Energy Offshoots

Comments Off on Energy OffshootsPetróleos de Venezuela (PDVSA) has been integral to Nicolás Maduro’s government and the greater Chavista project. Despite the state-owned oil company controlling the largest crude oil reserves in the world, its production capabilities have fallen sharply since 2014: the country went from producing 3 million barrels of crude per day in 2013, accounting for 96 percent of the country’s exports, to producing 800,000 barrels per day today. This 70 percent drop in oil production has gravely impacted funding for state social protection programs. Hyperinflation further aggravated the situation, ushering in a wide-scale crisis. The political turmoil unleashed by the most recent election has only exacerbated tensions.

The scope of the crisis attests to the central role of oil and gas in Venezuela’s development model. Dependent on oil as its main export, the Venezuelan national economy is left vulnerable to external shocks, which have the ability to impinge on social services and employment. Chávez’s election in 1999 marked a new era of the relationship between the state and the oil industry—one of direct government and party control. But the promise of the Chávez model, premised on greater control over the financial industry combined with a broadened welfare state, had already begun to crumble as investments and production fell during the first decade of the twenty-first century.

More recently, geopolitical transformations surrounding the oil industry have constrained Venezuelan politics. The Maduro regime has faced sanctions from the US government since 2014. Five years later, the US imposed further sanctions against the PDVSA and Venezuela’s Central Bank. These moves have imperiled the PDVSA’s finances, leading the Venezuelan government to seek closer relationships with China, Russia, and Iran in order to ensure the regime’s survival. But this realignment strategy has not drastically altered Venezuela’s commodity-based development model. In short, the horizon of Maduro’s regime still hinges on the country’s oil dependency.

Development and dependency

Since the 1922 “blowout” of the Barroso II well, the oil industry has been the main axis of Venezuela’s economy and politics. The oil boom precipitated the onset of deep transformations to the structure of the republic. With the end of dictatorships and the dawn of democracy, the second half of the twentieth century was marked by rapid urbanization and modernization, which was almost exclusively funded by oil income. From the 1950s to the 1970s, economic growth was noticeable through high national growth rates and substantial improvements in the quality of life of citizens, culminating with the creation of PDVSA in 1976.

In short, the oil boom allowed for the expansion of infrastructure, public services and, for the first time, the rise of a middle class. In addition, the nationalization of the oil industry with the founding of PDVSA secured state control over rents, which incentivized high public spending, despite the country’s lack of a solid tax base. The state became the main provider of goods and services, while the private sector lagged behind. This model laid the foundation for a rent-based state that would inspire and sustain Chavismo in the years to come.

But this progress was accompanied by increased dependency, leaving the country vulnerable to the fluctuations in the international market. The cyclical rise and fall of oil prices that started in 1973 revealed the vulnerabilities of the national model. Assuming the presidency in 1994, Rafael Caldera faced a banking crisis that devastated the financial system. In response, Caldera engaged the IMF and applied the “Venezuela Agenda” to stabilize the economy. His government pried open the oil sector, allowing PDVSA to lead investments and recover its growth by 1997.

From 1989 to 1998, PDVSA positioned itself as one of the five largest oil companies in the world, with interannual growth at 7.5 percent and production reaching 3.3 million barrels per day (mbpd). From its creation up until 1999, the company had distinguished itself as a global innovator in the hydrocarbons industry.1

A decline in oil prices during the 1997–1998 Asian financial crisis forced the country to create a Macroeconomic Stabilization Fund and to privatize state companies to mitigate volatility. Despite the efforts, institutional deterioration persisted, and widespread dissatisfaction laid the groundwork for Hugo Chávez’s electoral victory in 1998.

