanian at the Peterson Institute for International Economics have called the “China squeeze.”

Some countries have the good fortune to possess natural resources. The DRC, Guinea, Zimbabwe, and Namibia have all had some success in attracting investment by restricting exports of raw extractives. Indonesia has collected significant amounts of FDI and value-added exports from its export ban on raw nickel ore introduced in 2020—albeit not without some drawbacks.

Countries bereft of their own natural resources, or desirable consumer markets, might benefit from overseas Chinese foreign direct investment, or at least find opportunities to localize some parts of the value chain, if they can draw upon strong state capabilities. Almost half of the solar gear imported into Africa now is cells and wafers, rather than fully assembled panels. This means that countries like Ethiopia, Tanzania, Nigeria, and Kenya are already capturing a lot more of the value of the continent’s solar boom.

For those developing countries with even fewer bargaining chips and resources at their disposal, perhaps the best they can hope for in the near-term is taking advantage of China’s prolific manufacturing by deploying renewable energy and batteries to reduce their liabilities for fossil-fuel imports.

***

Developing or protecting industries in the context of Chinese manufacturing prevalence will require more than just trade relationships; domestic policy will be a big determinant of success in every type of country. The tendency of countries to focus solely on trade and industrial policy risks missing a bigger picture. China has built manufacturing on an array of broad measures.

Relevant lessons for other countries can be hard to find in China. Few can mimic its governance structure (which combines top-down directions with local improvisation and competitiveness), its ability to subdue powerful economic forces (like the property market), and the sheer scale of China’s economy.

Some drivers of China’s success, though, are widely instructive. Its use of policy tools from credit policies to higher education are salient for most countries, and its investment in basic health, literacy and infrastructure have helped set it apart from other large middle-income countries like India.

When confronting their industrial prospects, virtually all countries have to contend with their own domestic politics and distributive conflicts. German oligarchic families, for example, control giant corporations like Volkswagen and BASF that are invested heavily in China, and have enormous influence over the EU’s Chinese policy. In poorer countries, too, powerful elites will determine whether both domestic policies and international alliances benefit the whole society or just facilitate footloose globalization for the privileged few.

Distributive politics sit underneath geo-economic contests. In reckoning with this new global industrial landscape, there is no shortage of challenges.

Filed Under