The Political Economy of Brazilian Inflation

Comments Off on The Political Economy of Brazilian InflationOver the past two decades, Brazil has seen two great swings in its distribution of real national income. In the years between 2004 and 2014, the wage share increased progressively. This phenomenon faced severe political resistance. The momentous events of 2015—the impeachment of President Dilma Rousseff and the swearing in of Michel Temer—reflected this resistance and coincided with a reversal in the trend. For the next seven years, wages’ share of national income fell continuously until 2022. The year 2023 marked a possible new inflection point. While the long decline in the wage share finally reversed, however, the return of wage growth has coincided with a resurgence of unhappiness in business and financial circles urging more austere macroeconomic policies, including the central bank’s interest-rate policy.

The theory used by the Central Bank to justify its interest rate setting is the “New Consensus” macroeconomic model (NMC). Since 1999, the National Monetary Council—comprised of the Minister of Finance; the Minister of Planning, Development and Management; and the Governor of the Banco Central do Brasil (BCB)—has determined a central inflation target. The instrument for achieving this target is the BCB’s interest-rate policy. The NMC’s model assumes that inflation grows (or drops) as the result of demand shocks—when actual output is above (or below) potential output—and that “supply shocks,” including external shocks, average out to zero in the long run. Accordingly, the BCB sets the basic interest rate to manipulate aggregate demand and make output equal to potential. The New Consensus model also assumes that, in the long run, such monetary policies are neutral in respect to both the distribution of income and the trend of potential output; it manages inflation by matching short-term aggregate spending to the trend of long-run growth, which are given by supply-side factors.1

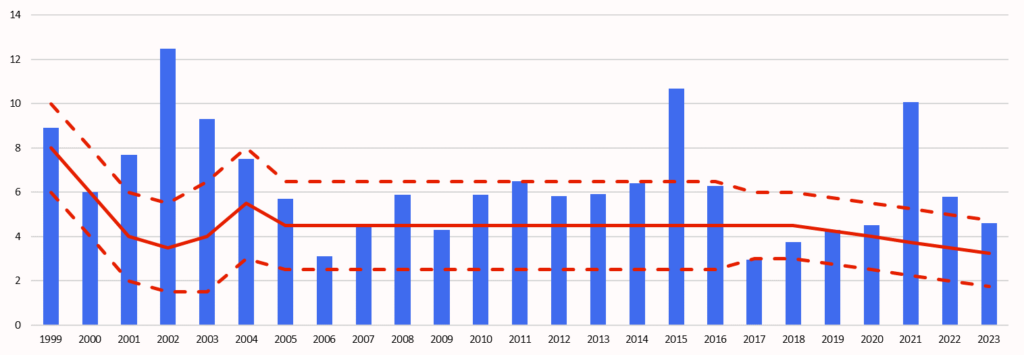

Figure 1: Inflation and target

Historically, between 1999 and 2023 (figure 1), the BCB’s inflation targeting system has been relatively successful on its own terms. Inflation surpassed the target ceiling only in the years immediately following its implementation, between 2001 and 2003, and then specifically in a few individual years: 2015, 2021 and 2022.