Oil welfare

With the election of Hugo Chavez in 1999, control over oil became a key political, financial, and geopolitical tool of the state. The state intensified its control over PDVSA, whose rents were used to expand social protections. At the same time, the Chávez regime pushed the twentieth-century model of oil statism to its limits. The result was the consolidation of national dependence on oil rents and exchange-rate controls.2

Two laws supported the changes in the relationship between the state and PDVSA: the Constitution of the Bolivarian Republic of Venezuela (CRBV), drafted in 1999, and the Organic Hydrocarbons Law of 2001. The Constitution marked the beginning of what Chavismo called the “Fifth Republic,” emphasizing the principle of sovereignty over subsoil resources. In practice, this meant that the state owned hydrocarbons reserves. While this regulation had been stipulated in prior laws, the new constitution stressed the role of the state in order to prevent the exclusion of the executive branch from industry decisions.

The legal changes also transformed the relationship between PDVSA and the welfare state. In 2003, PDVSA started to finance welfare missions worth $549 million each year. Two years later, the National Development Fund (FONDEN)—financed by oil holdings—was created. Now burdened with greater financial commitments, PDVSA needs to meet increasing welfare costs.

The arrival of Nicolas Maduro to the presidency in 2013 did not bring significant change. In fact, in July of 2014, oil prices fell by 76 percent, speeding the fall in oil production and investment. Consequently, social protection programs saw significant cuts, from around $13 billion in 2013 to $5.3 billion in 2014.

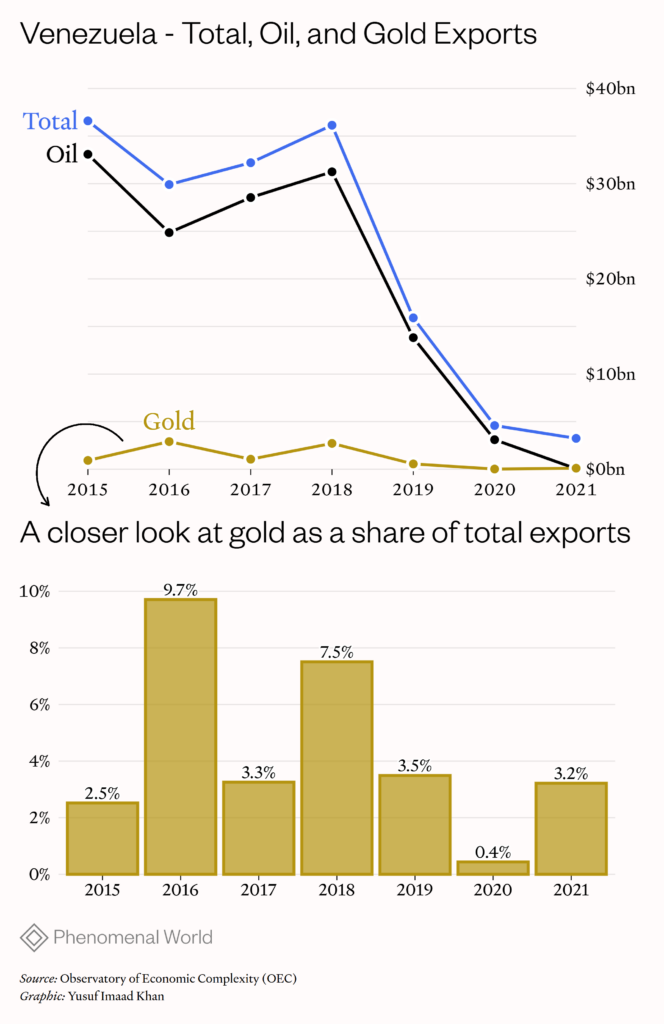

The plummeting of prices aggravated the social crisis, where dependency on oil income led to the collapse of the welfare state. This resulted in higher poverty rates, a dearth of goods and services, and the largest population exodus the region has experienced in modern history. During Maduro’s first term, crude exports accounted for up to 90 percent of total exports, but incomes dropped dramatically.3 Production in 2019 was only one-seventh of what it had been in 1976.

