Issue 1, June 2026

Analysis

Nvidia in the Gulf

The Arab monarchies turn to Silicon Valley

In May 2025, Donald Trump, accompanied by many of Silicon Valley’s luminaries, traveled to Saudi Arabia, Doha, and Abu Dhabi for the first overseas venture of his Presidential term. The same day he touched down in Riyadh, the President rescinded the Biden-era “Framework for Artificial Intelligence Diffusion.” Through the Framework, Trump’s predecessor had imposed detailed export controls on US chips, seeking to protect strategic technologies and contain the rise of China. In the Gulf, Trump revealed a more transactional approach—one jointly aimed at self-enrichment and consolidating the dominance of American firms within key markets.

In the policy pivot, Trump’s hosts saw a golden opportunity. Pledging up to $1 trillion in US-bound investment, the Saudis secured the right to import 18,000 units of Nvidia’s most advanced Blackwell server, the GB300. 1Kif Leswing, “Nvidia sending 18,000 of its top AI chips to Saudi Arabia”, CNBC(<)em(>) (<)/em(>)(May 13, 2025). Just before Thanksgiving, the Commerce Department’s Bureau of Industry and Security officially signed off on Trump’s pledge, in fact licensing Saudi Arabia to acquire up to 35,000 GB300s. The UAE’s Group 42 Holding Ltd (G42)—the technology holding company through which Abu Dhabi runs most of its artificial intelligence (AI) ventures—was meanwhile given permission to import 500,000 units of Nvidia’s H100 chips annually.2Natasha Turak, “US, UAE agree on path for Emirates to buy top American AI chips, Trump says”, (<)em(>)CNBC (<)/em(>)(May 16, 2025). This marked a striking reversal. For the past two decades, the Gulf had pumped credit and equity into the American tech ecosystem. While such financial flows have by no means dried up, new AI arrangements signal that these countries are now beginning to onshore critical elements of American tech’s infrastructure. The recent Nvidia deals, and the geoeconomic pivot they represent, pose a number of questions. Why has Washington moved away from its protectionist approach and pursued these commercial ties with the Gulf? Why have Saudi Arabia and Abu Dhabi, in turn, placed such a major bet on American AI? What does this mean for US imperial strategy more broadly?

For years, the Gulf’s outward investments have assimilated the region into circuits of accumulation dominated by the giants of the American information and communication technology (ICT) sector. Following the global financial crisis, the Gulf’s sovereign wealth funds played a critical role in servicing Silicon Valley’s insatiable demands for liquidity. This buttressed an American political economy increasingly tethered to rising asset valuations. Yet Gulf financial stakes in Silicon Valley had limited economic effects back home. They brought little in the way of tech transfers or upgrades to domestic productive capacity. Firms in these countries remained far removed from the technological frontier. Through their deals with the Trump administration, members of the Cooperation Council for the Arab States of the Gulf (GCC)—the alliance that comprises Saudi Arabia, Bahrain, the UAE, Kuwait, Oman, and Qatar—now seem to be changing tack: reconceptualizing not only their approach to the tech sector, but also its position within the fracturing world economy.

As yet, this transition remains fraught and incomplete. Just as the Gulf states have pinned their fortunes on the seemingly unstoppable rise of US tech, the primacy of politics has violently reasserted itself, with Tehran responding to the US-Israeli war of regime change by bombing Amazon Web Services data centers in the UAE and Bahrain. It thus remains uncertain whether the GCC’s alliance with Washington, as mediated by Silicon Valley, will turn out to be a source of economic dynamism or an area of acute vulnerability. The ultimate outcome will have far-reaching implications for the Middle East and its place in the inter-state system.

Washington and the Valley

The connection between Silicon Valley and the Gulf has its roots in the American state’s secular decline in research and development (R&D) capacity. During the 1960s, the federal agencies that had been charged with leading public, technology-facing research after the Second World War—the likes of NASA, the Defense Advanced Research Projects Agency, and sister institutions—absorbed approximately 17 percent of federal discretionary spending. In the first decade of the 2000s, by contrast, the figure dropped below 10 percent. As a share of GDP, federally funded R&D fell from a peak of nearly 2 percent in the mid-1960s to around 0.5 percent by the mid-2010s.3The Task Force on American Innovation, “American exceptionalism, American decline? Research, the knowledge economy, and the 21(<)sup(>)st(<)/sup(>) century challenge, Report (December 2012). Rebecca Mandt, Kushal Seetharam, Chung Hon Michael Cheng, “Federal R&D funding: the bedrock of national innovation”, Report: MIT Science Policy Review (2020). This altered the state’s relationship with a particular fraction of American capital, as the emerging ICT megaliths—Microsoft, Amazon, Alphabet (Google), and Meta (Facebook)—became increasingly responsible for planning processes and research capitalization related to the development of new technologies. The tech giants’ relatively low-cost, predatory innovation model—reliant on outsourcing, infrastructural control, and intellectual property-based rent extraction—helped to build what would become known as intellectual monopolies. Aided by the advance of platformization, these firms captured an expanding share of the wealth generated by a newly digitized and service-oriented economy.4Cecilia Rikap, “The US national security state and Big Tech: frenemy relations and innovation planning in turbulent times”, (<)em(>)Review of Keynesian Economics (<)/em(>)12:4 (2024). Cecilia Rikap and Bengt-Ake Lundvall, “Big tech, knowledge predation and the implications for development, (<)em(>)Innovation and Development (<)/em(>)12:3 (2022).

