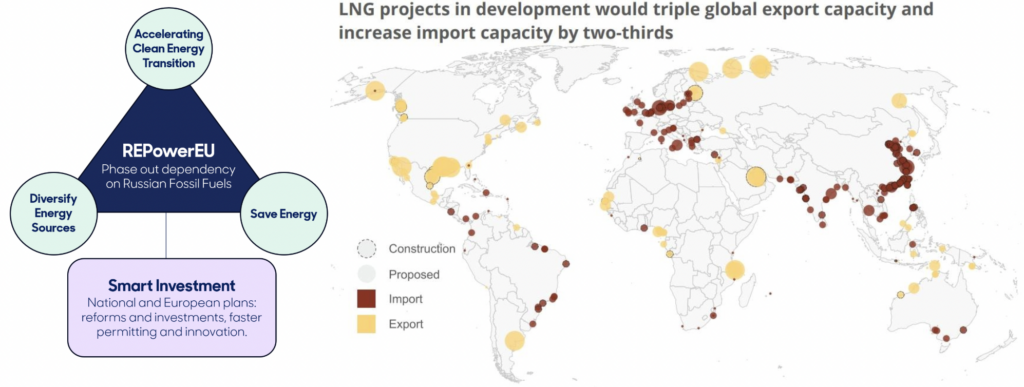

When Russia invaded Ukraine in February 2022, European, and especially German, industry was left in the lurch. Much of the 150 billion cubic meters of natural gas piped from Russia each year had to be quickly replaced with energy from elsewhere. All the stops were pulled out: nuclear and coal power plants were fired back up, solar and wind project approvals soared, and there was a rapid and massive buildout of LNG import terminals. Under the sign of the REPowerEU plan to phase out the continent’s reliance on Russian gas, almost 80 billion cubic metres of LNG import terminal capacity was built in Europe over the last three years. Another 80 billion is expected by 2030.

The surge in Europe’s LNG appetite came at the direct expense of poorer countries like Pakistan and Bangladesh, whose contracted LNG shipments in 2022 were diverted to European energy companies willing to pay a much higher price. In hindsight, the pace of this build-out looks frantic: even as capacity is increasing, several projects have been cancelled and the utilization rate of the new terminals is well below half. Analysts estimate that the scale of overinvestment of Europe’s LNG buildout is equal to the combined annual gas demand of Germany, France, and Poland.

In 2019, announcing increased LNG export authorizations from Freeport LNG in Texas, a Trump Department of Energy official declared that the government was proud to export “molecules of US freedom” to the world. Six years later, from Russia’s war in Ukraine to Gulf-EU trade disrupted by the Houthis to the deployment of LNG sales as an American trade war bargaining chip, we are awash in fossil fueled energy security crisis stories. At the center of it all is the hydra-headed global market for liquified natural gas.

The rise of LNG

Worldwide use of liquefied natural gas has more than doubled since 2009. This boom has occurred with the help a concerted and effective campaign from its industry boosters. Gas is, to be sure, nimble, flexible, and versatile. Its use can mean a marked reduction in air pollution from coal-fired power and indoor wood burning that together kill millions of people each year. It can be used for electricity generation and for industrial power. Chilled to -162 degrees centigrade, it becomes a dense liquid that is moved around the world in specialized tankers—and then warmed up into a gas to be burnt for fuel.

Methane gas has long been spoken of as a “bridge fuel.” Cleaner than coal, it was touted as an easy interim step on the way to clean energy, rather than an end in itself. This narrative was pioneered in the US by the gas industry in the 1980s, and amplified by big environmental groups and Democratic Party officials in the late 2000s and early 2010s as the fracking boom made gas cheaper. Research and monitoring since then has shown the climate advantage of gas over coal is nowhere near as wide as thought. The natural gas industry has recently declared that it’s no longer a “bridge fuel,” but rather a permanent source of “baseload” power—confirming fears that expanding gas infrastructure is likely to simply lock in more planet-boiling fossil-fuel combustion.

Oil has been the most important energy commodity of the modern era, and probably of all time. The control of reserves and transport routes; the cost of extracting, moving, and refining it; and the (in)elasticity of demand for oil have all played an outsize role in global politics for over a century. Coal’s trajectory has been different. Abundant and relatively easy to transport to industrial centers, it was the first widely used fossil fuel. While it did become a mass commodity like oil, it is for the most part consumed domestically in the country where it is extracted; less than a sixth of coal is traded on the international market. And at a value of less than a tenth of the trillion dollar plus oil market, it is far less central to the global economy.