The sanctions effect

The economic sanctions against Maduro’s regime further deteriorated PDVSA’s production. The goal was to modify the state management of the sector by constricting oil rents. Until 2017, the United States was a top destination for Venezuelan oil. Even as late as 2015, Venezuela was the third most important crude exporter to the United States, following Canada and Saudi Arabia. The result of the sanctions was to push Venezuela to realign with other geopolitical actors.

Overall, US sanctions drastically reduced the regime’s ability to operate in global markets, slashed its oil incomes, and consequently worsened the internal crisis. The possible reactivation or intensification of sanctions in the near future could hamper any attempt to revitalize the national energy sector—which is crucial to a country whose economy is still struggling to recover from years of poor management and international isolation.

The 2017 sanctions affected the oil sector directly. PDVSA was banned from accessing US financial markets and its abilities to refinance its debts and sell crude were restricted. In January of 2019, in parallel to Juan Guaidó’s self-proclamation as interim president, the United States froze some $7 billion in PDVSA assets, while blocking more than $11 billion in projected income.

To secure additional income, Maduro resorted to exploiting unconventional resources and selling strategic assets. Two new projects, the exploitation of the Orinoco Mining Arc and the introduction of the “petro,” a cryptocurrency backed by oil reserves, both resulted in failure. They were incapable of attracting investor confidence or offering a sustainable solution to the country’s liquidity crisis.4 The “petro” failed because of generalized distrust in the currency, in addition to the restrictions it faced after its launch.5 Meanwhile, the exploitation of the Orinoco Mining Arc mainly benefited the upper echelons of the government and military, in addition to foreign allies, such as Colombian rebel groups like the National Liberation Army (ELN) and the Revolutionary Armed Forces of Colombia (FARC),6 as well as the Russian private military company known as the Wagner Group.7