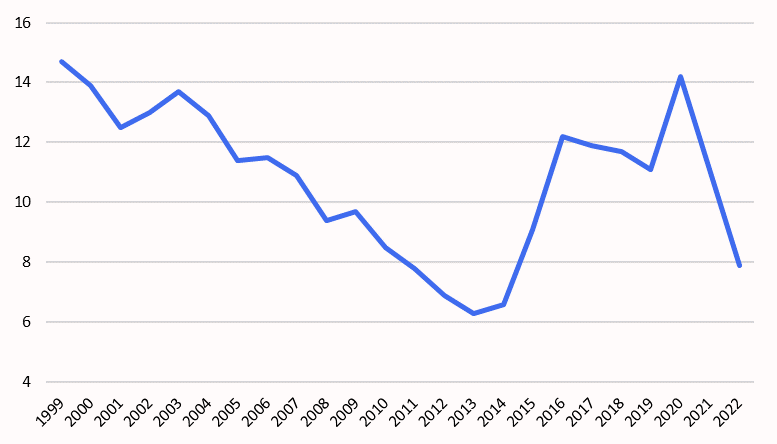

This success regarding inflation control, however, did not occur through the transmission channel the New Consensus model assumes. Figure 2 illustrates that the behavior of Brazil’s unemployment rate under the current inflation-targeting. The years in which inflation was higher and above the target limit are exactly the same years in which the unemployment rate was also higher—rising prices coincided with the cooling, not the heating, of the Brazilian economy. Moreover, periods with low unemployment rates correspond to stable inflation rates within the target range. Since the adoption of its inflation-targeting regime, therefore, Brazil has seen inflation that is not systematically associated with labor shortages.

Figure 2: Unemployment rate (%)2

How can the success of Brazil’s inflation-targeting policy therefore be explained? If the relationship between aggregate demand dynamics and inflation are the opposite of what the “New Consensus” expects, then there must be an alternative explanation for the political economy of Brazilian inflation—the relationship between the government’s macroeconomic policies, inflation, and the distribution of income across the institutions mediating between the two. Instead of the “New Consensus” model’s assumption that policy transmits to inflation through the real interest rate’s effects on aggregate demand, there is a more appropriate framework for explaining the success of Brazilian inflation targeting. This is the idea that trend inflation isn’t demand-pull, but cost-push, and results from distributive conflicts. This “cost-push” and “distributive conflict” framework for understanding inflation has important implications, for it also explains the consequences of inflation targeting on the distribution of income and the political processes that influence macroeconomic policy.

Production costs and distributive conflict

Contrary to the insights of the “New Consensus” model, approaching inflation as a cost-side phenomenon is also compatible with explaining the trend of long-run growth as driven by effective demand. According to this view, the level of effective demand determines much more than current output. It also determines the economy’s productive capacity—potential output and this explains, in general, the fact that there is a relative abundance of labor in relation to the capital stock that comprises that capacity. The stock of capital adjusts itself through investment according to the trend of effective demand.3 In light of this, the idea that the trend of inflation is due only to current excess demand deserves to be questioned. After all, a demand-pull inflation would only occur when the level of effective demand—aggregate monetary expenditures measured at supply prices—were above the full-employment level of output. This situation would reflect a shortage of productive resources and would be temporary since inflation itself would diminish aggregate spending in real terms to a level compatible with production at full capacity.

Brazilian inflation in the past two decades, however, occurred when production was below potential and persisted over time. Instead of reflecting a shortage of productive resources and having a tendency of being only temporary, cost-push inflation and distributive conflict occur before the economy reaches a situation of scarcity. That is, these models show how it is possible for nominal wages to increase before the economy fully employs the labor force. Inflation can persist, permanently, in this scenario, reflecting the distributive incompatibility of rival claims over the existing output, below potential. In general, however, distributive conflict results in inflation and not in acceleration of inflation.4

Wage bargaining is a fundamental form of distributive conflict. Even if the economy isn’t anywhere near reaching full-employment, persistently low (or high) unemployment rates can strengthen (or weaken) labor’s bargaining power, subject, of course, to the broader political and institutional context—the labor laws, trade union organization and leadership, social insurance protections, etc., that influence the bargaining process. A wage-induced inflation process arising from worker’s bargaining power in an economy that is abundant in labor, even if influenced by a higher level of activity in the labor market, reflects a phenomenon of cost and distributive conflict, not one of demand.

Besides labor costs, the increase in production costs is also greatly influenced by government-regulated prices of certain goods and services, as well as by the prices of tradable goods (final and intermediate goods that a country exports and imports) set in global markets and converted by the nominal exchange rate into local currency prices.5 These two sources of inflationary pressure can intensify the distributive incompatibility of claims by impacting real wages and profit margins. Under this approach, the cost-push inflation related to tradables and administered prices, as well as the one induced by wages, are not neutral from the distributive point of view.