Thus, Silicon Valley was steadily transformed into more than just the main engine of US economic growth. By the 2010s, it was a behemoth exploiting and absorbing smaller firms and subordinating entire industries to its will, creating staggering fortunes along the way. It developed technologies that were more and more pertinent to national security, so that whereas the Pentagon had once invested heavily in Silicon Valley, it now came to rely on Big Tech for everything from surveillance to cloud communications, robotics to artificial intelligence. As the US state became existentially reliant on the tech sector, the latter accrued more influence over policy. Critically, the Federal Trade Commission (FTC) disregarded antitrust law and allowed the leading tech companies—Google, Facebook, and Amazon—to carve out unassailable monopoly positions across a number of fields. The power of these firms within the world system grew commensurately.5Jessica Crobett, “’Total scandal’: Memos expose failure of Obama-era FTC to stop Google’s monopoly power”, (<)em(>)Common Dreams (<)/em(>)(March 16, 2021). This history can be surveyed quickly here: Stavroula Pabst, “How the Pentagon built Silicon Valley”, Analysis: Responsible Statecraft (August 24, 2024).

Over President Obama’s eight-year tenure, Silicon Valley’s sectoral interests were elevated into general ones. He created the new executive positions of Chief Technology Officer and Chief Data Scientist in the Office of Science and Technology, and Chief Performance Officer in the Office of Management and Budget, staffing each with industry-friendly appointments. The launch of US Cyber Command in 2009, followed by the National Security Strategy and Quadrennial Defense Reviews of 2010, saw the consolidation of this Big Tech–national security nexus, with digital infrastructure designated as a “national strategic asset.”6In order to protect US holdings of this asset, the Obama administration also explicitly called for strengthening partnerships with private sector leaders. Cristina Soreanu Pecequilo and Francisco Luiz Marzinotto Junior, “US power and the multinational tech companies of the digital era: an analysis of the Obama and Trump governments’ oligopolization (2009-2021),” (<)em(>)Austral: Brazilian Journal of Strategy & International Relations (<)/em(>)11:21 (2022). Obama’s second Chief Technical Officer, Todd Park, founded and directed a number of healthcare-focused software startups. His third, Megan Smith, came to the role after serving as a Vice President for Google.

The rise of American AI

Yet after this initial growth spurt, the tech sector found itself adrift in the late 2010s. With little means to sustain the rate of innovation, it tried instead to juice profits from existing products, leading to a sharp deterioration in quality. Facebook’s $77 billion investment in the “metaverse,” which ultimately yielded no new product and failed to generate any additional revenue, was a sign of growing desperation. In this context, American tech turned to generative AI, which had first taken off in 2012, as a possible solution.

The first Trump administration responded to the AI race with Executive Order 13859 and the National AI Initiative: two interventions whose logic was distinctly laissez-faire, giving the private sector the prerogative to drive the development of the new technology. This hands-off approach was welcomed by Silicon Valley and more or less maintained under the Biden administration. While FTC head Lina Khan made greater attempts to enforce antitrust laws, Meta and Microsoft outmaneuvered her in court to continue acquiring potential competitors.7Federal Trade Commission v. Meta Platforms Inc., et al, No. 5:2022cv04325 – Document 570 (N.D. Cal. 2023). Federal Trade Commission v. Microsoft Corporation et al, No. 3:2023cv02880 – Document 305 (N.D. Cal. 2023). The FTC appealed the Microsoft decision. In May 2025, the Ninth Circuit upheld the lower court’s decision. And while the White House made some attempt to impose guardrails on AI development—for example, through the Blueprint for an AI Bill of Rights—the general thrust of state policy remained the same: unambiguous support for Silicon Valley’s lead players and an iron-clad commitment to furthering their interests. This was evident in Biden’s fall 2024 National Security Memorandum, which reaffirmed the necessity of private-sector-led AI development in the context of rising rivalry with China. The CHIPS and Science Act of 2022, meanwhile, had already offered up tens of billions in subsidies and tax credits for semiconductor manufacturing and research in an attempt to protect Silicon Valley from competition. By situating the AI policy debate within the arena of national security, the administration gave permission for the tech firms to shirk their official responsibilities on regulatory standards, reporting, and transparency.8Preferential regulatory treatment is amply discussed in Karen Hao, (<)em(>)Empire of AI: Dreams and Nightmares in Sam Altman’s OpenAI (<)/em(>)(Penguin Books: 2025). For semiconductor export controls and their unintended consequences, see: Rodrigo Balbontin, “Backfire: export controls helped Huawei and hurt US firms”, Report: Information Technology & Innovation Foundation (October 27, 2025).