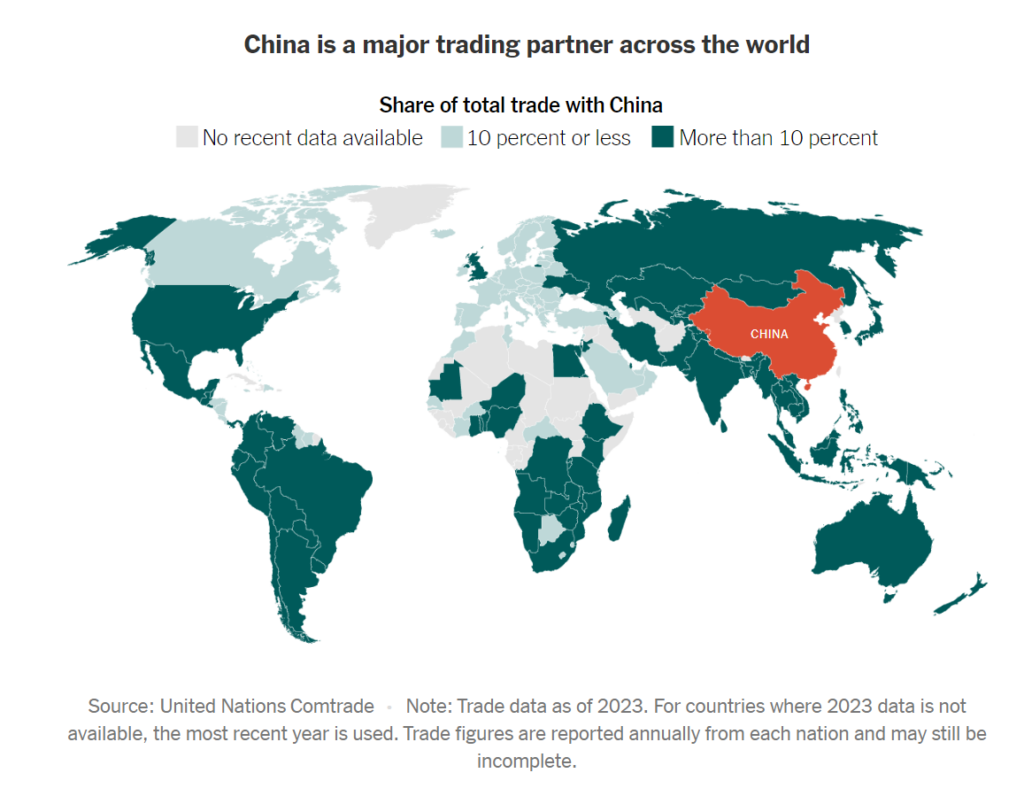

In 2021, exports dropped to a historic low, amounting to $3.2 billion, of which gold exports made up $104 million. Oil was removed from the record of legal exports. Instead, it was sold in clandestine markets via triangulations with Russian tanks that would cross the open sea to send crude to India, then reexporting it to other parts of Asia, especially China, at a heavily discounted rate. This operation, which was not accounted for in official figures, was marred by Russia’s invasion of Ukraine and by sanctions on Russian oil, which also impacted Venezuela.

Geopolitical realignments

In a context of international isolation and economic collapse, Maduro had to appeal to strategic alliances once forged by Chávez, leaning into a geopolitical bloc that has allowed Venezuela to partially evade sanctions, maintain a minimum oil income and, above all, secure Chavismo’s survival amid a hostile international environment. In the quest for new partners, Maduro’s bargaining chip continues to be, above all, the national oil sector.

Under Chávez, the government deployed the state-owned oil company’s resources to bolster ties with certain countries in Latin America, the Caribbean, Eurasia, and Africa. For example, the Petrocaribe initiative sought to coordinate the energy policies of Central America and the Caribbean. Venezuela provided the region with oil at low interest rates, with payment plans of up to twenty-five years. In exchange, Venezuela would receive commodities and agricultural products. But the agreement was questioned for its lack of transparency and confidence in its transactions. Most member countries canceled large chunks of their debt by bartering products whose value was hard to measure.8

