Polycrisis 2025

Comments Off on Polycrisis 2025The United States will be a source of chaos and volatility for the next several years. The first month of 2025 has set the scene. Events so far have included imperial gangsterism against both a poor Latin American country (Colombia) and a rich northern European one (Denmark); a long-overdue ceasefire ending a genocidal military campaign (Gaza); the most expensive natural disaster in US history with climate-fuelled wildfires destroying homes (California); a trillion dollar sell off in the AI bubble in reaction to a Chinese firm’s innovation from behind the chips blockade; and the outbreak of a virus (H5N1) that has killed hundreds of millions of US poultry, sending egg prices soaring and raising concerns among scientists of another pandemic. OK, doomer.

It is hard to predict where exactly the administration’s stated goals of deporting immigrants, solidifying dollar strength, restoring trade surpluses, and maintaining low inflation will land—or how they may cause friction with the underlying agenda of authoritarian kleptocracy. Searching for a clearly defined, stably coherent ideology of the Trump administration may be a fool’s errand. In any case, it’s not as though the US has been known for providing stable, benevolent, or far-sighted hegemony; the rest of the world has been adjusting to an increasingly erratic US for many years.

But if a coherent worldview is out of reach, there are still patterns to be discerned in the order being formed around Trump, and the ways in which the rest of the world is bound to respond.

When we launched The Polycrisis two years ago, we set out to examine the intersecting crises in the economy, energy system, commodities markets, geopolitics, and climate. Our aim was to “break intellectual and political silos to give a fuller picture of what’s going on.” The overlapping crises of ecology, economics, and empire, have continued to interact and metastasize. This year, as much as we pay attention to Trump’s chaos machine, we will focus more on the rest of the world’s efforts to organize itself around and without the United States. Whether they will be successful is anyone’s guess. To paraphrase Adam Smith, there is a great deal of ruin in the world order. Here are the themes and developments that we are watching.

Diplomacy and world-building

From the point of view of US policymakers, American diplomatic leadership stabilizes the world. Without it, the “jungle grows back,” as Robert Kagan put it, and the international order descends into the chaos of “might makes right.”

For the rest of the world, the US’s might has been something to strategically ally with or risk being crushed by, but rarely benign. And the liberal international order that the US has helmed is increasingly unstable—threatened by the economic and geopolitical ascension of China, the deindustrialization of the US domestic economy, the abuse of the UN and the international legal order most recently by the Biden administration’s support for genocide in Gaza, and the Trump-Biden move to protectionism and away from multilateral rules-based fora like the WTO, even as the rest of the world deepens its trade relationships.

The G20 meeting in Rio de Janeiro last November, soon after Trump’s election, may provide some sign of what’s to come. There, China, Europe, Brazil, India, and South Africa insisted they would uphold the multilateralism that the Trump administration has promised to abandon.

For many countries, that will mean continuing to build connections with China, even if warily. Most Asian countries are economically entwined with China but few are wholehearted geopolitical allies. Several African nations have been keenly receiving Chinese financing since the late 2000s—but that lending has shrunk dramatically since 2019 leading heavily indebted African countries to become more strategic in dealings with their creditors. Angola, for example, has managed to win space in servicing its considerable debt to China, and is also welcoming clean energy finance from Europe.

Going forward, China will continue to seek to shore up its role as an alternative hegemon. The day after Trump signed executive orders pulling the US out of the World Health Organization and the Paris climate agreement, China vowed to strengthen both organizations. At the G20, President Xi Jinping turned on the charm offensive, announcing an eight-point agenda to support developing countries. Throughout meetings with world leaders, Xi solicited support for free trade, with an eye on China’s flagging economic growth. Participants from other countries noted that Chinese representatives expanded beyond traditional diplomatic practice of focusing only on China’s “most essential interests.”

As the US recedes from the multilateral stage, other governments are stepping in. Last November, Dani Rodrik pointed to the middle powers helping to bring into being a multipolar world: “With advanced economies increasingly focused inward, middle powers like India, Indonesia, Brazil, South Africa, Turkey, and Nigeria have become the natural champions of global public goods.”

The Trump administration is definitively not in the business of delivering such goods. After just a few days in power, the US International Development Finance Corporation (DFC) has been required to stop deploying clean energy finance, and instead fulfil Trump’s expansionist ambitions around Panama and Greenland. Development aid, in the form of USAID spending—on children’s education, clean water, lead remediation, climate—has been frozen until it can be checked for alignment with the objectives of “America First.” Where some are looking to China for signs of hope, as a source of a green Marshall Plan, there is little sign of a boost to shrinking Belt and Road lending, let alone a big play to aid financing of imported Chinese clean tech, or transfer of technological know-how.

Europe

How effective will Europe be in an America First world at protecting its own interests and preserving multilateralism?