Monetary policy transmission channels

Although the Banco Central do Brasil has been relatively successful in keeping Brazil’s inflation close to target under its “New Consensus” inflation-targeting system, there are three main reasons why higher interest rates don’t lead to a systematic control of inflation through the aggregate-demand channel. First, there are a series of institutional factors that impact the regularity of the relationship between the real basic interest rate and consumer credit for durable goods and residential investments, such as spreads of state-owned banks, payroll loans, and housing policies, in addition to household debts. Second, changes in the interest rate can produce shifts in the exchange rate and impact demand in the opposite direction: currency devaluation resulting from an interest rate reduction can suppress real wages and consumption more than it expands demand through an increase in net exports. Third, variations in nominal wages seem to respond very little to the deviation of the unemployment rate from its trend. Only sustained unemployment rates, high or low, seem to have persistent effects through the demand channel over wage trends.

Factors related to production costs, on the other hand, are systematically related to the BCB’s interest rate policy. The main transmission channel between interest rates and production costs is the effect on the nominal exchange rate. A nominal interest rate higher than the international interest rate (plus sovereign spread) leads to a positive interest differential, which is usually associated with a trend of local currency appreciation. This happens because a positive (negative) interest rate differential tends to impact the inflow (outflow) of short-term capital flows which, in addition to other elements of the balance of payments, are central to determining the nominal exchange rates. Besides that, with the exchange rate’s “adaptive” or endogenous expectations, floating exchange rate regimes can favor speculation and instability. Consequently, a change in the nominal exchange rate usually alters the expected exchange rate in the same direction, intensifying the exchange rate appreciation or depreciation process.6

In Brazil’s case, the nominal exchange rate plays a fundamental part in determining the inflation rate. First because it directly influences tradable goods’ prices. Note that the exchange rate not only impacts the price of intermediate and final goods Brazil imports but also those that the country exports: exporters don’t sell their products in the domestic market at a different price than the one set for the international markets. Second, tradable prices are inputs into the indexes used for government-administered prices, such as the IGP—a price index that regulates the adjustments of a series of rental agreements and of the government-led price management process. Both factors impact the cost of production of all other economic sectors; the exchange rate significantly affects Brazil’s internal price dynamics. Whether the BCB achieves its target therefore depends to a high degree on prices in global trade markets (in dollars) and the exchange rate, which in turn determine prices that cascade throughout the national economy. In other words, the transmission channel from the interest rate to the exchange rate reveals a lot about how inflation is actually controlled (or not). The years in which inflation didn’t reach the target range are very much related to great currency devaluation episodes.7

The determinants of Brazil’s inflationary dynamic under Inflation-targeting

Through an empirical analysis of Brazil’s inflationary dynamic under inflation-targeting and its results regarding income distribution from 1999 to 2014, we can differentiate these variables’ behavior in two moments.8 The first one encompasses the years between 1999 and 2003, marking the implementation of New Consensus inflation targeting during Fernando Henrique Caardoso’s administration (1999–2002) and the first year of Luís Inácio Lula da Silva’s inaugural term in office (2003–2006). The second moment regards the period between 2004 and 2014, a timeframe that includes the seven following years of Lula’s first two terms (2003–2006 and 2007–2010) and the four years of Dilma Roussef’s initial term in office (2011–2014).

Immediately after the Cardoso administration’s adoption of central bank inflation targeting, between 1999 and 2003, the inflationary target was widely unfulfilled (figure 1). This resulted from (i) pressure from the imported inflation, which was caused by a currency devaluation process in a context of external instability; and (ii) high inflation of managed prices (figure 4). Overall, nominal wages’ growth rate was kept below inflation, leading to real wage losses and to a decrease of the wage share (see figure 6).