A complex oil shipping industry was well established before the Second World War but it took until the mid 1960s for the LNG trade to kick off, beginning with exports to the UK from a newly-discovered Algerian gas field. The cost of specialized equipment to freeze, ship, and reliquify LNG into burnable gas originally limited its appeal against coal or gas pipelines. Cheaper Chinese and Korean equipment and technological advances in the 2000s brought costs down, although they continued to fluctuate dramatically in typical commodities infrastructure cycles, where equipment and skilled labor squeezes can quickly become bottlenecks.

Floating LNG terminals, pioneered in the early 2010s, made it easier and quicker to turn gas from undersea fields into transportable liquid. They also facilitated import and storage. When Germany sought to urgently cut its reliance on Russian gas in 2022, then Chancellor Scholz boasted that the new floating terminals—at the Wilhelmshaven, Brunsbüttel, and Lubmin ports—were built in record time; the first took less than ten months. Incoming Chancellor Friedrich Merz, has since vowed “to build fifty gas-fired power plants in Germany as quickly as possible, which will be connected to the grid immediately.” (Germany continues to import Russian LNG on shadow fleets.)

With oil now undeniably past its growth phase, the LNG market—now worth about a quarter of a trillion dollars a year—has the aura of a new geopolitical currency. In early 2025, it briefly looked as though committing to buying American LNG might be a way to appease the Trump administration—but tentative overtures from the European Commission, India, and Japan have faded since it became clear in February that American international relations is as erratic and obstreperous as it is transactional.

LNG’s rapid rise has prompted analogies with the trajectory of oil, but while there are some similarities—it’s become increasingly critical to energy systems and geopolitics—there are at least as many differences. Although the proliferation of LNG has made natural gas globally tradable and fungible, for entire countries to invest in the infrastructure required to use it (and the opportunity cost, in terms of neglecting other options), requires the willingness and ability to ride out inevitable volatility—ranging from investment cycles to wars to shipping interruptions. If coal and oil were the only real alternatives to gas, such bumps in the road might be a reasonable price to pay for building dependence on it.

But LNG’s emergence has coincided with the rise of renewable energy and storage, a convergence that fundamentally changes what the scholar Liz Thurborn has called energy statecraft. Solar power in particular is becoming cheap enough that firming the supply with batteries (which are also becoming cheaper) is increasingly attractive on price alone; and more so for reducing dependence on imported commodities like gas. This means that LNG’s pathway to an oil-like role, or even to industry projections of continued growth through the 2040s, is far from assured.

Japan’s energy statecraft

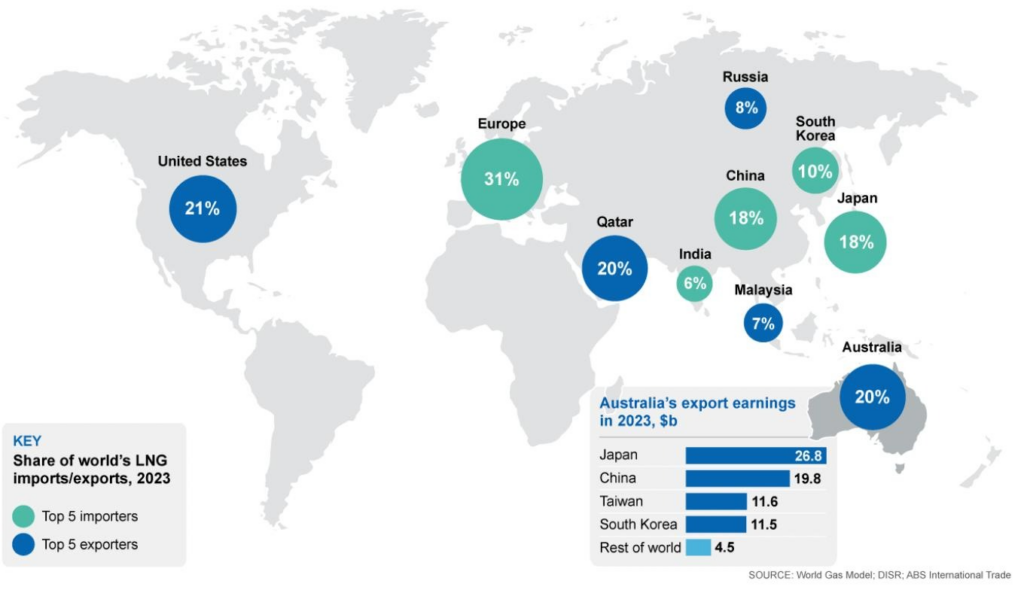

Australia, the US, and Qatar are the world’s greatest LNG producers and exporters. Energy-poor Japan, though, is something of a whale in the LNG industry—bringing in $14 billion in profits in 2023. Lacking gas resources itself, it is the home of the most profitable gas turbine firms and the biggest trading firms. It owns more LNG ships than any other country, and its companies have invested in every stage of the LNG industry from extraction to liquefaction to regasification to gas-fired power turbines. Japanese companies are major investors in foreign gas fields as well as LNG export and import terminals all over the world, from the US and Australia to Southeast Asia. Public finance institutions in Japan invested $56 billion in foreign gas in the decade before 2023. Australia, for example, which produces 20 percent of the world’s LNG, sells the vast majority of its supply to Japan, where more than half of it is then sold on to other countries. (Having failed to allocate adequate LNG for its own domestic use, however, Australia’s populous Southeast now faces the embarrassing prospect of having to import its own gas back from Japan—purchased at market rates.)