As Trump comes to power, the EU faces significant challenges. The euro area is projected to stagnate and Germany’s February elections look set to bolster the far right—domestically and beyond. In the aftermath of Russia’s invasion of Ukraine, energy vulnerabilities have been exposed. The inflationary surge following the pandemic prompted the European Central Bank to implement high interest rates, curbing investment without addressing underlying inflation causes. Such policy recalls previously self-inflicted wounds, like the austerity measures implemented following the financial crisis that led to Europe becoming poorer and weaker. For all the reports and grand plans, it’s not clear what the bloc will do to change its path.

For now, Europe is distracted and paralysed: harangued by Trump to increase its defense spending to 5 percent of GDP; lurching through an impressively quick but painful energy transition; and beset by far-right parties that will oppose any of the integration that will be necessary for the bloc’s revival. Stung by the US, the continent is looking South and East. Last week at Davos, Ursula von der Leyen spoke positively of recently negotiated trade deals with Switzerland, the South American bloc Mercosur, and Mexico—although these still require complex and difficult European parliamentary approval. Most importantly, she encouraged constructive engagement with China so as “to find solutions in our mutual interest.” She declared the first visit she took in the new Commission would be to India and that the work of building local clean tech value chains in Africa would continue.

Tech transfers

However the next several years play out, technology transfers will be key. As we wrote in 2023, China’s successful pursuit of expertise from batteries to semiconductors to AI has been enormously significant. It has upended the status quo of “G7 countries holding the tech required by the rest of the world.” Chinese material goods and know-how are now sought after not only by African and Latin American countries, but also by the US and the EU—which last month inserted a requirement for tech transfer from Chinese recipients of battery manufacturing grants.

This is what Adam Tooze recently called the “Second China shock”; if the first shock saw China being integrated into advanced tech supply chains, the second sees those same countries begging to be let into theirs. If the EU uses its considerable market power to negotiate tech transfers of intellectual property from China, making it available to other, less powerful countries, that would be a win for climate; and thus ultimately for everyone.