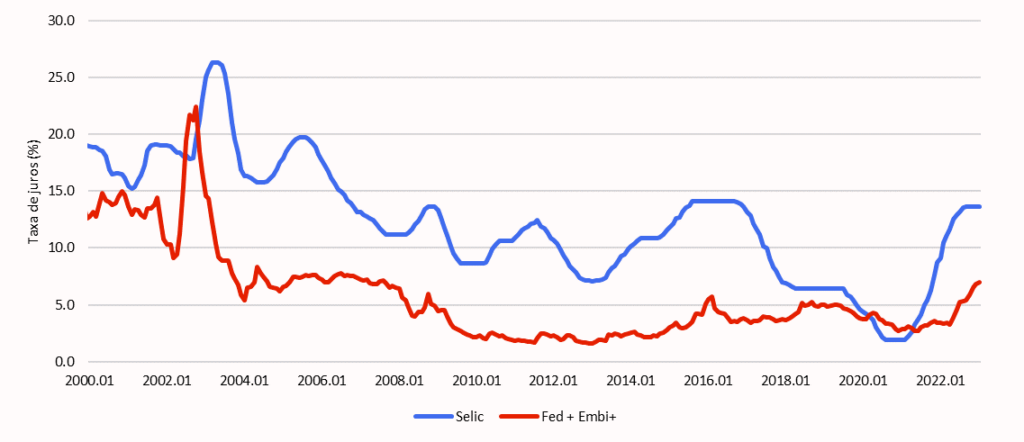

It is worth noting that in this international instability context, the interest rate differential—measured by the difference between the basic domestic rate and the basic international rate (the last one measured by the Fed’s basic rate added by the sovereign spread estimated by the EMBI)—decreased significantly (figure 3). Indeed, this differential became negative in 2002, once the great rise in sovereign spread wasn’t compensated by a sufficiently large increase in the domestic interest rate.

Figure 3: Nominal interest rate differential

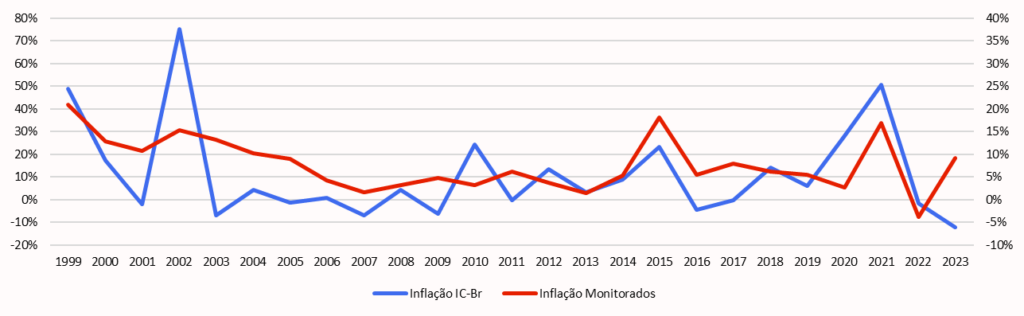

The currency devaluation process, therefore, was largely influenced by the interest rate differential operating at the time. Figure 4 illustrates the imported inflation’s behavior, that is, the price’s variation in dollars in addition to the nominal exchange rate variation, as well as the behavior of the inflation regarding regulated prices.9 It is evident that both indicators have contributed for inflation to not reach the target in the 1999 and 2003 period.

Figure 4: “Imported” inflation and regulated prices inflation (annual aggregate)

The imported inflation rate is shown in the left axis whilst the regulated prices inflation is exhibition the right axis

Between 2004 and 2014 the inflation target was met every year. Success, however, didn’t result from interest-rate control of demand. This period was also marked by a continuous decline in the unemployment rate as the product of a heated economy (figure 2). Rather, inflation was kept low by an improvement of the Brazilian international trade and finance situation—from a progressively better-managed balance of payments. Two factors allowed for Brazil to reduce its domestic interest rate whilst maintaining a high interest differential and accumulating reserves. Resulting from the commodities’ price rise and the increase in export volumes, there was Brazil’s trade balance enhancement. Financial accounts also improved, since there was an increase in international liquidity in the context of the US Fed’s low interest rate and the consequent compression in sovereign spreads.