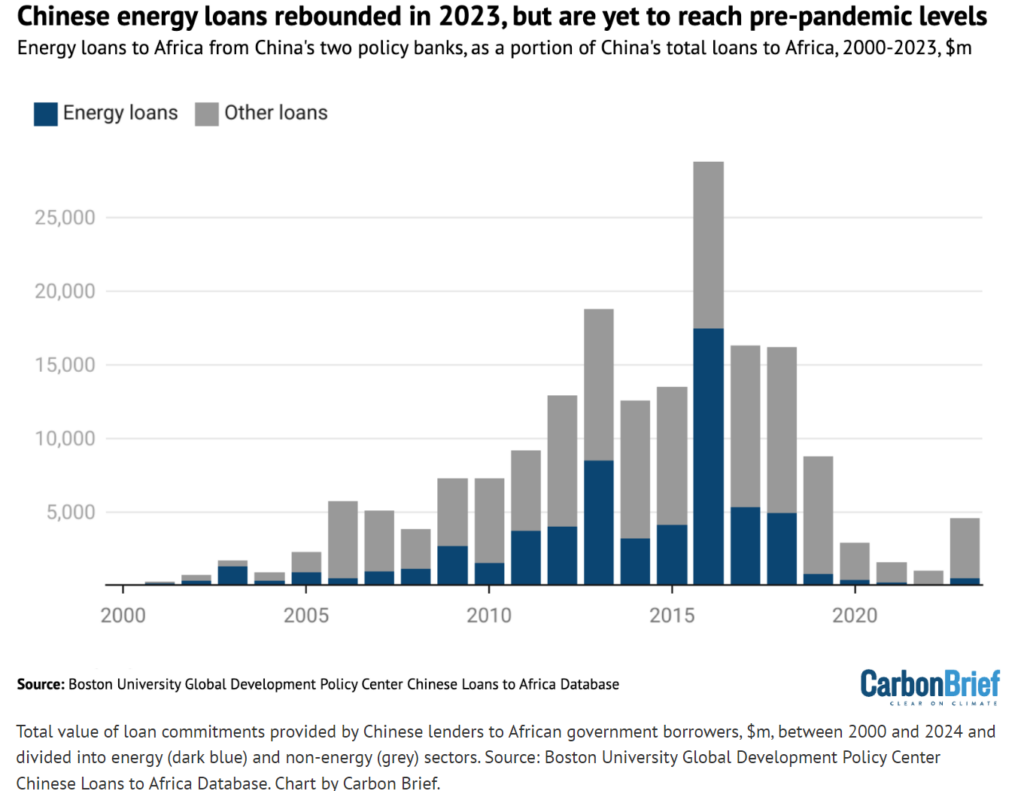

China has also been a key partner to Venezuela. The pillar of the China-Venezuela relationship is an agreement to exchange funds for oil, first initiated by Chávez. Venezuela began to receive loans that were mainly backed by oil-debt agreements in 2007—the China-Venezuela Joint Fund is one key example. Under Maduro’s tenure, and Xi’s regime, the agreements remain but they hold less weight given the changes in the sector. China has extended approximately $67 billion in loans to Venezuela, which have largely been paid by crude shipments. With the drop of oil production during the 2010s, the agreement has become increasingly unsustainable. The volume of oil sent to China has plummeted, forcing Caracas to restructure its debt on various occasions. Despite these challenges, Beijing has continued to support Maduro—no longer with loans, but with various infrastructure and technology investments, as well as military-equipment sales, though in a more cautious and conditional way than before.9

In 2023, China and Venezuela signed an agreement to mutually promote and protect investments. Three years prior, in 2020, the state-owned China Aerospace Science and Industry Corporation (CASIC) took up the transportation of Venezuelan crude as a way of compensating for some of Venezuela’s debt to China. But the relationship with China is not limited to the mere transfer of resources—there is a broader strategy at play. By participating in infrastructure, mining, and telecommunications projects, China has secured a significant presence in key sectors of the Venezuelan economy. This is the case in the field of telecommunications, for example, with support from companies like Huawei and ZTE, as well as in the military plane.

On the other hand, Russia has been a key ally in the survival of the Maduro regime, not only supporting its energy sector but also providing military and diplomatic assistance. The relationship between Moscow and Caracas has intensified in response to pressures from the United States and European Union. For Russia, Venezuela represents an opportunity to defy US influence in its own hemisphere.

The Russian state-oil company Rosneft played a key role in the commercialization of Venezuelan crude oil, especially after the imposition of US sanctions. In 2020, Rosneft sold its shares in Venezuela to the security company RN-Okhrana-Ryazan, which is controlled by Roszarubezhneft, an entity created by the Russian government. This transaction allowed Russia to continue to exploit Venezuelan oilfields through the National Oil Consortium (CPN). Rosneft affiliates, like Rosneft Trading and TNK Trading International, were sanctioned for facilitating the trade of Venezuelan crude, a clear attempt by the US to prevent both governments from reaping benefits from their transactions.

Through a complex network of companies and transactions, Rosneft helped Maduro evade sanctions, while also keeping up a constant flow of crude exports. The main recipients were Asian markets, which accounted for 64 percent of total exports in 2023, before the Biden administration temporarily eased sanctions.

Perhaps one of the most surprising and least predictable alliances has been between Venezuela and Iran. With its refining infrastructure in ruins and under the pressure of sanctions, Maduro turned to Iran, a country also facing a severe regime of international sanctions, to help with its fuel supply. Defying US sanctions, Iran sent several fuel shipments to Venezuela, which inaugurated a new phase of cooperation between two regimes isolated by the West. In exchange, Venezuela granted Iran access to gold and other strategic resources.