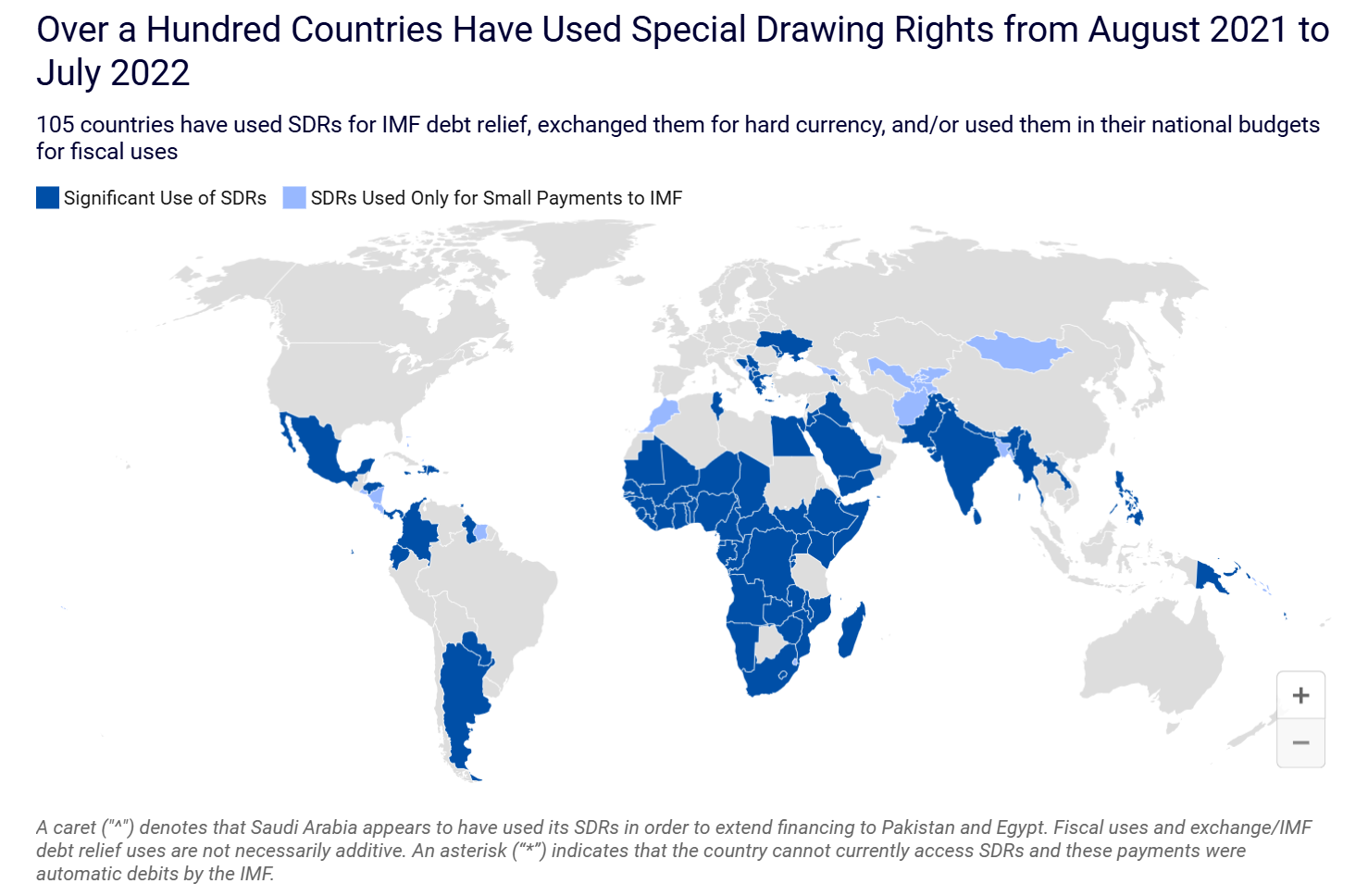

Finance for realists

The Biden administration acknowledged the urgency of mobilizing financial resources for global climate and development needs, centering its strategy on private sector involvement, which predictably failed to materialize. Now, with the Trump administration in place, any sense of commitment to addressing climate change among big US banks like Morgan Stanley and Goldman Sachs has dissolved. (The banks’ membership in a finance industry climate alliance, GFANZ, was used to make hyperbolic promises of $130 trillion waiting to lend to developing economies, which also failed to materialize.) If there is a silver lining in all this, it’s the casting off of the illusion that private finance would ever prioritize climate goals over profit; in turn, this might mean wider opportunity to refocus on fundamental financial reforms. These include the high cost of capital for global South countries (which Barbados championed, and South Africa has placed high up on its G20 presidency agenda) and the unsustainable debts owed to private creditors, which means governments tend to divert significant resources from essential investments toward debt servicing.

The Vatican has designated 2025 as a Jubilee year, and Pope Francis has urged Northern creditors to consider forgiving debts, and aligned with broader efforts to address the global debt architecture. Halfway through this Jubilee year, the Fourth Financing for Development Conference (FfD4) will meet, led by the Group of 77 and facilitated by the UN. The conference’s zero draft includes proposals for addressing the systemic inequities in the global financial system that constrain development in the global South.

The venue could make headway on the debt system and the barriers to climate finance, if the focus shifts away from relying on private finance or expecting leadership from the US government—neither of which has proven viable.

Extraction

Even as the world moves towards a more manufactured and less extractive energy system, things that are pumped or dug out of the ground remain central to geopolitics. In the wealthy world, fear of Chinese dominance and greed for new resources and markets continue to spur the scramble, as the latest grab for Greenland makes clear.

These minerals are an evolving avenue of North-South trade and, potentially, industrial cooperation. Every developing country with transition minerals wants to emulate Indonesia, which used an export ban on unrefined nickel to leverage its large reserves for technology transfer with Chinese and Korean onshoring processing plants. Latin American countries are hoping to become economically prosperous by leveraging resources like copper (Mexico, Chile), lithium (Chile), graphite, and manganese (Brazil) to participate in battery and green supply chains.

A powerful buyers’ club—involving the US, Australia, South Korea, Japan, and the EU—may be emerging in the form of the Minerals Security Partnership, but so far there is no critical minerals version of OPEC that would help poorer, less powerful countries with mineral reserves to advance their own interests as sellers.

South Africa plans to use its G20 presidency this year to harness critical minerals for African development, with Cyril Ramaphosa describing “a grand bargain that promotes value addition to critical minerals close to the source of extraction.” It reflects a widening recognition that resource-rich developing countries need tech transfers to move up the value chain. Such transfers are rare. A Columbia University study which examined dozens of international projects in the pipeline across Latin America, Asia and Africa found that instances of tech transfer were scarce, even though it is the main source of innovation for value-adding in the critical minerals sector. It recommended that the WTO adopt the proposals of the African Group of 44 countries, and that developing country governments make tech transfer a condition of investments from foreign companies.

Oil

In 2025, oil demand looks more likely than ever to peak well before 2030, while supply climbs up, up, up. Saudi Arabia is still withholding in the region of three million barrels per day of production. Meanwhile, the US is producing record amounts, and China, which relies on imports, is curtailing its use—leading to what a Morgan Stanley analyst calls “a different oil market in the future than it has been in the past.”