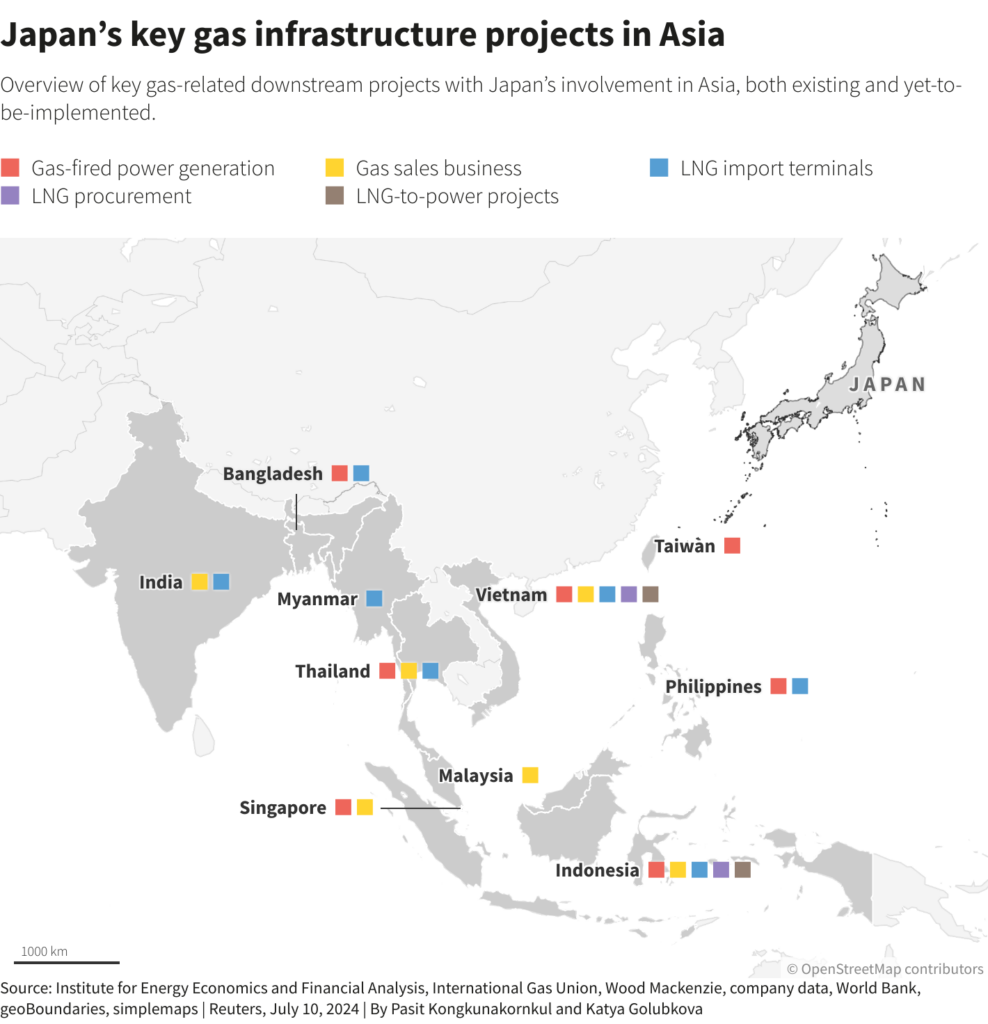

Japan’s state-owned Organization for Minerals and Energy Security “now hosts regular retreats for government officials from emerging economies,” reports Bloomberg. “The itinerary features a crash-course in the fundamentals of LNG, plus some sightseeing in Kyoto.” Big Japanese corporations’ natural gas profits match those the country’s mighty consumer electronics sector. By diversifying suppliers, investing upstream, and facilitating terminals, it has helped drive the overall expansion of LNG.