These movements occurred in concomitance to a currency valuation process which, despite the commodities’ price rise in dollars (US$), was translated into a lower imported inflation in reais (RS) compatible with the inflation target. Additionally, the regulated prices inflation was lower, as a consequence emerging partially from the currency valuation itself (and its effects over the IGP index) but also from changes in the pricing rules of these goods and services promoted by the government and by state enterprises (see figure 4).10

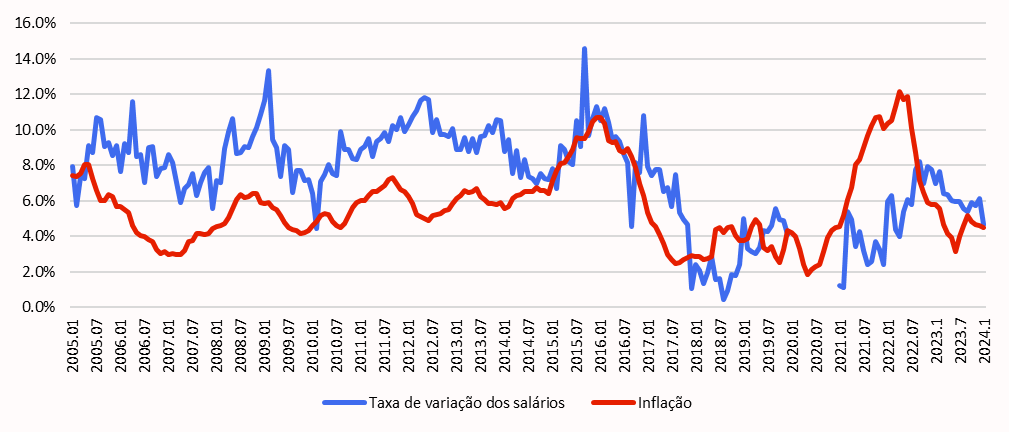

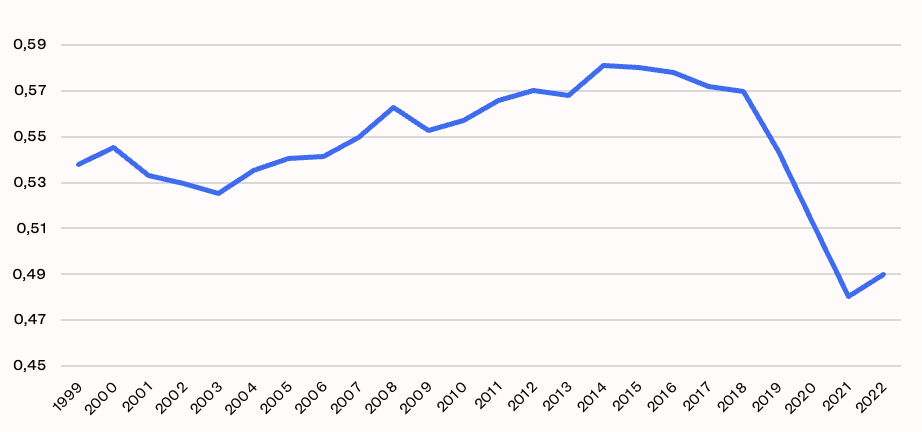

Wages, nonetheless, had a distinct behavior between 2004 and 2014 when compared to the years from 1999 to 2003. The most recent period was marked by what we call the “undesired revolution” in Brazil’s labor market.11 This decade allowed for the strengthening of workers’ bargaining power for a series of reasons, such as (i) the policy of wages’ real increase and the broadening of social policies coverage; and (ii) the structurally lower unemployment rate, resulting from higher economic medium growth rates, broad job creation in the service sector, and minor expansions of the labor force due to demographic reasons. Consequently, between 2004 and 2014, the wages’ inflation was above the inflation rate itself (figure 5) and there was a real increase in wages (higher than productivity).12 The distributive result of such a phenomenon is observable on the share of wages’ increase in the national income functional distribution during that period (figure 6).