The Biden administration also helped to secure the massive amounts of funding that Silicon Valley demanded. Here, the Gulf came in handy. In June 2023, the White House brokered meetings between Sheikh Tahnoon bin Zayed of Abu Dhabi and senior executives from Microsoft, Google, and OpenAI. Around the same time, Secretary of Commerce Gina Raimondo was personally acting as Sam Altman’s sherpa among the GCC powerbrokers as well. Partly by dint of these efforts, GCC funding for US-based AI companies increased fivefold in 2024. Public disclosures indicated that Sanabil Investments, a subsidiary of Saudi Arabia’s Public Investment Fund (PIF), offered backing to the venture capital houses that helped to sustain Silicon Valley’s AI ecosystem: Coatue Management, Insight Partners, Andreessen Horowitz, Founders Fund, Radiate Ventures, and General Atlantic. Abu Dhabi’s predominantly state-owned MGX and G42 also directly financed the “hyperscalers”—the cloud-computing companies such as Amazon Web Services, Oracle, and Google—determined to expand American AI capacity. MGX stood in as one of the primary backers of OpenAI during a $6.6 billion funding raise in October 2024, only months after Mubadala, the emirate’s second-largest sovereign-wealth fund, took over the significant equity position that Sam Bankman-Fried’s FTX held in Anthropic.9Mackenzie Sigalos, “FTX estate selling majority stake in AI startup Anthropic for $884 million, with bulk going to UAE”, (<)em(>)CNBC (<)/em(>)(March 25, 2024). Elizabeth Dwoskin, Ellen Nakashima, Nitasha Tiku, and Cat Zakzrewski, “How the authoritarian Middle East became the capital of Silicon Valley”, (<)em(>)Washington Post (<)/em(>)(May 14, 2024). Kate Rooney and Kevin Schmidt, “Middle Eastern funds are plowing billions of dollars into hottest AI startups”, (<)em(>)CNBC (<)/em(>)(September 22, 2024). On the breadth of the PIF’s capital within the venture capital scene, see: Jessica Matthews, “Silicon Valley and Saudi Arabia are still closely intertwined despite age-old controversy,” (<)em(>)Fortune (<)/em(>)(April 4, 2023).

Abu Dhabi had been flirting with Chinese AI alternatives during the first half of Biden’s tenure, but secret negotiations between Raimondo’s Commerce Department and the leadership of G42 eventually persuaded the company to divest from Chinese technology firms and remove Huawei chips from its AI data centers. The pivot away from China was only partial, as G42’s holdings in China’s ByteDance (TikTok) were transferred to another state-owned vehicle (Tahnoon bin Zayed’s Lunate), while the UAE continued to partner with China on 5G, drone, and military tech. Yet, even so, this climbdown brought Abu Dhabi closer to the American AI camp. It not only paved the way for Microsoft to sign a $1.5 billion cloud-computing and AI deal with the UAE in April 2024; it also put the country’s resources (financial and energy), as well as its access to global South markets, at Silicon Valley’s disposal.