Gulf kingdoms are trying to diversify their economies by deploying footloose petrodollars to acquire new industries. They are also increasingly focused on development finance, especially carbon offset deals covering vast tracts of land in African countries—a fifth of Zimbabwe, 10 percent of Liberia, 10 percent of Zambia, and 8 percent of Tanzania—while rapidly expanding their domestic renewable power capacity to save their remaining hydrocarbon deposits for much-needed export dollars. Several low-income countries with fossil resources, such as Namibia, Senegal, and perhaps Uruguay, are hoping to develop them in time to exploit a declining market, while others such as Colombia and Ecuador are exploring ways to transition to new industries before the price decline.

LNG markets are perhaps as significant as trade in oil. The versatility of LNG, its lingering (incorrect) reputation for being “cleaner” than coal, and relative ease of transport make it the marginal fossil fuel of choice. Demand is volatile, projections across most time horizons are fiercely contested, and price spikes are painful for importing countries—giving it big geopolitical ramifications, as well as climate ones.

American LNG exports, the largest in the world, are a bullying tool for Trump against the EU—buy our gas or we won’t protect you!—and a convenient addition to the US “energy dominance” narrative. LNG is a source of potential tension between richer importers and poorer ones, as when European countries outbid Pakistan and Bangladesh for shipments in 2022. The relative speed of building facilities raises the risk of sovereign asset stranding (will Germany need all its new LNG import terminals?). As well as contributing to climate impacts, LNG is also a conduit for them to the wider world: when China’s hydropower dams are affected by drought, for example, world LNG prices rise (as seen in the lead-up to 2022).

Domestic themes

Domestic politics drive international political instability. The faltering and fracturing of formal multilateralism will underscore the importance of national policies and political coalitions—just as it did during the last Paris Agreement exit by the US. We see a couple of particularly important themes playing out across domestic contexts this coming year.

How Europe addresses media and tech barons. In stark contrast to the mood of Trump I, US tech giants, with billionaires at the helm and staggering stock market valuations, have all either gone full MAGA or bent the knee. The battle over public opinion is now being waged largely through the platforms they control.

Last year, Brazil demonstrated that states can in fact take on seemingly all-powerful social media platforms, by demanding that X adhere to its domestic anti-disinformation laws. The European Commission is investigating whether X has breached its Digital Services Act, and this January sought to review the platform’s recommendation algorithms. It’s unlikely to preempt any disinformation perpetrated in the lead-up to Germany’s late-February elections, but Brussels has enough institutional power to take on the platforms’ increasingly open attacks on democracy, and represents a large enough user base to hurt the social media oligarchs.

Anti-migrant politics. A consistently growing theme in many western countries is the vilification of immigrants, waged increasingly aggressively by conservative political parties of all stripes. It is not just a violent agenda, but also a strategy to co-opt the centre right and centre left by preying on fears.

Fuelling and exploiting anti-immigration sentiment is a playbook that has been repeated with great success by the far right in numerous rich countries. Look at European leaders getting close to Meloni, and Germany’s CDU collaborating with the AfD. Having picked up on the narrative momentum of globalization eroding (“stealing”) manufacturing employment, the immigrant scapegoat can be blamed for inflation, high housing costs, and even climate impacts. The challenge is whether a successful politics and coalition can be forged that addresses exploitable woes—through better housing, energy, monetary, fiscal, and climate policies—and pulls the blame away from migrants.

Climate

This year, like all recent years, climate-driven disasters will affect billions of lives. What does the America First, fragmented, multipolar world mean for climate action? And especially for climate action in the context of international climate diplomacy which—like the EU—came of age at the high noon of neoliberal globalization?

The return of COP to Brazil will highlight land use conflicts: forestry, renewables, food. Fights over land are fundamental to human society, with landowners underpinning resistance to change in the mid-transition to new energy systems. The relatively smooth global decarbonization pathways spat out by models provide little preparation for the reality of land contestation in one community after another.

The retreat of private sector insurers from climate-vulnerable areas will push more and more pressure onto the state. People in countries with the fiscal means and the willingness to use it will have a safety net. The countries that don’t have the means, but have high exposure to climate impacts, have been escorted into arrangements like parametric insurance. After several big disasters that failed to pay out, will many of them want to continue?

Greenhouse gas emissions can’t be cut dramatically without big changes in our global trade and debt systems. In 2023, COP28 recognised the need for concessional and grant-based finance and was the setting for commitments by multilateral banks to extend catastrophe clauses in their loans. At the 2024 COP, just held in Azerbaijan, trade-related climate measures were given a formal space for the first time.

The challenging context may induce siloed policy responses, which in turn gives oxygen to the right, keen to point the finger at targets like immigrants in order to cohere their own narratives without having to consider the nature of the intersecting crises in which we all live.

Climate change cannot be addressed as a siloed policy area. Questions of mining and energy, finance and development, migration and tech, cannot be separated out from the vast changes occurring in the world’s climate. No crisis is an island. Each of these areas affects and is affected by the other, and addressing one will require addressing all.