Figure 5: Wages inflation and prices inflation (as accumulated in 12 months)

The wages series’ discontinuity is explained by the changes applied in the CAGED methodology in 2020.

Figure 6: Share of wages in the national income13

Measurements used for updating the dataset were based on Miebach and Marquetti (2019).

What comes after the “undesired revolution”?

The events from 2015 onwards can be understood from this same analytical framework. Even though inflation was within the target during 2004 and 2014, the distributive conflict was aggravated by the “undesired revolution,” gradually creating political consensus regarding the need to change Brazil’s economic policy.

This takes us back to the work of Michal Kalecki. During the Great Depression, World War II, and the spread of macroeconomic thinking and policy across the post-war world, Kalecki drew attention to the possibility that an expansionary economic policy capable of generating a long-lasting and low unemployment rate, and consequently strengthening worker’s bargaining power, could be reversed in the face of a growing opposition from a ruling class of employers and owners.14 Such an opposition would occur both due to political aspects (e.g. a loss of “factory discipline”) and economical aspects of full employment (e.g. decreasing profit margins and increasing wage shares of income).15 He pointed out that such a ruling class would act to convince the government to change the direction of economic policy, slowing growth down and increasing unemployment rates.

The first year of Dilma Roussef’s second term as president (2015–2016) saw this political economy dynamic at work. It was marked by a profound political instability and by the narrow win in the 2014 presidential elections. In the beginning of 2015, the government drastically altered the direction of economic policy and promoted a strong contraction of demand through many different instruments.16 This change was carried out in the context of accelerated reduction in state-owned enterprises’ investments as a response to the allegations of the Lava Jato Operation. The transformation simultaneously included a strong fiscal adjustment, contraction of public credit, interest rate hikes, exchange rate depreciation, and the increase of administered prices.

If such economic measures were greatly contractionary, causing the GDP to fall sharply and the unemployment rate to rise significantly, they were also inflationary policies. In 2015, the inflation rate was above the target cap, which is explained by the increase in both imported inflation and regulated prices’ inflation. In the following year, the inflation rate decreased again as the currency depreciation and administered prices’ effects were fading. Still, unemployment was kept at a high rate, putting a stop to the process of real wage growth and creating an ideal environment for the implementation of reforms destined to reduce labor and social rights in order to permanently curb workers’ bargaining power. In effect, from 2015, especially after Dilma’s impeachment and Michel Temer’s inauguration (2016–2018), followed by Jair Bolsonaro’s victory in the presidential elections (2019–2022), Brazil adopted a series of austerity measures, putting an end to real wage growth, rolling back social policies, enforcing labor and pension reforms, and implementing a public spending cap.

In the face of a sharp reduction in workers’ bargaining power, nominal wages started to grow below inflation between the years of 2016 and 2019 (figure 5). As a result, the wages’ share in the functional income distribution decreased continuously in this period (figure 6). The inflation rate also considerably decreased as a consequence of the low nominal wages’ growth as well as of the lack of robust pressures of imported inflation and administered goods-and-services’ prices. Once again, Brazil met its inflation target.

The Covid-19 pandemic magnified this redistributive tendency. On the one hand, the 2020 recession expanded the unemployment rate even further. On the other hand, there was a strong increase in both imported inflation and regulated prices’ inflation, resulting from a sharp currency depreciation in addition to high dollar prices on tradable goods and services (mainly those related to energy costs). The latter reflected a high global inflation consequent to logistical problems in global value chains and the war in Ukraine’s effects on global commodities markets.