Gulf onshoring

The second Trump administration is now using its AI policy to serve the hyperscalers, albeit with moments of incoherence and irrationality along the way. On his first day back in office, Trump issued an Executive Order titled “Removing Barriers to American Leadership in Artificial Intelligence.” This deregulatory reform took aim at the Biden administration’s already exceedingly weak consumer protections and reporting requirements. Trump’s Department of Justice also moved to free the tech giants from antitrust-related worries. As of August 2025, Attorney General Pam Bondi had dropped more than a third of the lawsuits and investigations involving tech inherited from the Biden administration. Last spring and summer, Trump’s Executive Order “Advancing Artificial Intelligence Education for American Youth” and his AI Action Plan pledged to rip up “red tape,” pushing AI adoption into both US K-12 education and what would soon be rebranded the Department of War, protecting American intellectual property, and removing barriers to building new data centers and power generation facilities. This was followed by a December 2025 Executive Order that aimed to block state governments from imposing or enforcing regulations on AI.10Leonie Allard and Julian Blum, “US foreign policy: power in the age of AI”, Report: Institut Montaigne (2025). Adi Robertson, “US removes ‘safety’ from AI Safety Institute”, (<)em(>)The Verge (<)/em(>)(June 4, 2025). Rick Claypool, “Deleting tech enforcement”, Report: Public Citizen (August 2025). Pursuant to the Action Plan’s designs for the Department of War—and funded by the $13.4 billion expressly allocated for AI adoption in the Pentagon’s budget—note that Pete Hegseth et al launched an AI Acceleration Strategy this past winter.

Encouraged by the White House, GCC capital has continued to flow into Silicon Valley. MGX and G42 committed to investing $1.4 trillion in the US over ten years. MGX also participated in a large Series C funding round for Elon Musk’s xAI and helped fund a $10 billion capital raise for the US AI platform developer Databricks.11Apart from venture capital commitments, Saudi’s PIF significantly increased its holdings in Amazon in the first quarter of 2025—a leading AI developer in its own right—lifting its position to 1.2 million shares. Steve Holland and Federico Maccioni, “UAE commits to $1.14 trillion US investment, White House says”, (<)em(>)Reuters (<)/em(>)(March 21, 2025). On Databricks, see: Marlize van Romburgh, “Databricks raises $10B in 2024’s largest venture funding deal”, (<)em(>)Crunchbase News (<)/em(>)(December 17, 2024) After Trump’s visit in May, the rate of Gulf funding to Silicon Valley dramatically accelerated. Anthropic’s $13 billion funding round last September included the Qatar Investment Authority (QIA) as a “significant investor,” and QIA joined the UAE’s MGX in supporting a $20 billion capital raise for xAI. Notably, these investments have often relied on capital channeled through personal patronage networks.12Mark Bergen and Adveith Nair, “Anthropic stake propels Qatar’s $524 billion wealth fund deeper into AI”, (<)em(>)Bloomberg (<)/em(>)(September 3, 2025). “Elon Musk’s xAI raises $20 billion in Nvidia-backed funding round”,(<)em(>) Agence France-Presse (<)/em(>)(January 7, 2026) Shortly before Trump’s inauguration, representatives of Tahnoon bin Zayed bough a 49 percent stake in World Liberty Financial, a crypto venture led by the Trump and Witkoff families, for $500 million. Two weeks prior to the President’s May 2025 visit to the Gulf, MGX committed an additional $2 billion of its own capital to the Trump-Witkoff crypto firm.13Sam Kessler, Rebecca Ballhaus, Eliot Brown, Angus Berwick, “’Spy sheikh bought secret stake in Trump company”, (<)em(>)Wall Street Journal (<)/em(>)(January 31, 2026). Eric Lipton, David Yaffe-Bellany, Bradley Hope, Tripp Mickle, and Paul Mozur, “Anatomy of two giant deals: the UAE got chips. The Trump team got crypto riches”, (<)em(>)New York Times (<)/em(>)(September 15, 2025).