But the cooperation between Caracas and Tehran goes beyond shipments. Iran has provided technical assistance for the reactivation of Venezuelan refineries, sending spare parts and materials for fuel production in an effort to temper the collapse of Venezuela’s refinery industry. The relationships with both Russia and Iran also have a significant symbolic charge. By presenting itself as an ally of Eurasian powers in defiance of US hegemony, Maduro guarantees an image of resistance on the international stage that aligns his regime with the multipolar narrative that Chávez promoted.

Through this process of political realignments, driven by sanctions themselves, Venezuela fully embraced a circuit of evasion by selling oil on unregulated fleets, with the transactions conducted in the Chinese currency renminbi. This scheme has allowed Venezuela to keep exporting crude despite restrictions, by relying on alternative financial systems beyond Western control that undermine the effectiveness of sanctions.10

Uncertain horizons

In 2023, the Biden administration temporarily lifted certain sanctions in order to incentivize free elections. After long conversations and at least six gatherings in Doha, the Barbados Agreement was reached between Maduro’s government and Venezuela’s opposition party. The agreement involved a series of political commitments and the granting of a license to produce, extract, sell, and export oil from Venezuela. However, sanctions were reinstated mid-2024 in response to the Venezuelan Supreme Court ratifying an electoral blockage against the opposition campaign of María Corina Machado.

The threat of reimposing sanctions looms over the Chavista leadership. Ongoing negotiations could reach a critical turning point on January 10, 2025 when Nicolás Maduro is set to assume his next term as president. Donald Trump’s reelection in the United States also adds to the uncertainty, as he could choose to reinstate sanctions and intensify pressure from Washington.

Parallel to these political developments, the US Department of the Treasury renewed General License 41, allowing Chevron to continue limited operations in Venezuela up until April of 2025, with certain restrictions. This suggests that a dual strategy is emanating from Washington: some economic channels are being kept open for US companies, but the US government is maintaining its ability to exercise political pressure against the Venezuelan regime. This dynamic will undoubtedly influence political decisions in Caracas.

In light of the geopolitical situation, the Venezuelan regime faces the need to urgently revitalize its energy sector amid economic collapse. The exploration of new wells along the Orinoco Oil Belt—which houses the greatest heavy crude reserves in the world and has been historically underexploited—has become key to this strategic attempt to reverse plummeting production. Collaborating with Chevron, as authorized by the US Office of Foreign Assets Control (OFAC) in 2022, has allowed the American company to resume plans to drill up to thirty new wells along the Belt by 2025, and increase production alongside PDVSA by up to 35 percent to reach 250,000 barrels per day. Yet the sanctions still limit Chevron, which cannot expand operations to new fields or distribute dividends to PDVSA. This restriction secures Washington’s control over the regime even as PDVSA seeks to sustain its energy sector.

Furthermore, the exporting of natural gas from Venezuela to Colombia and the oil discovery in Guyana have similarly become crucial strategies. The exports of natural gas to Colombia are not only economically significant, but they also carry political weight, as Colombia has offered to mediate the regime’s crisis of legitimacy while Venezuela, in turn, has served as guarantor for Colombian president Gustavo Petro’s “Total Peace” dialogues. However, the dual role as mediators and guarantors strains the partnerships between the countries, putting the export project under intense political pressure, both internally and externally. In addition, Venezuela’s gas capabilities and the state of its gas pipeline have cast doubts around the viability of the project.11

Meanwhile, Guyana’s recent oil discovery and growing oil production has intensified a long-winded territorial dispute between the two countries, specifically around the resource-rich region of Esequibo and its exclusive economic zone for offshore oilfields. While Guyana has moved forward in the exploitation of these oilfields with the backing of multinational corporations like ExxonMobil and Chevron, Venezuela has escalated its claims on the region. This is yet another source of regional instability and geopolitical risk.

For now, Maduro has continued to bet on oil. In a hostile international environment, the regime has viewed oil and PDVSA as means for survival, using these assets to maintain alliances and explore new markets that might allow it to generate wealth and sustain itself in the face of immense external pressure.