Besides echoing a global movement of emerging countries’ currency devaluation, it is worth noting that the strong exchange rate devaluation between 2020 and 2021 was deepened by the BCB’s policy of determining the country’s interest rate. Figure 3 exhibits how the BCB fixed its basic interest rate below international rates set in the US in this period, as it did in 2002. This led to a process of nominal exchange rate devaluation.17

From the beginning of 2022, the turn in BC’s interest policy that resulted in a process of basic rate’s increase seems to have contributed to the control of the imported inflation by a reversion in the currency devaluation movement. Additionally, a deflation in managed prices resulted from the adoption of a punctual public policy of price control – most notably the control over gas prices implemented in the last year of Jair Bolsonaro’s term, 2022, which was also marked by his defeat in the presidential elections against Lula – whose term started in the following January (2023–2026).

Brazil’s inflation rate was once again within the target range in 2023, a result that seems to be much more related to those cost elements than to factors regarding aggregate demand. Despite the cycle of increases in nominal interest rates by the BCB, employment expanded continuously in 2022 and 2023. Among other reasons, this occurred because of a more expansionary fiscal policy. Despite the unemployment rate’s drop, wage increases only partially offset losses due to inflation, leaving a gap to absorb wage pressure and avoid higher inflation levels. The distributive result of this movement was an increased wage share in the national income during the 2020–2022 period—as figure 6 shows.

Brazil’s disguised incomes policy

The analysis of Brazilian inflation behavior under the targeting regime, based on the cost-push inflation approach and on the distributive conflict perspective, allows us to identify three central elements to the country’s recent macropolicy. The first one regards the 2004–2014 distributive conflict intensification and its positive effects over real wages, resulting in a permanently higher but stable inflation rate, although not in acceleration of inflation. Coupled with strong control measures over imported and government-regulated prices inflation, this phenomenon was responsible for the inflation rate to stay within the target range throughout the period, even if in some of the years it was above the target center. The second one is that even when the distributive conflict was appeased and the real wages growth was not observable, the inflationary targeting was still highly dependent on imported inflation. The third element, as it has become clear, is that the inflationary process isn’t neutral in distributive terms, not only because it depends on the nominal wages’ behavior and on the workers’ bargaining power, but also because it greatly depends on the exchange rate, the behavior of tradables’ dollar prices, and on the administered prices readjustment policy. All of these variables influence the functional income distribution.

Austerity policies go beyond changing the basic interest rate by the Central Bank, and they must be understood through this context. Ultimately, to curb the wage inflation process by sustaining a high unemployment rate as a measure for reducing worker power is to execute much more of a disguised income policy than a neutral or technical price control policy. Abba Lerner, an historic economist and advocate for the distinction between cost-push inflation and demand-pull inflation, not only criticized policies that aimed at maintaining a high unemployment rate in order to reduce the cost inflation and the distributive conflict, but also offered an alternative to the austerity measures: to link income policies directed at controlling cost-push inflation with demand expansion and full-employment promotion policies, thus avoiding waste in productive resources.18

As seen, if the distributive conflict intensification leads to a permanently higher inflation rate, but not to an accelerating inflation, income policies that soften this conflict can be a progressive alternative to austerity measures. Taking Brazil’s structural and institutional aspects into account, a possible income policy would be expanding the provision of public goods and services and lowering managed prices. This would raise real wages and prevent the negotiations from occurring only regarding nominal wages bargaining. Over time, it also would be important to avoid abrupt fluctuations on regulated goods and services’ inflation, as well as on the nominal exchange rate and, consequently, on the imported inflation. The exchange rate fluctuation management imposes limits to lowering the domestic nominal income rate, specially when the basic nominal income rate set by the Fed still finds itself in high levels and without any clear perspective of being reduced.

Considering its recent sharp drop, to recover the wages’ share in the functional income distribution will certainly require efforts in the direction presented above.19 After the unique growth of the wages share in 2023, the minimum-wage real readjustment policy that has been readopted and the lower unemployment rate represent the conditions necessary for the steady recovery of the wage share. On the other hand, even the brief reversal of the distributive trend is generating discontent among business and financial circles, already calling for an end to it. In line with the interests of these same circles, the zero-deficit fiscal policy and the recent reduction of the inflation target will certainly constitute additional obstacles to a sustained recovery of the wage share of income.