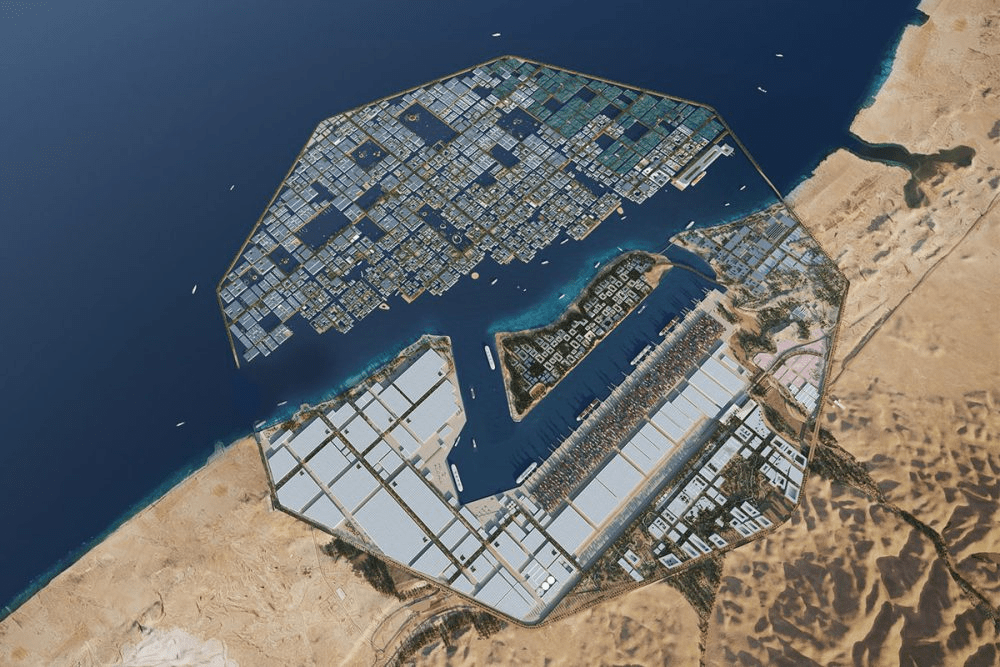

Arguably even more consequential is the Gulf states’ recent move to “onshore” AI: not just pumping cash into the hegemon, but harnessing its technological capacities as part of their own domestic development plans. MGX, for example, has joined a consortium led by Nvidia, Microsoft, Blackrock, and xAI to purchase Aligned Data Centers for $40 billion, a company now exploring the possibility of issuing as much as $50 billion in debt to expand its AI portfolio. Then there is Stargate UAE, a one-gigawatt AI compute cluster joint venture between OpenAI, Nvidia, Cisco, SoftBank, and G42. In November 2025, the US Commerce Department officially cleared G42 to acquire tens of thousands of GB300 servers for the project.

The White House fully backs the plan to build out Gulf-based AI compute clusters and has thrown its weight behind a number of joint ventures. Qatar and the UAE have signed on to the White House’s “Silicon Declaration,” a pact for developing the supply chain and digital infrastructure needed for AI development. Saudi planners have now begun redirecting efforts and capital toward constructing their own AI data center hub: just last year, the PIF and xAI launched Humain, a “national champion” for AI, to operate the data centers using the country’s newly purchased Nvidia GB300s. Its CEO, Tareq Amin, says he wants to bring 6.6 gigawatts of AI compute capacity online by 2034—meaning that Saudi Arabia would bear 6 to 7 percent of the world’s AI workload, a market share surpassed only by the US and China. In November 2025, Humain and Nvidia established a strategic partnership specifying that the former may purchase up to 600,000 graphics processing units (GPUs)—the specialized electronic circuits used to train AI models—from the latter over the next three years. The trade press suggests that these chips will be used in data centers in both the US and Saudi Arabia. In the US, data centers are to be managed under a joint venture between Humain and Global AI, an AI infrastructure company founded by former IBM executives. In Saudi Arabia, Humain and Amazon Web Services are developing a dedicated AI facility near Riyadh expected to use Nvidia’s wares. Meanwhile, reporting suggests Sam Altman has been pressing to raise $50 billion or more from the Gulf’s leading sovereign wealth funds since early 2026.14“Humain expands strategic partnership with Nvidia, advancing global AI infrastructure with xAI, Global AI, and AWS at the US-Saudi Investment Forum”, Humain (November 19, 2025). Adam Satariano and Paul Mozur, “Saudi Arabia’s new power play is exporting A.I. to the world”, (<)em(>)New York Times (<)/em(>)(October 27, 2025). Pramod Kumar, “Humain invested $3bn in xAI before merger with SpaceX”, (<)em(>)Arab Gulf Business Insight (<)/em(>)(February 19, 2026). “Is OpenAI betting its future on the GCC? Altman’s big ticket pitch to Middle East investors”, (<)em(>)Tech Revolt (<)/em(>)(January 23, 2026).

The GCC’s ability to combine subordination to the US private sector with national investment throughout the tech value chain is impressive. OpenAI now deploys its most advanced open models from data centers in Saudi Arabia, and xAI will soon be training its proprietary models there, too. Gulf powers are building out their own vertically integrated AI operations, with Humain and G42 developing AI infrastructure, model training, and consumer applications. Humain is also currently piloting a voice-powered product it hopes may one day challenge Windows, MacOS, and the other global leaders in computer operating systems.15Tala Alrajjal, “Saudi Arabia is making a massive bet on becoming a global AI powerhouse”, (<)em(>)CNN Business (<)/em(>)(November 2, 2025).

In sum, the combination of American capitalism’s reliance on Silicon Valley and the self-destruction of its state-led R&D capacity has caused Washington to cede leadership of AI development to the dominant corporate players in the field. The Gulf’s relative abundance of financial resources, access to cheap electricity, and power generation capacity has brought those players—all of whom have built their business strategies on the scaling of compute—to see the GCC’s monarchies as essential allies. And those monarchies are now vying to become AI powerhouses in their own right with the blessing of the Trump administration.