Market dynamics

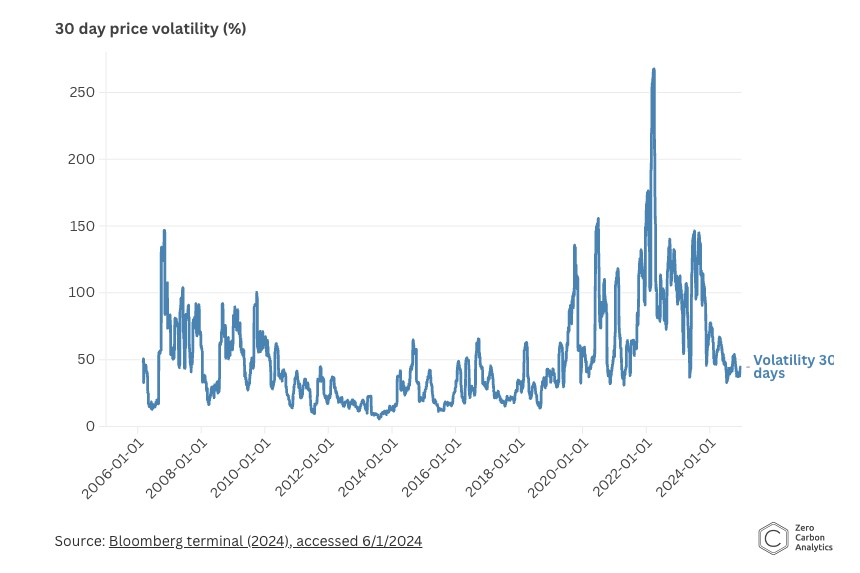

As the market for LNG has boomed, the ways that it is bought and sold have radically changed. Multi-decade contracts from buyers were once the norm. These commitments helped to finance the expense of getting gas out of the ground and building big facilities to freeze it, as well as ships to carry it. More than four-fifths of LNG shipments in 2009 were under such long-term contracts; by 2021 it was less than two-thirds and falling. Financial intermediaries or “portfolio players” have grown, and they are increasingly eschewing contracted volumes of LNG in favor of the spot market; about 50 percent of their obligations are “open” rather than covered by a sale contract. That increases the flexibility of LNG for buyers, but also introduces more risks such as price spikes when disasters, wars, and shipping disruptions happen.

LNG produced by the US is mostly “flexible” in terms of where it is delivered. This means it can leave sellers without buyers. Qatar is planning to almost double its export capacity by 2030 and is building out its production infrastructure with very few guaranteed, contracted sales. The strategic bet apparently rests on the likelihood that volumes from other exporters will decline (Australia) or face varying degrees of uncertainty (US, Mozambique)—but that demand will remain strong, especially from East Asian countries other than Japan, whose domestic consumption is falling. When the Houthis determinedly blocked the Bab al-Mandab straits, Qatar’s gas tankers were forced to go to Europe the long way around Africa.

The abiding assumption among industry groups is that LNG demand will continue to grow through the 2040s. Shell, which was among the earliest and strongest LNG advocates, has identified China as well as “east Asian developing countries” as key areas of growth. In South Asia, Pakistan has gone from an LNG boom to an LNG glut. Having been subject to disastrous blackouts that hobbled households and factories in 2022 (when Europeans outbid ships with the South Asian country’s contracted supplies), the government introduced measures to encourage households and businesses to install solar panels being produced ever more cheaply in China. This led to an extraordinary solar boom—nearly 30 gigawatts of panels have flooded into the country since 2020—that has helped to crash LNG demand.

Large and powerful importers, like India, are increasing their LNG use but are relaxed about locking in more supply, instead picking and choosing between contracts and relying on the spot market, because the latter is often cheaper. India’s contracted LNG falls sharply after 2028, but between Qatar’s planned expansion, the US’s likely expansion, and unexpected falls in appetite from Pakistan and China.

Existential prospects

Building a sovereign dependency on volatile tradable commodities is risky. Exporting countries that are highly reliant on any particular commodity will see their fortunes rise and fall with market movements that most of them have little control over (Mexico is the only oil exporter that has successfully hedged its sovereign exposure to fluctuating prices; OPEC+ increasingly disregards or even disadvantages its smaller members when setting production quotas). For importers, reliance for critical purposes creates a strategic vulnerability and heightens inflation risks—as Western Europe found in 2022.

Gas is volatile, versatile, and everywhere all at once. But LNG’s structural volatility, and security risks amid extreme geopolitical tension, mean it could be on a trajectory to a much more marginal role in the future energy mix than its boosters might suggest. No exporter is safe from declining demand for oil and gas; ships can get blocked from the Bab al-Mandab to the Panama Canal; petrostates and buyers should think twice about locking in new investments and infrastructure. All that is liquified can melt into air.

The Polycrisis is a publication focusing on macro-economics, energy security & geopolitics.

Filed Under