Service to empire

The GCC’s bet on Silicon Valley can be attributed to a few major factors.16N.B.: Saudi Arabia remains connected to Chinese entities in a number of AI-related domains. KAUST continues to have a number of research partnerships. Aramco integrated DeepSeek models into its Dammam data centers and Alat, a PIF subsidiary, has a $2 billion joint venture with Lenovo for the manufacturing of data servers. See, also, Tahnoon bin Zayed’s investment firm Lunate. The first is technical: for now, Nvidia produces chips at the industry frontier, which makes it rational for the Gulf to align itself with American tech. The second is ideological: Mohammed bin Salman’s fascination with US-styled tech futurism—and its cyberpunk aesthetic—is well documented, and OpenAI’s Altman describes Tahnoon bin Zayed as a “dear personal friend.” Yet the third and most salient factor is the set of incentives, restraints, and path dependencies imposed by the region’s existing position within the American empire, which long predates the AI boom.

The GCC’s integration into the US-led post-war order began in 1933, with Standard Oil of California’s securing of an oil exploration concession in Dhahran, and consolidated after 1974 when agreements on petrodollar recycling—investing export earnings in Wall Street banks—were reached with Washington. For the Gulf regimes, domestic capital accumulation had been premised on these tributary responsibilities; the most obvious sign of the Arabian Gulf’s service to US empire was the countries’ pricing of oil in dollars and their rerouting of oil receipts into US-dominated capital markets. With time, however, the Gulf’s subservient position pushed it to accept a more meaningful role in propping up the financial health of the US. In the 1990s, Saudi Arabia’s Olayan Group expanded its position in Chase Manhattan Corp, while one of the country’s royals, al-Walid bin Talal, rode to the rescue of Citicorp when it was in peril in 1991.17Michael Quint, “Saudi prince to become Citicorp’s top stockholder”, New York Times (February 22, 1991). Sarah Barlett, “Saudi group now owns over 5% of Chase stock”, New York Times (April 23, 1991). The 2008 global financial crisis consolidated this dynamic, as the Abu Dhabi Investment Authority moved quickly to save Citigroup while Gulf purchases of US sovereign debt became critical to the “success” of the Fed’s Quantitative Easing program.18Ben Bernanke, 21st Century Monetary Policy: The Federal Reserve from the Great Inflation to COVID-19 (W.W. Norton & Company: 2022). Per Bernanke, Gulf treasury purchases drove US borrowing rates down by ~1% between 2005 and 2014.

Once the crisis began to abate, GCC investment proved equally critical for the tech-dependent recovery out of the US Great Recession. During this period, GCC members became ever more conscious of the need to diversify their national economies away from oil and gas. Partly because of the close handful of consultancy firms that advise each of these governments, their national strategies closely resembled one another, with Abu Dhabi, Dubai, Saudi Arabia, Qatar, and Kuwait all rolling out “Vision” plans with the same basic template. For the UAE and Saudi Arabia in particular, this meant taking a greater interest in AI. By the late 2010s, Saudi capital had become the single largest source of investment in the startups that had sprung up in the environs of San Francisco.19Eliot Brown and Breg Bensinger, “Saudi money flows into Silicon Valley—and with it qualms”, Washington Post (October 16, 2018). The state murder of Jamal Khashoggi briefly interrupted the burgeoning Saudi–Silicon Valley relationship (Altman left the board of Neom in protest) but the backlash soon subsided into a return to business as usual. Throughout the post-Covid credit crunch, Saudi and Emirati money continued to backstop personal fortunes and restore stock prices for Silicon Valley’s leading lights.

The Gulf’s relations with Silicon Valley are also underpinned by the logic of regime security. In using their capital to support a sector-cum-class fraction that is central to the American economy and state, the GCC countries are expecting Washington to reciprocate, backstopping the royals’ hold on power in an increasingly volatile Middle East. It is telling that Saudi Arabia’s recent Nvidia deal arrived after Mohammed bin Salman and Trump signed a new Strategic Defense Agreement, which, along with provisions on civil nuclear energy cooperation, stipulated sizable Saudi purchases of US military kit. These will include an unspecified number of F-35 fighter jets, history’s most expensive weapon system, and golden goose for Lockheed Martin.20Ashley Roque, “F-35, tank sales part of new US-Saudi strategic defense agreement”, Breaking Defense (November 18, 2025). Dan Grazier, “Has the Pentagon learned from the F-35 debacle?, Analysis: Program on Government Oversight (June 8, 2023). Rich Smith, “Lockheed scores blockbuster $24 billion sale of 296 F-35s”, The Motley Fool (October 12, 2025). This is AI investment qua protection money.

Best laid plans

What might this alignment mean for the future? With their new attempt to import AI compute power, the leading Gulf regimes have been told of unique opportunities for rent extraction. In 2022, McKinsey analysts posited that AI adoption could add $150 billion to GCC economies per annum. PwC more recently estimated that AI will contribute a minimum of $135.2 billion (or 12.4 percent projected GDP) to the Saudi Arabian economy as of 2030, and $96 billion (or 13.6 percent GDP) to the UAE’s.21Niklas Berglind, Ankit Fadia, and Tom Isherwood, “The potential value of AI—and how governments could look to capture it”, Article: McKinsey & Company (July 25, 2022). Shivangi Jain, “US $420 billion by 2030? The potential impact of AI in the Middle East”, Report: PwC (2025). The two firms’ projections represent mainstream consensus: setting the world economy as the scale of analysis, Goldman Sachs forecasts generative AI boosting global GDP by 7 percent over the next ten years on its own, while McKinsey claims generative AI will boost labor productivity by 0.1 to 0.6 percent annually through 2040. These huge projections are already giving rise to novel institutional configurations, with the creation of new planning, regulatory, and financial bodies, as well as corporate entities that might serve as lead investors.22 In the UAE, Tahnoon bin Zayed al Nahyan directs the campaign. Research concentrates in the Mohamed bin Zayed University of Artificial Intelligence—which has recently opened a research lab in Sunnyvale, California—and in the Technical Innovation Institute, which has pioneered Arabic-language LLM models like Falcon. Over in Saudi Arabia, the Saudi Data & AI Authority (SDAIA) bears responsibility for setting the course. Founded in 2019, the SDAIA is chaired by the Crown Prince. In addition to taking the lead with research—often through joint ventures with Chinese partners—much of the state’s early venture capital and technological transfer efforts ran through King Abdullah University for Science & Technology (KAUST). The PIF-established Humain, however, is now the lead institute for directing AI investment and developing a domestic AI stack, involving a host of other public entities and private partnerships.

But threats are looming. The most immediate are downstream from the Iran war. Tehran has demonstrated its capacity not only to dictate terms in the Strait of Hormuz but to threaten US allies to its west whenever it chooses. The US has meanwhile proved that it lacks both the will and the means to protect its clients in the GCC from the fallout of its disastrous military adventure. Its protection racket only extends so far. With no stable political resolution for the region in sight, the Gulf’s dreams of developing major AI infrastructure could come to naught.

Even if the status quo ante were to be restored, the systemic financial risks presented by Silicon Valley’s AI model may well undermine the medium-term outlook of US-Gulf schemes for global AI dominance. The extraordinary rate of cash burn by American start-up technology developers, the unprecedented capital expenditures from hyperscalers (more than $800 billion expected in 2026), the circular relations binding key players in the industry, and Silicon Valley’s general disregard for revenue generation all make the Gulf’s long-term economic forecasts look uncertain.23“David Sacks Says AI Could Drive 75% Of US GDP Growth As Morgan Stanley Sees Big Tech AI Capex Surging Past $800 Billion In 2026,” Yahoo Finance, May 5, 2026. While investors were previously willing to ignore the yawning gap between AI expenditures and revenues, this began to change in the early months of 2026, amid the disorder unleashed by the second Trump administration. After an earnings call at the end of January, Microsoft shed $357 billion in market capitalization in a single day.

There are more reasons to believe that the chickens might soon come home to roost. Oracle has issued billions in debts in order to build data centers that OpenAI (among other companies) has pledged to lease; yet OpenAI’s ability to honor its pledges hinges on the firm continuing to raise funding from the likes of Nvidia and SoftBank—both of which have signaled that they may be backing out of their non-binding commitments. Should key American partners fall on hard times, the knock-on effects could compromise the GCC’s finances and plans to develop national AI stacks.

The Gulf’s projected capital expenditure on AI data centers further complicates the financial picture. According to S&P’s projection, the megawatt load of the Saudi Arabian data center sector will experience 29 percent compound annual growth between 2024 and 2030. An increase of generating capacity at that scale will need to be met by a major surge in demand; otherwise, losses resulting from overcapacity could be enormous. And this is irrespective of the significant challenges of managing chip obsolescence, as the existing cutting-edge chips may be surpassed within five to seven years. With the Gulf’s so-called AI national champions troubled by shortages in skilled labor—despite large Saudi and Abu Dhabi investments in education and training, and despite offering huge pay packages—the obstacles to success are daunting.24Mai Barakat, “The Saudi Arabia data center market: a catalyst for economic innovation”, Special Report: S&P (December 2025). Chris Hamill-Stewart and Megha Merani, “$1m salaries, but Gulf still can’t woo enough AI talent”, Arab Gulf Business Insider (August 25, 2025).

There are broader questions about the underlying developmental utility of the AI industry. At this juncture, there is little basis to assume AI will generate substantial enhancements in productivity. Globally, the data suggests that AI’s most immediate labor-market effect is to wipe out what were previously secure entry-level jobs, especially in software and related industries. Saudi Arabia is already struggling with a youth unemployment rate of around 15 percent. It takes Saudi high school and university graduates forty weeks on average to secure employment. Studies from the King Abdullah Petroleum Studies and Research Center identify women and youth as those most vulnerable to AI-derived job displacement.25Erik Brynjolfsson, Bharat Chandar, Ruyu Chen, “Canaries in the coal mine? Six facts about the recent employment effects of artificial intelligence”, Working Paper: Stanford Digital Economy Lab (August 2025). “Slow transitions drain billions from Saudi economy”, Wamda (November 17, 2025). Cian Mulligan, “AI and green jobs in the Saudi labor market: exposure and complementarity”, Report: King Abdullah Petroleum Studies and Research Center (November 2025). To ignore these warning signs and inject AI into the ailing Kingdom is to risk causing major social pain.

AI’s ecological impact must also be considered in relation to the Gulf’s climatic challenges, not least in Saudi Arabia, where the state plans to use natural gas-fired plants to supply electricity to the AI clusters under construction. With data centers sited in locations far too hot for optimal performance, the fact is that the emissions bill for cooling these facilities—even where more efficient air and evaporative systems are deployed—is going to be gigantic. Possibilities for reducing AI’s carbon footprint through the use of solar plants face a number of obstacles, including the intermittency of renewable energy. Even with the Saudis making impressive jumps in grid-scale battery capacity in recent years, the country is a long way off from being able to store the levels of power needed to ensure that data centers are fed with the constant energy supply they require.26Hazel Gandhi and Rina Chandran, “We mapped the world’s hottest data centers”, (<)em(>)Rest of World (<)/em(>)(December 15, 2025). Rachel Millard, “There’s a new ‘breakout star’ in the battery storage market”, (<)em(>)Financial Times (<)/em(>)(February 3, 2026)

The Gulf monarchies have acted as indispensable allies to both the British and American imperial projects, ensuring the circulation of petroleum to the benefit of the wealthiest nations and helping to backstop the global dollar-based financial order. The unashamed role of these regimes in the world-system is to expand the profit share of income. Their rulers have refined the art of exploiting workers at home and extracting value abroad, using petrodollar recycling to plunder the Global South in the 1970s and ’80s, then designing corporate models to skirt labor laws and prevent collective bargaining in the new millennium. They thus have a natural affinity with AI, which is not a simple means for replacing workers so much as a complex tool for degrading, deskilling, speeding up, and outsourcing labor.27Moritz Altenried, (<)em(>)The Digital Factory: The Human Labor of Automation (<)/em(>)(The University of Chicago Press: 2022); Alex Hanna and Emily Bender, “The hidden labor that makes AI work”, (<)em(>)Rest of World (<)/em(>)(July 1, 2025); Jason Resnikoff, “Contesting the idea of progress: labor’s AI challenge”, (<)em(>)New Labor Forum (<)/em(>)33:3 (2024). Gulf participation in the ventures of Altman et al., driven by a combination of economic interest, political expedience, and ideological commitment, is thus the latest stage in a much longer historical trajectory. But while the Gulf states have so far benefited from serving as gilded American proxies, this strategy could backfire in the near future, both because of the volatility created by US aggression and the internal contradictions of the AI boom. Over the coming decade, the health of empire in the Middle East will depend in no small part on whether this Gulf–Silicon Valley nexus can hang together.

Further Reading

Rebuilding the Kingdom

Transformations of state, economy, and class in Saudi Vision 2030

Crown Prince Mohammed bin Salman’s Saudi Vision 2030 promises to transform the oil power’s economy and society. The plan has prompted an enormous wave on...

America’s Braudelian Autumn

Factions of capital in the second Trump administration

In its efforts to revive the American Empire, the Trump administration will have to delicately balance the interests of both manufacturing-oriented nativists and capital factions...

Breaking Up Google

Antitrust, competition, and the intricacies of monopoly

In late August, Judge Amit P. Mehta of US District Court for the District of Columbia found Google guilty of maintaining an illegal monopoly in...